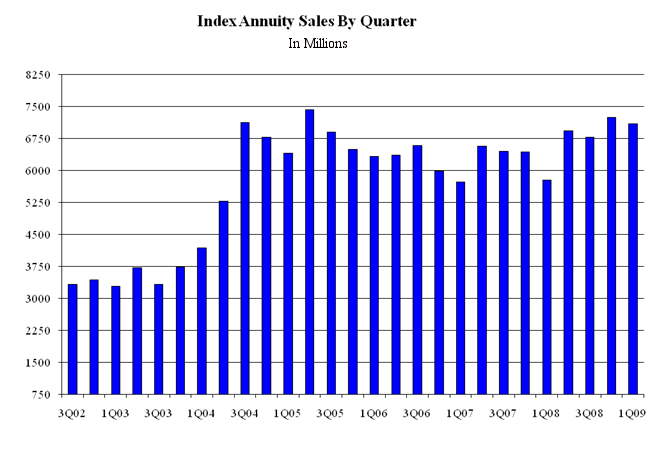

Regulatory Cloud Stifles EIA Market

Only two new EIA contracts were issued in the first quarter of 2009, both with bonuses and both with mandatory GLWBs. They were Forethought Life’s single-premium Income 125 and American Equity’s flexible-premium Retirement Gold.