Mr. & Mrs. M. T. Knestor, an actual 60-something couple given a silly made-up name, have $663,000 in savings but no idea how to turn it into lifetime income. In retirement, they’ll receive a combined $63,000 in Social Security and pension income every year, inflation-adjusted. They plan to retire in 2022, when they pay off their mortgage.

The Knestors think they can live on $7,000 a month (pre-tax) in retirement, but they also need a sidecar fund for special expenses, like a new roof, a new car, and a wedding for their daughter. They’re cautious investors, they enjoy above-average health, and they’d like to leave their daughter at least $250,000.

RIJ emailed the Knestor’s numbers to WealthConductor LLC, the Hartford, Conn.-based firm that licenses its “IncomeConductor” time-segmentation software to advisors at 32 broker-dealers. WealthConductor was co-founded in 2017 by Sheryl O’Connor and Phil Lubinski. She’s the CEO. He’s been using, designing and licensing time-segmentation tools since the 1990s.

In this latest in our series of articles on real retirement income cases, RIJ focuses on the time-segmentation or “bucketing” approach to income planning. Bucketing tends to stir controversy because it relies as much on psychology as on finance. But that’s why some advisors like it: Retirement income planning typically requires both.

Meet the Knestors

The Knestors aren’t rich, but their asset level puts them in the top fifth of retirees in the US. They’re married, own a home, and have an $18,000-a-year joint-and-survivor pension (from Mrs. Knestor’s teaching job). At 60, Mrs. Knestor is newly retired. Mr. Knestor, 66, plans to retire and claim Social Security in four years, when he’ll qualify for the most monthly income.

Of their $663,000 in investable savings, the Knestors have two IRAs and a 403(b) account valued at $395,600 today. Their after-tax brokerage account is worth $258,400 and they have $9,000 on hand at their bank. Their 2500-sq ft house on 0.75 acres is worth $250,000 today; they expect it to be worth at least $300,000 in 15 to 20 years.

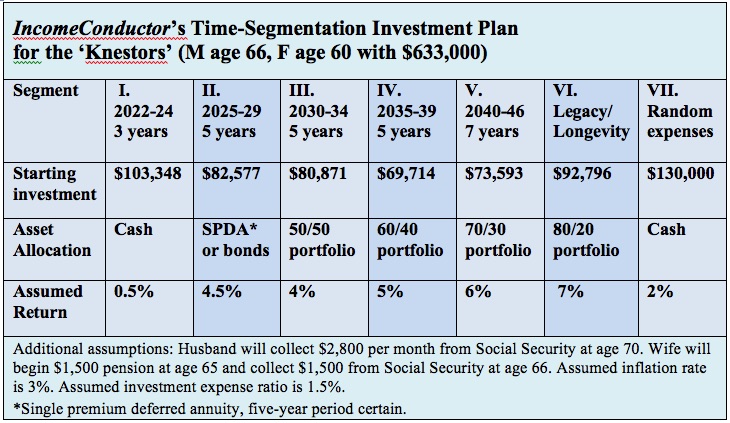

At WealthConductor, Lubinski fed the Knestor’s data into his IncomeConductor software. It produced the seven-bucket time segmentation plan below.

Acknowledging the Knestor’s need for a sidecar fund, Lubinski first designated $130,000 in cash for an emergency fund (Segment VII). In addition, he set aside about $93,000 in an account that, invested mostly in equities, was expected to grow to $503,000 after 25 years—to fund a legacy and as a hedge against longevity and medical expense risk.

Lubinski then set aside $103,348 in cash to cover the Knestor’s income needs in their first three years of retirement (Bucket I on the chart above). That sum would provide $4,328/mo in the first retirement year, to supplement Mr. Knestor’s $2,800 in Social Security benefits and increasing their income to the required amount.

That bucket would need to supply only $2,873 in 2023, when Mrs. Knestor starts receiving her $1,500/mo pension. It would need to supply just $1,467 starting in 2024; that’s when she’ll claim her $1,500 Social Security benefit.

