Issuers of fixed indexed annuities (FIAs) generate returns for contract owners based mainly on the movement of equity indexes. By purchasing options on the indexes with part of the income they glean from investing client money in bonds, they can capture some—but not all—of the index growth.

Low interest rates and high market volatility are headwinds for FIA issuers. Low rates can squeeze the issuer’s budget for buying option. Volatility can drive up the cost of options. But, internally, FIAs contain many levers and dials that an issuer can manipulate to burnish a product’s curb appeal.

Two powerhouses of the FIA world, AIG Life & Retirement and Scottsdale-based Annexus, a designer and distributor of FIAs, use almost every possible tool to enhance X5 Advantage, a new FIA with a non-optional lifetime income benefit. AIG’s American General Life subsidiary is the issuer.

The X5 Advantage orchestrates a symphony of deferral bonuses, a long surrender period, embedded fees, leverage, risk-sharing negative floors, assumed lapse rates, volatility-managed indexes, caps, participation rates, spreads and finely-tuned age-based payout rates to serve a surprising number of purposes.

With only a small bit of skin, indirectly, in the equity markets, X5 Advantage aims to satisfy the revenue needs of the life insurer, the distributor, the agent/adviser, and—eventually—to mitigate a client’s market risk, sequence risk, mortality risk, longevity risk and nursing home risk.

Impossible? Not if you hold it long enough. Like a tough cut of beef that becomes fit for a king if you cook it for a long time at a low temperature, this product aims to turn the little that the market offers right now into a feast for everyone involved. It’s a marvel of financial engineering.

Bonuses are the key

X5 Advantage has two stages: An accumulation stage that starts at purchase, and an income stage that starts no less than 10 years later, at the end of the surrender period. During the accumulation stage, the client gets interest credits based on the performance of options on volatility-managed equity indexes from PIMCO, Morgan Stanley or S&P.

The payout rate doesn’t reach 5% of the benefit base until age 70 for a single person (4.5% for a couple), but there are bonuses. During the accumulation stage, the benefit base (equal to the premium at the time of purchase) rises by 200% of each year’s earnings. During the payout stage, the benefit base rises by 150% of the annual earnings.

Here’s how AIG illustrates the product in its brochure. John, a 60-year-old who plans to retire at age 70, funds his X5 Advantage with a $100,000 premium and chooses a 10-year strategy with two five-year terms. Ten years later, his account value is $165,772. But, thanks to the annual bonus, his benefit base has grown to $247,937.

At age 70, and not before, John begins drawing an annual income of 5% of the benefit base, or almost $12,400. The benefit base, and the income stream on which it is based, both keep growing after income begins, by the aforementioned 150% of annual credited interest. These are better terms than a deferred income annuity (DIA) with 10-year deferral period could promise. Anecdotally, that’s partly because FIAs have higher lapse rates than DIAs, which are virtually illiquid.

If John becomes ill and needs nursing home care, he can receive double the usual income amount for up to five years. There are two death benefit options. If John died at age 70, for instance, his beneficiaries could get either his account value ($165,772) in a lump sum or his benefit base ($247,937) in five annual payments of $49,587 each.

Participation rates, spreads and risk-sharing

Those are the bonuses. What about the caps and participation rates on the interest crediting methods? The issuers carefully manage the portion of the index gains the FIA owner can lock in at the conclusion of each one-year, five-year, or ten-year crediting term.

And what about the indexes? In this case, the three custom indexes all contain volatility controls that can dampen the index gains from the inside and take out the market spikes.

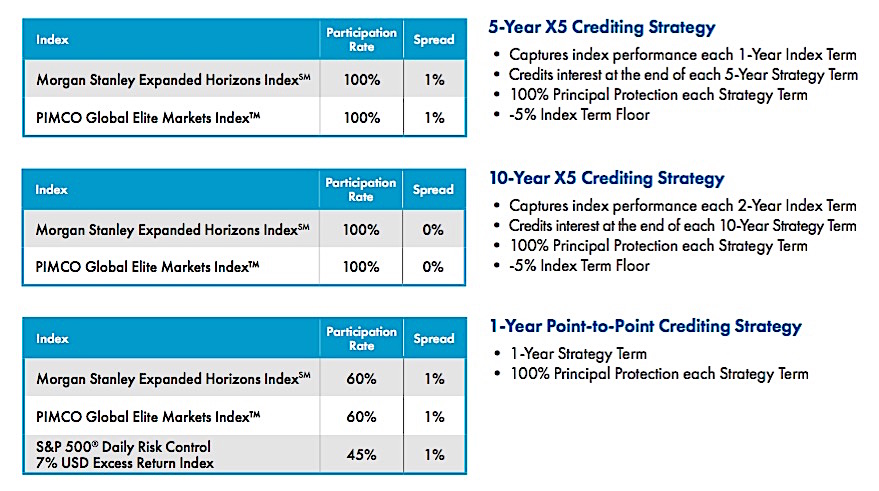

Contract owners can get exposure to the Morgan Stanley Expanded Horizons Index, the PIMCO Global Elite Markets Index and an S&P 500 Daily Risk Control 7% USD Excess Return Index. The box below lists the current crediting rates, according to AIG’s product rate sheet.

From the X5Advantage Rate Sheet

As an example of volatility control, let’s compare the S&P 500 Daily Risk Control 7% USD Excess Return with the traditional S&P 500 Index. The risk-controlled version has a net one-year return of 3.87% while the traditional version has a one-year return of 2.31%. The “Excess return” part of the index name reflects the fact that the investment is leveraged; the contract owner gets the portion of the return (3.87% in this case) that was in excess of the cost of borrowing money to do the leveraging.

Looking again at the box above, you can see more of the dials and levers that allow the issuer to fine-tune the risk/return proposition. For instance, two of the crediting strategies have 1% “spreads.” That means the contract owner would get the participation rate (100%, 60% or 40%, depending on the strategy) of the index return minus 1%.

Both the five-year and 10-year strategies have a minus-5% floor on possible losses in any one-year or two-year term within a crediting period, respectively. (But a negative return for the entire crediting period is guaranteed not to occur.) This risk-shift to the client allows the issuer to advertise slightly higher caps by shifting some of the investment risk to the client.

The one-year strategies have participation rates that are less than 100%. If the index gained seven percent, for instance, the client gets either 45% or 60% of 6% (2.7% or 3.6%) depending on which index he or she chose. The one-year option also has a 1% spread, which is subtracted from the credited interest. It also has participation rates, which are alternatives to caps.

To protect the issuer, the rates are subject to change by the issuer at the end of each crediting period. To protect the client, there are guaranteed minimums. The five-year crediting strategies have a minimum participation rate of 50%, a maximum spread of 3%, and a minimum index term floor of -10%. The one-year point-to-point crediting strategies have a minimum participation rate of 25% and a maximum spread of 3%. The ten-year crediting strategies have a minimum participation rate of 50% and a maximum spread of 3%.

As good as it gets

The past dozen years have been tough for annuity issuers. With low bond yields reducing the return on their fixed income assets, but a booming equity market, they’ve had to create products, such as variable and index annuities, that tap into the bounty of the long bull market. It creates a lot of complex engineering to interface an insurer’s general account with the equity markets without violating any state or federal regulations.

For indexed annuities to do a lot with a little, they also need time. But as long as the contract owner holds onto the contract and follows its rules, several of his or her major retirement risks will be addressed. For near-retirees who can’t afford a fee-based adviser, products like the X5 Advantage may be as good as it gets under current market conditions.

© 2020 RIJ Publishing LLC. All rights reserved.