The completion of a $10 billion partnership between American Equity Investment Life Insurance company (AEL) and Brookfield Asset Management Reinsurance (BAM Re), which was announced last week, is significant in many ways—for AEL, Brookfield, and the US annuity industry.

For American Equity Investment Life, the deal marks the realization of its “AEL 2.0” strategy. CEO Anant Bhalla announced the strategy not long after he joined AEL from Brighthouse Financial in March 2020. His goal: to release surplus capital, raise investment yields, and please impatient shareholders.

“We are taking what would be a spread business focused on return-of-equity and turning that into a fees business focused on return-on-assets,” Steven Schwartz, head of Investor Relations at AEL, told RIJ. “A spread business requires us to hold significant capital. A fees business requires holding less capital. That’s what AEL 2.0 is all about.”

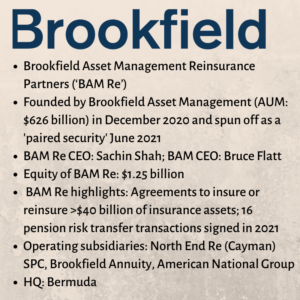

For BAM Re, created only months ago by Toronto-based Brookfield, which manages $626 billion in alternative investments worldwide, the deal makes it a player in the gold rush to manage “sticky” annuity assets. Its competitors—Athene/Apollo, KKR, Blackstone and other private equity firms—are already there.

For the annuity industry, the deal embodies what RIJ has named the “Bermuda Triangle” strategy. It involves a US life insurer, an offshore reinsurer, and an asset manager. For small to mid-sized publicly traded annuity issuers squeezed for years by the Fed’s low interest rate policy, this strategy represents nothing short of survival and independence, at least temporarily.

The fruition of ‘AEL 2.0’

The deal with BAM Re gives AEL, which has an A- rating from AM Best, what it wants and needs. Reinsuring about $4 billion (of AEL’s $55 billion in assets) in existing “IncomeShield” fixed indexed annuity (FIA) contracts with surrender periods of up to 10 years with BAM Re’s North End (Cayman) reinsurer releases about $200 million.

That’s on top of the $350 million AEL gained by reinsuring about $5 billion in a deal with Värde Partners and Agam Capital Management in 2020. To free up more capital over the next six or seven years, AEL will send another $6 billion in assets (75% of projected FIA sales) to BAM Re and North End Re for reinsurance.

Technically, the annuity assets and liabilities will stay on AEL’s balance sheet. But when it moves $3.8 billion to a trust account at North End Re, it will receive a “reserve credit.” Because the capital requirements are lower in the Cayman Islands, AEL only has to move $3.8 billion to North End Re to back $4 billion in liabilities. That’s where the $200 million in released capital comes from.

North End Re’s parent, BAM Re, will manage the money. (AEL’s chief investment officer said in September that AEL intends to allocate” 30% to 40% [of its money] to private asset strategies.”) Out of what BAM Re earns on those assets, it will pay AEL a “ceding commission” of 49 basis points (bps) and an “asset liability management” fee of 30 bps (0.30%). On the $6 billion in future transfers, BAM Re will pay AEL a ceding commission of 140 bps and a 30 bps asset liability matching fee.

Transformative

“This transforms a piece of AEL’s $55 billion spread business into a fee-based business without capital requirements. It’s an important step in diversifying their earnings mix,” Ryan Krueger of Keefe, Bruyette & Woods told RIJ. “AEL will retain over $50 billion of annuity business not being reinsured to Brookfield, of which a portion will be reinsured to a new captive reinsurer” called Project Ray Re. The reinsurer is mentioned in AEL’s December 2020 Form 8-K filing with the Securities and Exchange Commission.

CEO Anant Bhalla of AEL

“Like most of publicly traded life insurance companies, AEL wants to return capital to shareholders,” said JP Morgan analyst Pablo Singzon. “Reinsurance transactions can help them do that. They also need to bring up investment yield. Lower yields mean less attractive products and less profits for the insurer. So they’re updating their investment strategy.”

“AEL had to evolve,” Erik Bass, an analyst at Autonomous Research, said in an interview. “The old formula wasn’t going to work. They were at a disadvantage on the asset side and they were using almost all the capital they generated to support new business growth. They’ve had to issue equity capital in the past to fund some of that growth. They also had a lot of credit risk on their balance sheet.”

AEL’s new strategy also keeps it independent at a time when other small to mid-sized public traded life insurers are being scooped up by private equity (PE) firms. Fending off a takeover bid from Athene Re and MassMutual earlier this year, AEL chose to go its own way. Instead of letting one PE firm manage all of its assets, it will use several.

The stable of asset managers now includes Värde Partners, Agam Capital Management, and now Brookfield. AEL engaged Brookfield to manage only the assets that North End Re reinsures, and not the rest of AEL’s assets. In September, AEL outsourced the management of its traditional fixed income holdings to BlackRock and Conning. “Their goal is to have a diverse mix of best-in-class asset managers,” Bass told RIJ.

BAM’s gambit

BAM Re’s parent, Brookfield Asset Management, the $626 billion Toronto-based alternative asset manager, wanted this deal as much as AEL needed it. Best known as a real estate investor, BAM saw rivals Apollo, KKR, Blackstone and others setting up reinsurers and reeling in chunks of the $500-billion FIA asset pool. It created BAM Re in late 2020 (spinning it off in June 2021) to do the same.