The software assigned $82,577 to the second bucket (2025-2029) to buy a five-year period certain single premium deferred annuity with an internal rate of return (the rate the annuity payments are discounted to equate them to the annuity purchase price) of 4.5%. It will produce $1,629/mo to supplement the Knestor’s Social Security and pension income and raise their monthly income to $7,789.

Phil Lubinski

“The logic is that for the first eight to ten years you have no market risk,” Lubinski said. “That feature really takes the scare out of retirees.”

For the next 17 years of the Knestor’s retirement, IncomeConductor divided their remaining savings into three buckets (5 years, 5 years, and 7 years) to be liquidated for income beginning in years nine, 14, and 19 of retirement, respectively). The asset allocations of these three portfolios will shade gradually to equities (50%, 60% and 70%, respectively) and have increasing assumed rates of return (5%, 6%, and 7%).

Lubinski ran the Knestors’ numbers through the software twice, once assuming historical rates of return and once using a -1.5% net rate of return (including fees) for compliance purposes.

Under historical rates, the couple enjoyed an ending balance of $503,000 (assuming that they exhausted their emergency funds). Under the zero investment return assumption, they had an ending balance of just $63,597. Those numbers do not include the value of the Knestors’ home or any unspent emergency funds.

High maintenance

The overall portfolio becomes more rather than less risky over time. Unless market volatility merits or necessitates mid-segment corrections in the asset allocation of a bucket, the bucket maintains its original asset allocation right up until the time it is needed for current income.

Bucket V, for instance, is designed to “cure” at its 70% equity allocation for 18 years. That’s how much time, on average, it will need in order to grow large enough to cover the Knestors’ need for investment income during the 19th to 25th years of retirement. A system where each tranche were de-risked every five years would be much more complicated.

“The process isn’t, ‘Every segment takes a step to the left every five years.’ It’s, ‘One segment steps to the left and all the others stay where they are.’ The beauty is the clarity of it,” Lubinski told RIJ.

If the segments grow faster than expected, however, and appear capable of reaching their target date and accumulation level with a lower equity allocation, then the advisor and client can de-risk it. IncomeConductor includes a function that alerts advisors to opportunities to de-risk.

“We created automatic emails that say something like, ‘Bucket III needs only a 2% growth rate moving forward,’” Lubinski said. Clients have to acknowledge and approve or reject the advisor’s offer to de-risk. “It takes the clients out of the chasing-yield mindset and moves them to more of a pension mindset.”

The software comes with training and marketing modules, and can be used in conjunction with popular planning software, like MoneyGuidePro or eMoneyAdvisor. According to Lubinski, IncomeConductor has received a clean FINRA review and has been certified as Department of Labor-compliant by Jason Roberts, CEO of Pension Resource Institute.

Academics are divided in their opinions of the time-segmentation method. Zvi Bodie, a pension expert, believes that equity returns grow less predictable over time, and that the assumption of reversion-to-the-mean, the law on which the buckets’ ‘curing’ times are based, isn’t valid. But behavioral finance specialist Meir Statman has said that bucketing leverages the ‘mental accounting’ techniques that many people already use.

Advisors like Lubinski, who swears by time-segmentation, use it because it’s effective for them and their clients. Bucketing pushes risky assets into the distant future, so to speak, so that clients don’t feel threatened when markets hit a turbulent patch. Clients are therefore less prone to panic and sell depressed assets.

Lubinski prefers bucketing to the classic retirement distribution method of setting up a systematic withdrawal plan (SWP) from a balanced total return portfolio. Such portfolios offer higher potential rewards but at higher risks, and a SWP based on the 4%-per-year rule can put monthly income levels at the mercy of short-term market performance.

“When you have one big bucket, your gains can vary dramatically from year to year,” Lubinski told RIJ. “That strategy may have made sense years ago when stocks were paying steady dividends and there was a stable high interest rate. But we don’t have that today.

“If we have another 2008-type event,” he added, “the client can see that some of their buckets are on fire. But they can also see that by the time they get to that point of needing those buckets, they will probably have recovered.”

© 2018 RIJ Publishing LLC. All rights reserved.