Anybody with a stake in the annuity business—as an advisor, distributor or manufacturer—needs to know at least a little about application programming interfaces, or APIs. Last week, RIJ reported on the June launch of Envestnet’s Insurance Exchange, whose seamless integrations of data and software depend on these interfaces. This week, we take a second (but non-technical) look at them.

By now we all use APIs almost every day, and certainly whenever we shop online. For example, a FedEx or UPS might add its API to an e-commerce site—a Land’s End or L.L. Bean platform, maybe—to facilitate “ordering shipping services and automatically include current shipping rates, without the site developer having to enter the shipper’s rate table into a web database.”

Catching up with the API technology train as fast as possible is essential for the survival of the annuity business. Any company that wants to do business on the web, that wants to “bolt-on” third-party services as easily as Lego blocks, and that wants to give customers the fluid experience they expect online, has to use APIs.

The worlds of advice and financial product distribution are clearly headed in this direction, and life insurance companies have to follow. Six annuity issuers—Allianz Life, Brighthouse Financial, Global Atlantic, Jackson National, Nationwide and Prudential—have already begun to integrate with the Insurance Exchange. Others are expected to join later this year.

Walther

“I was just talking about API technology with one of our major distribution partners,” Corey Walther, head of business development and distribution relationship management at Allianz Life said in an interview with RIJ. “We were joking that, a year or 18 months ago, that topic would never have come up, even at large organizations. But here was the president of a distribution firm initiating a conversation about APIs. It’s going to be a requirement in the future.”

They’re just like Lego blocks

Lego blocks and APIs, in fact, are often compared. With APIs, “developers don’t have to start from scratch every time they write a new program,” said an article at thenewstack.io. “They no longer have to build a core application that tries to do everything. Instead, they can contract out certain responsibilities by using already created pieces that do the job better. So APIs are the Lego bricks of software development: standardized tools for software to communicate with other software, leading to faster building and deployment… and faster load times.”

