During the financial crisis of 2008, the Federal Reserve created trillions of dollars to bail out insolvent banks. At the time, politicians warned the American people, incongruously, that their nation was “broke” and on the brink of “hyperinflation.”

Many ordinary people couldn’t help wondering how the country could be so rich and so poor at the same time. The only economists who seemed able to answer our questions were the relatively obscure academics who whose work involved “Modern Monetary Theory,” or MMT.

Stephanie Kelton, an economist at Stony Brook University, was one of them. With a Ph.D. from the University of Missouri at Kansas City, she has emerged as MMT’s most visible proponent. I heard her speak at a Morningstar conference in 2016. She’s been an economic adviser to the Democrats on the Senate Budget Committee. Last month, she published “The Deficit Myth” (PublicAffairs, 2020), a layperson’s guide to MMT. On Amazon.com, it’s a best-seller in the Money and Monetary Policy category.

Stephanie Kelton

In the book, Kelton describes MMT’s foundational concepts: That wealth in the private sector increases when federal debt increases; that the country’s finances are the opposite of a household’s; and—counter-intuitively—that the federal government spends before it taxes or borrows (not after).

A few weeks ago, RIJ interviewed Kelton about her book and the controversy around MMT. Her book could not be better timed: In 2020, as in 2008, the federal government showed that it does, as predicted by MMT, have a virtually unlimited supply of dollars. If that’s true, Kelton and other MMTers might say, we should be using it more deliberately, and for better purposes.

What is MMT?

Here are three of MMT’s core principles, which Kelton presents not as theories but as facts about the world we’re living in today:

Public debt is private wealth

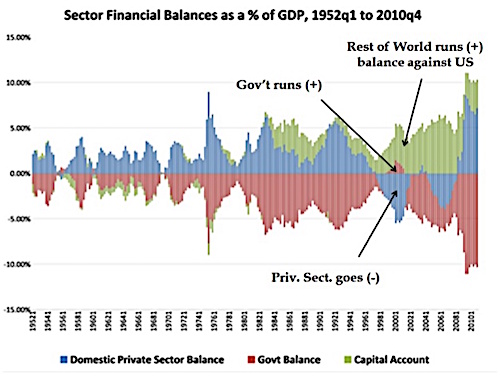

According to Kelton, the federal debt is a measure of how much money the government has spent into the economy and not taxed out. In other words, the $16 trillion in federal debt held by the public isn’t an economic albatross or millstone, and not a burden on our grandchildren, but a measure of assets held by the public as savings or investments.

“Government deficits are always matched—penny for penny—by a financial surplus in the non-government bucket,” Kelton writes. “At the macro (big picture) level, Uncle Sam’s red ink is always our black ink. When he spends more dollars into our bucket than he taxes away, we get to accumulate those dollars as part of our financial wealth.”

The U.S. is not a household

Most of us are experts on household finance. We know that if we borrow too much we’ll be in trouble. Our credit card bills will mount, crowding out savings and investments. We know that if companies, school districts or even state governments borrow too much, they’ll fail.

But MMT says that the federal government isn’t like a household. Unlike households, the government can levy taxes, issue legal tender, and extend its liabilities over an infinite time horizon. Ipso facto, Uncle Sam can’t go broke.

The government spends first, then taxes or borrows

We learn in economics class that the government finances itself by taxing us, by borrowing from us, or by watering the money supply (printing dollars).

The reality is precisely the reverse, MMTers say. Money has a life cycle. It is born when the government spends it into existence or banks lend it. It circulates through the banking system to the global economy, financing purchases of goods, services or investment assets. It dies when people pay taxes and repay loans.

“All government spending is paid for first,” Kelton writes. “Then, through taxing and borrowing, some of it is subtracted away.” Since only the government can issue money—barring counterfeiters—it can’t happen any other way, MMTers say. There’s no currency to tax or borrow until the government issues it.

“They’re all trying to say that the problem with MMT is that it takes advantage of the ‘printing press.’ But we’re saying that this is how the government works,” she told RIJ. “We’ve always described MMT operationally. It’s not a proposal. It’s how government finance works today.”

Criticism and praise

MMT has drawn a range of reactions, from the skeptical to the hostile to the passionately favorable. Progressive politicians like Rep. Alexandria Ocasio-Cortez (D-NY) and Sen. Bernie Sanders (D-VT) are drawn to MMT; it validates their desire to spend public money on public projects, like affordable housing, universal health care, and better schools. Mainstream economists often call MMT a recipe for inflation.

Philosophically, MMT’s polar opposite is be the “Austrian School” of economics, which is based on the work of Ludwig von Mises and Friedrich Hayek. Austrians tend to believe in holding gold. In a recent blog post about MMT, the Institute’s president, Jeff Diest, accused its advocates of promoting the seductive but illusory idea that governments can legislate prosperity.

Philosophically, MMT’s polar opposite is be the “Austrian School” of economics, which is based on the work of Ludwig von Mises and Friedrich Hayek. Austrians tend to believe in holding gold. In a recent blog post about MMT, the Institute’s president, Jeff Diest, accused its advocates of promoting the seductive but illusory idea that governments can legislate prosperity.