In its first foray into the annuity business, BAM Re paid $5.1 billion for American National Insurance Group, acquiring the Galveston, TX-based, publicly traded insurer’s $30.4 billion in assets (against $23.6 billion in liabilities). American National Insurance Co. had $436.2 million in FIA sales in the first half of 2021, for 17th place on LIMRA SRI’s top-20 list of FIA issuers. American National also sold $468.4 billion in fixed deferred annuity sales, and $53.8 million in income annuity sales.

“The private equity industry is drawn to sticky, low-cost liabilities. FIAs are the most popular right now,” Krueger told RIJ. “The [PE firms] also like funding agreements and pension liabilities with low acquisition costs, which generates assets to invest at more favorable spreads.”

Asset managers have begun referring to FIA assets as “permanent capital.”

FIAs are seen as sticky or permanent because they have terms as long as 10 years. Many of them include surrender charges and market value adjustments that discourage or sterilize withdrawals by policyholders. While contract owners can withdraw 10% per year without penalty, there’s negligible risk of “runs” that would force the asset managers to liquidate illiquid assets like collateralized loan obligations (CLOs).

‘Flow reinsurance’

The AEL-BAM Re relationship, while not exclusive, is meant to last awhile. To “cement” its relationship. BAM Re has already purchased 9.9% of AEL, or about 9.1 million of its common shares. S&P Global reported that BAM Re paid $287.1 million for the shares. BAM Re is waiting for regulatory approval to buy another 10% of AEL, according to press reports.

CEO Sashin Shah of BAM Re

The “flow reinsurance” aspect of the deal extends the BAM Re-AEL partnership out for at least six years. That’s how long the 170 bps fee arrangement is guaranteed for. BAM Re will reinsure new IncomeShield contracts as quickly as agents and advisers sell them. The prospect of AEL receiving steady fees (170 bps on $6 billion is $102 million) for the next several years may comfort AEL shareholders.

Flow reinsurance appears to be on the rise. Lincoln Financial Group, which signed a flow reinsurance deal with Athene in 2017, entered into another one last month with Talcott Resolution Life Insurance Company. Talcott will reinsure up to $1.5 billion in sales of Lincoln’s flagship variable annuity with living benefit riders. (Living benefits are capital-intensive. They are tied to the equity markets and are optional. It’s difficult to predict how many contract owners will exercise them.) The transaction covers business issued from April 1, 2021, through June 30, 2022.

What could go wrong?

As noted above, the AEL-BAM Re deal epitomizes the Bermuda Triangle strategy. The strategy requires a publicly traded US-based life insurer to gather long-term fixed annuity premiums, a Bermuda or Cayman Island reinsurer that saves capital by estimating the annuity liabilities at a lower value, and a deep-pocketed asset manager with expertise in originating bespoke loans to leveraged companies. For the life insurers, there may be tax advantages to reinsuring offshore as well.

The companies at the points of the triangle are often related. The asset manager or the US life insurer may set up and capitalize the reinsurer. In some cases, the asset manager, the US life insurer, and/or the offshore reinsurer are affiliated or co-owned. Indeed, annuity issuers owned by or partnering closely with private equity firms have already captured almost half of the FIA market in the US, according to data from LIMRA’s Secure Retirement Institute.

Analysts see credit risk as the biggest hazard in these deals. As in the run-up to the Great Financial Crisis, the asset managers are securitizing bundles of below-investment grade loans and valuing some of their “tranches” as investment grade securities that life insurers are allowed to own. And when the same company controls all three points of the triangle, the deal may lack the safeguards that unrelated counter-parties might require.

The analysts who spoke with RIJ didn’t seem overly concerned.

“The asset managers may take more risk with the assets than the ceding company did. That’s part of the strategy,” said Bass. “But the asset managers say they’re taking liquidity risk, not more credit risk. They’re investing in, for instance, private corporate loans, private direct mortgages, and aircraft leases instead of publicly traded bonds. And they’re increasing the spread by doing so. But the rating assigned for the assets, and the capital charge for the credit risk on those assets is the same as publicly traded BBB corporate bonds. The credit risk is the same, but they’re taking liquidity risk.”

“They’re investing in assets that AEL previously would not have,” JP Morgan’s Singzon said. “The net effect will be higher yields, which will make AEL more competitive. They haven’t been uncompetitive. But if they want to stay in the FIA market, they have to offer higher crediting rates. It’s all tied to earning more yield on what they have. Now they can ‘drive in both lanes.’ They can be competitive with their policyholders and earn enough profits for their shareholders.”

“Will these higher allocations to private assets produce risk-adjusted returns as good as companies think, or is there more risk than they expect?” Krueger asked rhetorically. “The evidence to date has been positive. There have been no material problems. Lots of smart companies and individuals are adamant that these private assets will continue to generate strong risk-adjusted returns.”

Analysts expect AEL’s 2.0 strategy to help widen its spreads to the neighborhood of 4% and to increase its return-on-equity. “This has been a transition year for the company,” said Krueger. “They’ve been making business investments and holding excess liquidity. We expect an 8% return on equity [ROE] in 2021. But, with the refreshed strategy and completion of various transactions, we’re projecting 11.3% in 2022 and 11.7% in 2023.”

In its December 2020 8-K, AEL bullishly predicted a potential (15+%) ROE over time, “even in a low interest rate environment.” If so, 2.0—and the Bermuda Triangle strategy—will be validated.

© 2021 RIJ Publishing LLC. All rights reserved.