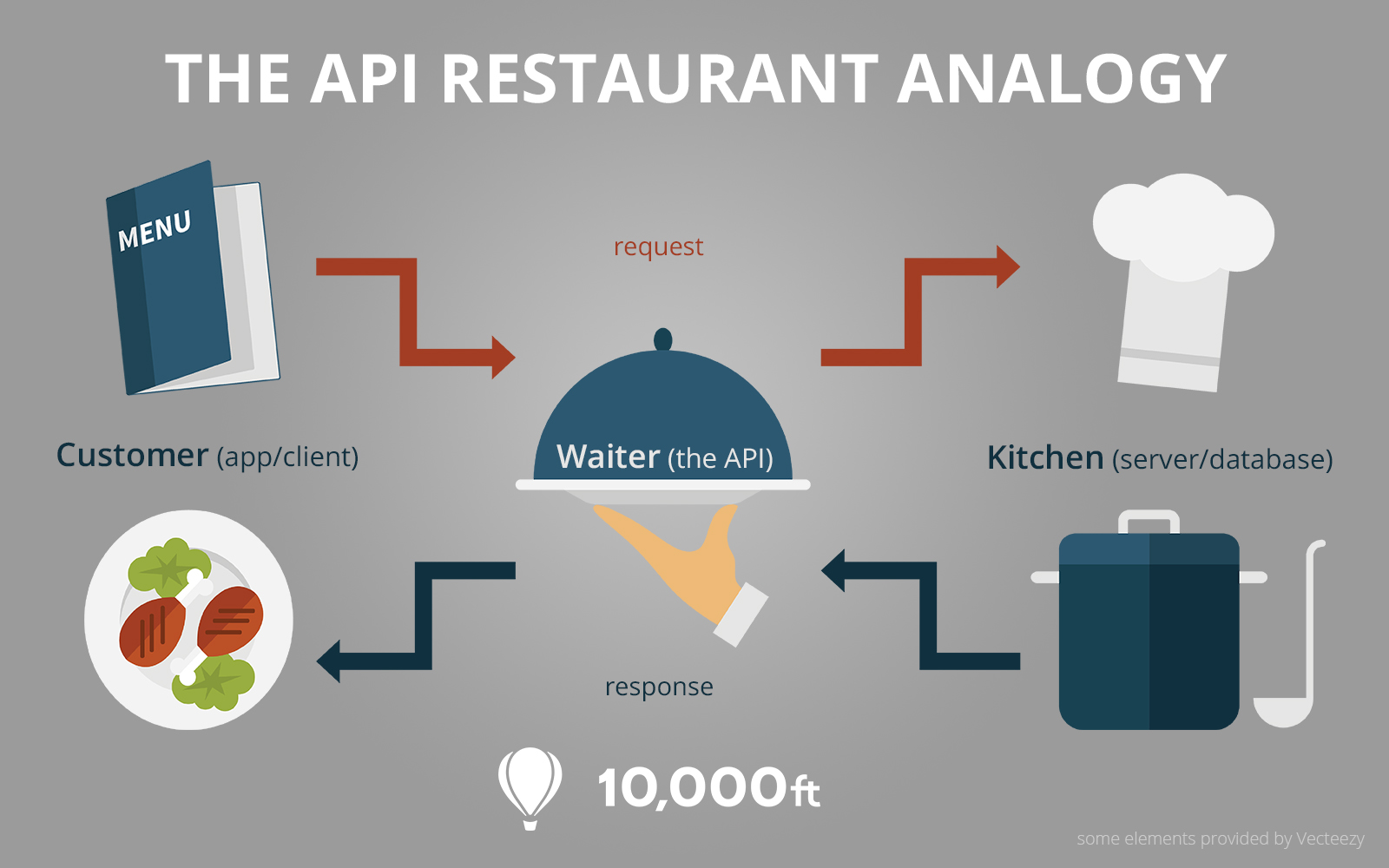

APIs are central to Envestnet’s cloud-based technology strategy. They’re the neurotransmitters that allow advisors to integrate insurance products and investment products on the same web page. They form a network that allows Envestnet to offer clients an á la carte menu of services instead of a prix fixe list. (For the “restaurant analogy” of APIs, click on image below.)

To build the Insurance Exchange, Envestnet first created FIDx, a stand-alone company in Berwyn, PA. FIDx builds bridges—integrations, in developer-speak—between software inside Envestnet and software tools from outside vendors. It often relies on the vendors’ existing APIs to make the connections. For instance, FIDx can integrate Envestnet’s MoneyGuidePro planning tool and Insurance Technologies’ annuity order-entry and illustration tools using Insurance Technologies’ FireLight Embedded API.

“Advisors won’t have to change the way they do business,” Rich Romano, the chief technology officer at FIDx, told RIJ. “Their businesses are enhanced. They can process annuities the same way they process their managed account businesses.”

For example, Riskalyze, the client financial risk assessment tool for advisors, has an API that allows it to integrate with Saleforce or Redfin, two customer relationship management software providers. Advisors can import client data from one to the other without cutting and pasting or re-entering anything. This technology, by now taken for granted in most of the e-commerce world, is relatively new to the annuity divisions of life insurers.

Thanks to APIs, annuity distributors and advisors can use the Insurance Exchange without necessarily abandoning any of their existing current technology partners. It means that advisors have more tools at their fingertips, so that they can more easily offer the comprehensive financial planning that clients want. At a mundane but important level, integration also reduces the cost of rework associated with NIGO (not in good order) annuity applications.

“The ‘north star’ for our vision is that advisors shouldn’t have to duplicate-entry anything,” said Walther at Allianz Life. “They should be able to go from proposal to implementation to monitoring, and it should all be tied together at the household level.”

Allianz Life’s partnership with Envestnet and FIDx “has never been just about selling fee-based annuities,” he told RIJ. “There’s a much bigger game that’s being played. It’s about the ability to bring ecosystems together more effectively. We’re taking asset management and insurance out of their silos.

“We can leverage tools like LifeYield, which shows people how to optimize their Social Security claiming decision and how best to take withdrawals from pre-tax accounts,” Walther added. “Or Riskalyze. We’re exploring integrations with BlackRock iRetire. Envestnet in effect becomes the Microsoft operating system. If you use a different CRM system or a different planning system, you can bolt those on.”

Ganguly

Dev Ganguly, the chief information officer at Jackson National, told RIJ, “We use FireLight as our ‘Intel Inside’ for order-entry and illustration. Those are Lego blocks that we outsource to FireLight. We have other Lego blocks for things like post-issue [services]. FIDx fits together our Lego blocks with Envestnet’s. APIs are the connectors between the blocks. Even today, not many insurance companies think about all the ways APIs approach. At Jackson we have taken the API approach.”

Green fields for insurers

“The carriers have two big boxes they want to check,” said John Yackel, leader of Strategic Initiatives at Envestnet. “First, they want to make their current business more efficient. And they’re telling us, ‘Get me into new markets that I haven’t gone after before.’” That would include the 15,000 advisors in the RIA channel who manage $1.2 trillion. “Annuities have only 3.3% penetration in that market,” he added, “so they look at it as a green field.”

“But it’s not just about fee-based business,” said Ganguly. “We look at ‘fee-based’ as a revenue model but we look at ‘advisory’ as a mindset. We’ll also leverage the power of the platform to do brokerage or commission-based business. The biggest benefit is the fact that two ecosystems, investments and insurance, are coming together. ”

© 2019 RIJ Publishing LLC. All rights reserved.