An Entrepreneur Tackles Decumulation, with TIPS

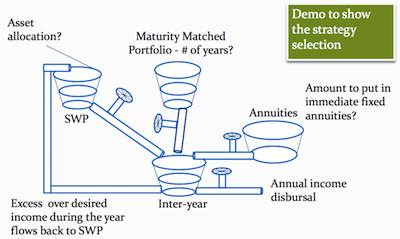

Manish Malhotra’s FIAP platform, set to launch next year, will enable advisors to build retirement income streams out of laddered TIPS, immediate annuities, and withdrawals from balanced portfolios.

Manish Malhotra’s FIAP platform, set to launch next year, will enable advisors to build retirement income streams out of laddered TIPS, immediate annuities, and withdrawals from balanced portfolios.