In today’s cover story, which is based on an interview with Lincoln Financial executive Will Fuller, we note that Lincoln is smaller than some of its close domestic rivals near the top of the retail annuity sales charts, like AIG or New York Life. Nor does it have a big foreign parent, as Jackson National does.

In fact, Lincoln has grown and shrunk over the past 40 years in response to trends, events and opportunities. These include the conglomerate craze that began in the 1960s, the GE/Jack Welch divestiture trend in the 1980s, the post-1986 variable annuity boom, the bull market of the 1990s and the Great Financial Crisis of 2008-2009.

To learn more about this history, we turned to actuary Jeffrey K. Dellinger, who designed Lincoln’s annuities from 1981 to 2002 and headed Lincoln’s Individual Annuities business. He pioneered the development of variable annuity (VA) living benefit riders, patented Lincoln’s uniquely flexible i4Life income rider, and wrote “Variable Income Annuities” (Wiley Finance, 2006).

Dellinger

What follows might be considered a brief history of Lincoln Financial. While it represents the view of just one person, that person was in a position to observe a lot.

Insuring NASCAR

“Before around 1980 Lincoln abided by the favored corporate strategy of the day, which was ‘be a highly diversified company,’” Dellinger told RIJ. “The Lincoln National Life Insurance Company, founded in Fort Wayne, Indiana in 1905, is and was the flagship insurance company. But it formed a holding company, Lincoln National Corporation (LNC) in 1968. LNC has at various times owned First Penn-Pacific Life, which sold fixed annuities and owned a universal life (UL) administration system; American States Insurance Company, a property/casualty insurer; and Chicago Title and Trust Co.

“Lincoln offered life insurance, individual annuities, employer-sponsored annuities, individual mortgages, mutual funds, group health, disability income insurance, reinsurance, and structured settlements. It had a full-service defined benefit pension business and a pension risk transfer business. Outside the U.S., it was in the UK and Mexico. Lincoln even owned K&K Insurance Specialties, which insured major sporting events, including automobile racing events like NASCAR.”

But the conglomerate era passed, succeeded by a downsizing era. “In the 1980s, corporate strategy in the American academic world did a 180-degree turn. The new mantras were: ‘Narrow your focus’ and ‘Only engage in businesses where you can be a market leader or at least one of the top three companies,” Dellinger said.

Lincoln sold American States Insurance Company to Safeco and Chicago Title and Trust Company to Alleghany Corp. Lincoln exited its huge group health insurance business, its disability income business, its defined benefit pension business, and its pension buyout business. It sold its huge Lincoln National Reinsurance Company to Swiss Re and sold K&K to AON. It even outsourced its travel department and IT functions.

By the early 1990s, Lincoln was down to three core business lines: Individual annuities (the largest), employer-sponsored annuities, and life insurance. There was also the closed block of annuity buyout business the company was letting run off its books rather than selling.

Annuities take center-stage

“Lincoln’s individual annuity business was the earnings engine of LNC. Three things primarily accounted for this. First, alternative tax-deferral investment vehicles mostly went by the wayside due to federal tax law changes in the 1980s, leaving deferred annuities in an advantaged position,” Dellinger said.

“Second, while Lincoln was already selling individual annuities, primarily through its career agency system, its affiliation with American Funds Distributors (AFD) helped supercharge sales growth. At the time, Lincoln’s American Legacy VA product suite was the only place where you could get American Funds’ investment adviser, Capital Research & Management Company, inside a variable annuity. That relationship gave Lincoln access to tens of thousands of brokerage advisers as well as AFD’s wholesalers.

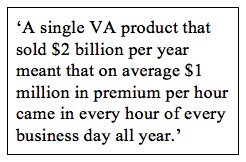

“This growth opportunity—and the bull market of the 1990s—spawned huge individual annuity product development. With so much at stake, a lot of attention was paid to pricing and asset/liability management. The design and pricing had to be proper because Lincoln’s tremendous individual VA sales growth and assets under management would magnify the impact of mistakes. Lincoln’s annuity business was the third largest in America, behind only TIAA-CREF and Hartford Life. Think about it: A single VA product that sold $2 billion per year meant that on average $1 million in premium per hour came in every hour of every business day all year.”

