Heather and Simon, two 65-year-olds on the verge of retirement, have joined the bibulous Las Vegas gambler, Jorge, and the five 95-year-old bridge-playing tontine-minded grandmothers, among the useful fictions created by Moshe Milevsky, the Toronto-based annuity expert and author.

In a recent paper, Milevsky, a finance professor at York University’s Schulich School of Business, introduced Healthy Heather (in glowing health) and Sickly Simon (in miserable health) to illustrate the point that people without long life expectancies can still get value from broad-based pensions like Social Security—but not as much from individual retail annuities, which are purchased voluntarily.

Even though healthy people receive more on average from a defined benefit (DB) pension system like Social Security—the healthy obviously live longer and collect benefits longer—shorter-lived people still get an important benefit because their life expectancies are more uncertain, statistically speaking. Ironically, they have more “longevity risk” than healthy people.

“Swimming with Sharks: Longevity, Volatility and the Value of Risk Pooling,” as the paper is entitled, is timely. The US approaches a reckoning over Social Security reform. As policymakers contemplate raising the initial age of eligibility (62) and or the full retirement age (67) to save money, the impact on people with shorter life expectancies will be an issue. Meanwhile, many individual Boomers (of varying life expectancies) have difficulty gauging if retail annuities are a “good deal” or not. This paper can inform discussions of both issues.

Cross-subsidies

Milevsky

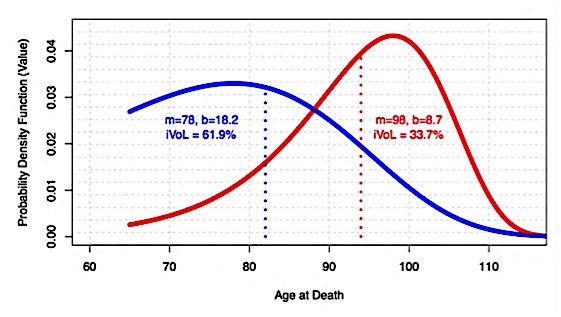

In Milevsky’s paper, Heather and Simon are each eligible for lifetime pension benefits of $25,000 a year from their employer. But she is in excellent health (a “shark,” in Milevsky’s metaphor) and expects to collect her pension until age 95 while he is in poor health (a “fish”) and will be lucky to reach age 75. So the pension plan, which is geared to average life expectancy, appears to be a much worse deal for him than for her.

How big is that shark-bite? At current rates, a life insurer would charge Heather (before fees and costs) $487,250 for a 30-year period certain annuity paying $25,000 a year, Milevsky calculates. The same insurer would charge Simon $212,750 for a 10-year period certain annuity paying the same annual amount. Since their pension plan (hypothetically) had to set aside about $350,000 for each of them, he suggests that Simon subsidized Heather to the tune of $137,250 ($350,000 – $212,750).

This seems to reinforce the conventional wisdom that people in relatively poor health should avoid life-contingent pensions: they’ll simply be handing money over to the longer-lived members of their annuity “cohort.” Not necessarily, Milevsky says. Not only do a certain number of disadvantaged people reach age 95; in fact, as noted above, their date of death is less predictable than that of healthy and wealthy people.

Happy as a CLM

To understand this argument, you need to be acquainted with the “Compensation Law of Mortality” (CLM). It states, “the relative differences in death rates between different populations of the same biological species decrease with age.” The law is also described as “late-life mortality convergence.”

“So, although there is an expected transfer of wealth, there are still insurance and risk management benefits to accepting such a deal,” Milevsky said. The chart below makes this easier to see.

“It’s more subtle than ‘Oh, fish might live a long time,’ Milevsky told RIJ. “It’s really about what pure academic economists call risk aversion. Basically, the uncertainty for the “fish” is much wider (see the blue curve above) so they value insurance more. They get more utility. They are willing to pay a higher ‘loading’ in the insurance sense. The reason their Longevity Risk is larger (again, blue curve) is because of the CLM. Nature made unhealthy people have higher volatility of longevity. Nature wants us all to pool.”

There’s an even more esoteric explanation for this phenomenon. A 1991 paper by Leonid A. Gavrilov and Natalia S. Gavrilova, discusses reliability theory, which includes a process called “redundancy depletion.” This describes the eventual loss of the back-up cells or systems that help people (and machines) function even after their primary systems or defenses break down.

“Redundancy depletion explains the observed ‘compensation law of mortality’ (mortality convergence at older ages) as well as the observed late-life mortality deceleration, leveling-off, and mortality plateaus,” the authors wrote.

Three takeaways

CLM is powerful enough, in Milevsky’s view, to make less-healthy people participate in mandatory pensions like Social Security. But it’s not strong enough to justify their purchase of retail life annuities, where “adverse selection”—the tendency of healthy people to buy life annuities—makes these products especially expensive for people with shorter longevity expectations.

Milevsky wrote in an email:

“I was trying to make three points in that paper and (academic) presentation I delivered at the HEC-Montreal conference. The first was about bio-economics, the second was about pension economics and the third about lifecycle economics:

Biology. The compensation law of mortality (CLM) implies that individuals with high mortality rates (fish) tend to have higher volatility of longevity risk compared to those with low mortality (sharks). So, the fish subjectively “value” life annuities more than the sharks, all else being equal. In some sense one can think of it as Mother Nature wanting the poor and rich to pool longevity risk together.

Pensions. Forcing people with high mortality rates to effectively pay the same price for annuities as individuals with low mortality, for example as in mandatory (unisex) DB pension plans, creates a large financial subsidy from high mortality to low mortality. But luckily, this is partially offset by CLM.

Lifecycle. Unless insurance companies start offering micro-tailored annuities (underwritten for each and every fish and its health), I would argue that a lot of retired fish who already have substantial pre-existing annuity income (e.g. Social Security), should not purchase any more annuities that are priced for sharks.”

[It should be noted that some life insurance companies in the US and UK do offer life annuities at a discount for people who have illnesses that are likely to shorten their lives. These contracts are called “medically underwritten” or “impaired” annuities.]

© 2018 RIJ Publishing LLC. All rights reserved.