The number of life insurers offering a variable or “structured” index annuity with a lifetime income benefit has suddenly doubled. CUNA Mutual Group’s new Zone Income Annuity has joined Allianz Life’s Index Advantage Income contract, raising the number of products in this micro-niche to two.

Investors and advisers who like the risk-reward proposition of the structured index annuity (aka registered index-linked annuities or RILAs) and wish they could pair it with an income rider have had only the one option until now. Other companies have avoided attaching income riders to structured annuities, in part because they’re still digesting the living benefit risk they took on a decade ago when selling more than a trillion dollars worth of variable annuities with generous guaranteed lifetime withdrawal benefits (GLWBs).

A structured index annuity works like a fixed index annuity, except that the upper limits (caps) on returns are higher because the client agrees to accept some risk of loss. The new CUNA Mutual annuity appears to differ from Allianz Life’s Index Advantage Income in allowing the client to take extra risk (and get more upside potential) even after income begins.

Zone Income offers a 10% floor on losses, as opposed to the more common 10% buffer in this type of product. A buffer shields the contract owner from the first 10% of losses in a contract year. A floor shields the contract owner from a loss in excess of 10% in a year. Zone Income has only one term length—six years—and a starting surrender penalty of 9%.

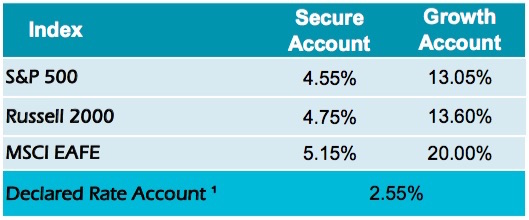

Contract owners can get exposure to the S&P500 Index of large-cap domestic stocks, the MSCI-EAFE Index of developed country stocks, or the Russell 2000 Index of small-cap domestic stocks, or they can invest in a fixed rate account. Here are the current rates (to August 25, 2019):

The money that’s dedicated to each index option then has to be split between a Secure Account and a Growth account, in 0% to 100% deciles. Each combination has its own upside cap and its own downside floor. For the S&P500, a 50/50 Secure/Growth split would have a cap of 8.8% and a floor of -5%.

“Our belief is that people like a known risk rather than an unknown risk,” said Martin Powell, CUNA Mutual Group’s head of annuity distribution. “So we allow the client to dial the risk up or down. They can take a -2.5% floor one year and move to zero the next year. It also helps advisers with their compliance requirements.”

The income benefit

As for Zone Income’s lifetime income rider, the client invests a lump sum at a certain age, and is assigned a certain base withdrawal rate (such as 4.5% for a single person age 60 to 64). The starting benefit base (the amount by which the withdrawal rate will be multiplied to determine the annual payout) is the purchase premium. For every year the client delays taking income, the withdrawal rate goes up by 0.30 percentage points. Unlike a deferral bonus that increases the benefit base—a characteristic of benefit riders of a decade or more ago—a withdrawal-rate bonus doesn’t raise contract fees. The benefit base can increase over time as the account value grows, but it cannot go down.

For instance, a couple that bought the Zone Income Annuity when both were age 60 would have a starting withdrawal rate of 4%. If they waited five years to take their first withdrawal, their lifetime withdrawal rate would have risen by 30-basis points per year to 5.50%. (A single person’s withdrawal rate would be 0.50% higher.) There’s an annual 0.75% contract fee and a 0.50% income rider fee.

“We give you both the step-up in account value each year [if there’s a gain], and the 30-basis point increase in the withdrawal rate,” said Elle Switzer, director, annuity product development at CUNA Mutual Group. Her company has the risk budget to attach a living benefit to its RILA because it doesn’t have a big book of living benefit business, and the risks associated with one, left over from historical VA sales.

Allianz Life’s Index Advantage Income contract, which launched in August 2018, works a bit differently. The minimum benefit base is not locked in until income payments start, rather than at the purchase date as in the Zone Income product. At 5.20%, Index Advantage Income’s base withdrawal rate for a couple at age 60 is much higher than Zone Income’s. With deferral credits of 1.8 percentage points, the withdrawal rate rises to 7.0% after a five-year wait.

There’s a trade-off, however. After income starts, all of the money in Index Advantage Income moves into the equivalent of a fixed indexed annuity contract and stays there. The Zone Income contract owner, by contrast, can continue to enjoy much higher caps than the Index Advantage owner during the payout phase, and potentially achieve a higher annual income. Index Advantage has a 1.25% annual contract fee and a 0.70% income rider fee. It has a single six-year term and the surrender penalty starts at 8.5%.

© 2019 RIJ Publishing LLC. All rights reserved.