“The promise of something for nothing will never lose its luster,” Diest wrote. “MMT should be viewed as a form of political propaganda rather than any kind of real economics or public policy. And like all propaganda, it must be fought with appeals to reality. MMT, where deficits don’t matter, is an unreal place.”

But his critique was qualified. “Kelton deserves credit for writing a book aimed at lay audiences instead of for her peers in academic economics,” Diest wrote. “Unlike most of those peers, she seems genuinely interested in helping us understand how the world works. And unlike most left progressive academics, she also seems interested in helping average people improve their lot in life.”

Gregory Mankiw, an economics thought-leader at Harvard, doesn’t much like MMT. He describes himself as a monetarist: if the money supply outgrows real economic output, inflation occurs. He’s agrees with government-led monetary policy (the Fed’s rate adjustments), but not aggressive government-led fiscal policy, which MMT favors.

But in a recent paper on MMT, he wasn’t entirely unkind. “My study of MMT led me to find some common ground with its proponents without drawing all the radical inferences they do,” he writes.

“I agree that, in a world of pervasive market power, government price setting might improve private price setting as a matter of economic theory. But that deduction does not imply that actual governments in actual economies can increase welfare by inserting themselves extensively in the price-setting process.” [That is, instead of letting the forces of supply and demand determine prices.]

But MMT also has friends in places that might surprise you. A defense of MMT was published in 2019 at at GMO.com, home of the well-known and widely respected value investor Jeremy Grantham. GMO partner James Montier wrote:

“Modern Monetary Theory (MMT) seems to provoke a visceral reaction amongst the ‘great and the good’ such as [Kenneth] Rogoff, [Paul] Krugman, and [Larry] Summers. In my experience, MMT provides a much more accurate and insightful framework for understanding the economy than the precepts of neoclassical economics.”

But “The Deficit Myth” has attracted a lot of positive attention, Kelton told RIJ. She’s been interviewed by journalists from Vox, the Financial Times, Bloomberg, The Nation, and many other publications. “My days and nights are filled with exchanges, and the vast majority are positive and enthusiastic,” she told RIJ. “I’m getting invitations from all over the world to speak at conventions of world leaders and heads of industries.”

‘Radical’ implications

MMT draws criticism in part because it is not as politically neutral as Kelton makes it sound. Mankiw called it “radical,” and it is. MMT turns the conventional economic worldview upside down when it implies that federal debt isn’t necessarily bad or that America pays its taxes and buys Treasury bonds with money that government has already spent. And when it justifies aggressive government spending on health care, jobs, and a “Green New Deal,” MMT inevitably invites comparisons to socialism.

“I trust in the democratic process,” she said in a recent email. “Congress should work to deliver a budget that best reflects the will of the people. And if people want a border wall instead of more hospitals and schools, that is what we’ll get. The goal is to bring the public into the conversation.”

MMT can’t answer the political questions that its economic ideas raise. Even if the government spends much more money, legislators and policymakers will still fight over what to spend it on. Even if higher taxes are better for fighting inflation than high interest rates, people will still fight over whom to tax and by how much.

But no other school of economics answers those questions either. No other economists have ever been able to answer all of the serious questions raised by the 2008 and 2020 financial crises and the subsequent Fed rescues. MMT has come closer than most.

When House Speaker John Boehner in 2009 said that the government had to tighten its belt because households had to tighten their belts, or when George Bush and Barack Obama later said that the government was “broke,” all of them were wrong. Only MMT could explain why. The same has been true in the current crisis. Traditional economics has no recommendations for our worst-of-both-worlds situation, where we’re spending fortunes without investing in the future.

MMT and Social Security

Given its applicability in financial crises, MMT has generated a lot of media attention relative to its size. All of its leading figures—Warren Mosler, Randall Wray, Bill Mitchell, Stephanie Kelton, Pavlina Tcherneva, and Scott Fullwiler—could fit around a large dinner table.

And while they don’t lack for important academic predecessors—Keynes, certainly, Wynne Godley and Hyman Minsky, whose “financial instability hypothesis” was rediscovered in the Great Recession and gave impetus to MMT—the nation’s most influential economics departments have not been hospitable to economists specializing in MMT.

You won’t find MMT economists on the faculties of the biggest and most prestigious universities. They teach at fine schools like Bard College, the University of Missouri at Kansas City, the State University of New York, but not at the University of Chicago, Harvard, or MIT, whose graduates will someday set policy in Washington and on Wall Street.

Social Security, which will technically run short of money between now and 2034, might turn out to be a test case for MMT. In the conventional view, Social Security is a zero-sum game between America’s tax-paying workers and the rising number of retirees their payroll taxes support. It’s assumed that unless payroll taxes go up or benefits go down, the system will fail to fulfill its promises.

On the topic of retirement income, I asked Kelton for her thoughts on the Social Security funding dilemma. She doesn’t see it as a crisis. If Congress can’t agree to lift the cap on the earnings subject to FICA taxes, she told me, it could cover the impending Social Security funding shortfall with an appropriation from general funds—the way it currently pays for most of the costs of Medicare Part D. Social Security doesn’t face an actual funding crisis, she said, “but if everybody agrees to keep up that fiction, I don’t know who will win.”

© 2020 RIJ Publishing LLC. All rights reserved.