Wholesale changes

One more factor that affected Lincoln’s size: After a period of divesting non-core businesses, Lincoln started buying life insurance businesses.

“Wall Street analysts would often say that Lincoln’s individual annuity business line accounted for too much of its profits,” Dellinger said. “In response, then-CEO Jon Boscia once again had Lincoln entertaining acquisitions. This time, however, it was acquisitions of life insurance companies or blocks of life insurance. This led to the Jefferson-Pilot acquisition in 2006 and the acquisition of CIGNA’s life insurance operations.”

But these acquisitions didn’t produce a full counterbalance. Rather, Lincoln’s individual annuity business continued to dominate its earnings, and grew organically rather than by acquisition, he said.

The fact that Lincoln’s flagship American Legacy VA lost its monopoly on American Funds did not help Lincoln’s growth. American Funds became available in the Hartford Leaders VAs and, later, in other insurance companies’ individual VAs. At the same time, wholesaling for American Legacy VAs shifted from American Funds Distributors to Lincoln’s new in-house wholesaling company, Lincoln Financial Distributors. That was expensive.

“It takes a lot of money to start a several-hundred-strong collection of external-internal wholesaler pairs,” Dellinger told RIJ.

Crisis and bailout

Lincoln is relatively small compared to its peers in part because of the turmoil it endured one decade ago, he added. “Lincoln had written a lot of VAs with guaranteed living benefits (VA/GLBs), particularly guaranteed lifetime withdrawal benefits (GLWBs). Due to my work on these for my 1999 GLWB patent, I had strong familiarity with their characteristics.

“It was clear that sufficient GLWB sales, if mismanaged or mis-hedged, could eventually cause solvency-threatening risk exposure for insurers. While a federal government bailout of an insurance company had not yet ever happened, I wrote two to three years before the financial crisis that it was likely to come when the next large downturn in stock values occurred.

“So due to factors including liquidity and VA/GLB issues, Lincoln needed a government bailout. To receive one, it had to turn itself into a bank holding company to qualify for the federal money. Lincoln stock dropped from $74.72 on April 30, 2007 to $4.76 on October 31, 2008. In 2010, Lincoln sold Delaware Investments, its investment department and mutual fund company, to raise cash. This shrunk the company a little.

“To its credit, Lincoln did not exit the individual variable annuity business or the individual annuity business in total. Rather, it sought external help from an actuarial consulting firm to help it understand the investment risks inherent in its product designs and ways to mitigate such risks through product design, pricing, and especially hedging.

“The company doesn’t want to make annuity acquisitions—except for some compelling strategic advantage—that would exacerbate its dependence on its individual annuity business line for earnings. As an aside, another reason Lincoln is relatively small is that a big European company hasn’t swallowed it up.”

The stock buyback era

“Share buybacks have also shrunk Lincoln in size. Like many public corporations, Lincoln has bought back shares of its own stock. It’s safer for corporations to keep dividends low and instead return money to some shareholders via buybacks. The number of shares outstanding is down. Lincoln had 319 million shares outstanding in 2010 and has about 200 million today. So more than one share in three has been retired in the last decade. This, too, keeps Lincoln smaller than it might otherwise be,” Dellinger said.

“I recall Lincoln having a market value of around $7.5 billion perhaps 20 years ago. Its current market value is around $11.64 billion. Its growth rate—about 2.3% per year—is the combined result of earnings made, earnings reinvested in the company, earnings paid out as dividends, and earnings spent on stock buybacks. The point is that the size of the company hasn’t grown at much of a clip. In sum, there are many reasons why Lincoln is the size it is.”

© 2020 RIJ Publishing LLC. All rights reserved.