Overall US annuity sales volumes fell nine percent in 2020, to $219 billion in 2019, according to the Secure Retirement Institute (SRI) US Individual Annuity Sales Survey. But fourth-quarter 2020 sales were three percent higher than in the same period in 2019, at $58.6 billion.

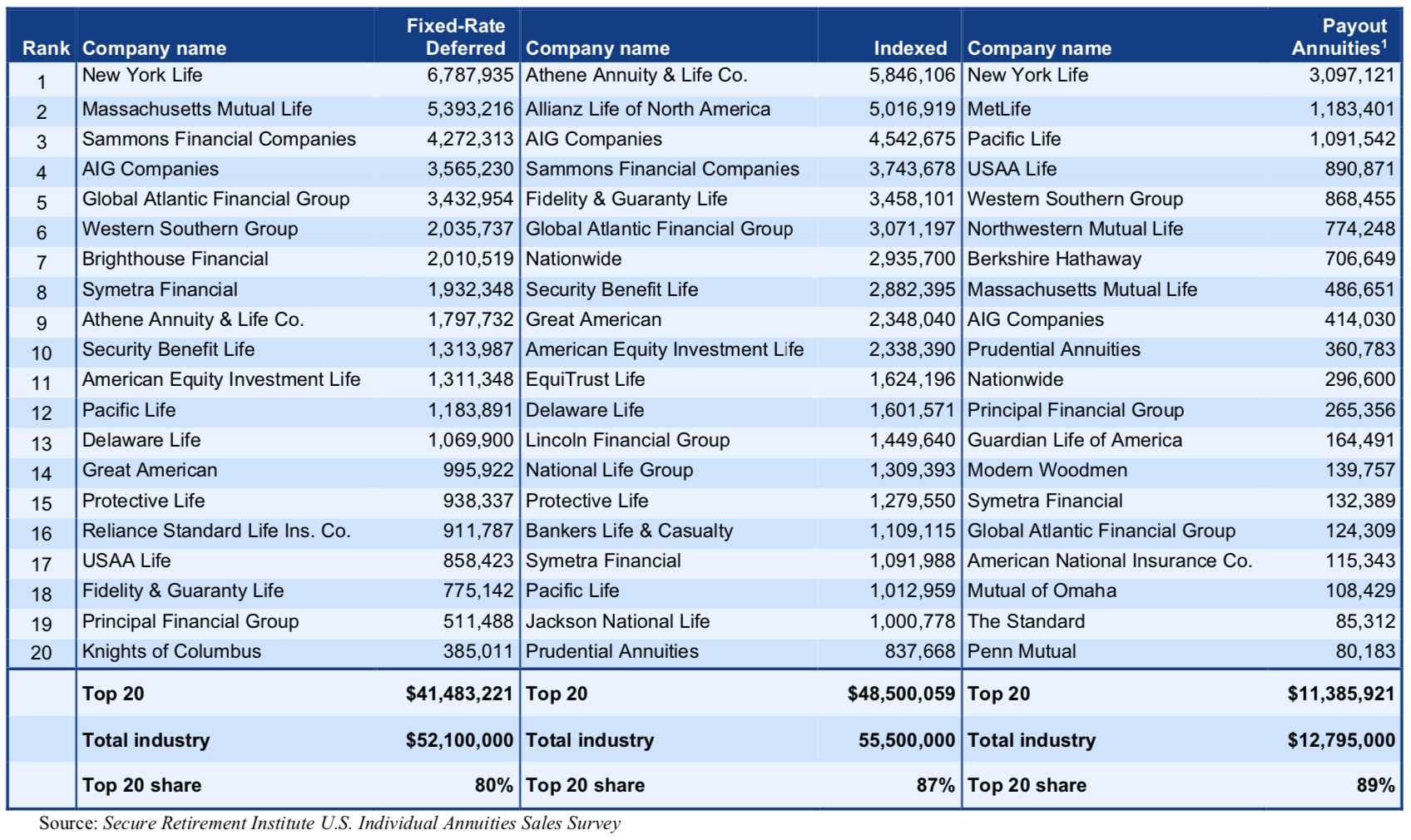

At $55.5 billion, fixed indexed annuities (FIAs) were the top-selling annuity product category. In a sign of the growing clout of asset managers like Blackstone, KKR and Apollo in the FIA business, eight of the top 12 issuers of FIAs in 2020 have partnered or merged with such firms since about 2010.

Those eight issuers are (in order of sales volume): Athene, Fidelity & Guaranty Life, Global Atlantic, Security Benefit Life, Great American, American Equity Investment, EquiTrust Life, and Delaware Life. Together these firms now account for about 42% of the FIA market.

All charts below are for year-end 2020 sales, and are provided by LIMRA SRI. For a detailed year-over-year sales break-out by product category, click here.

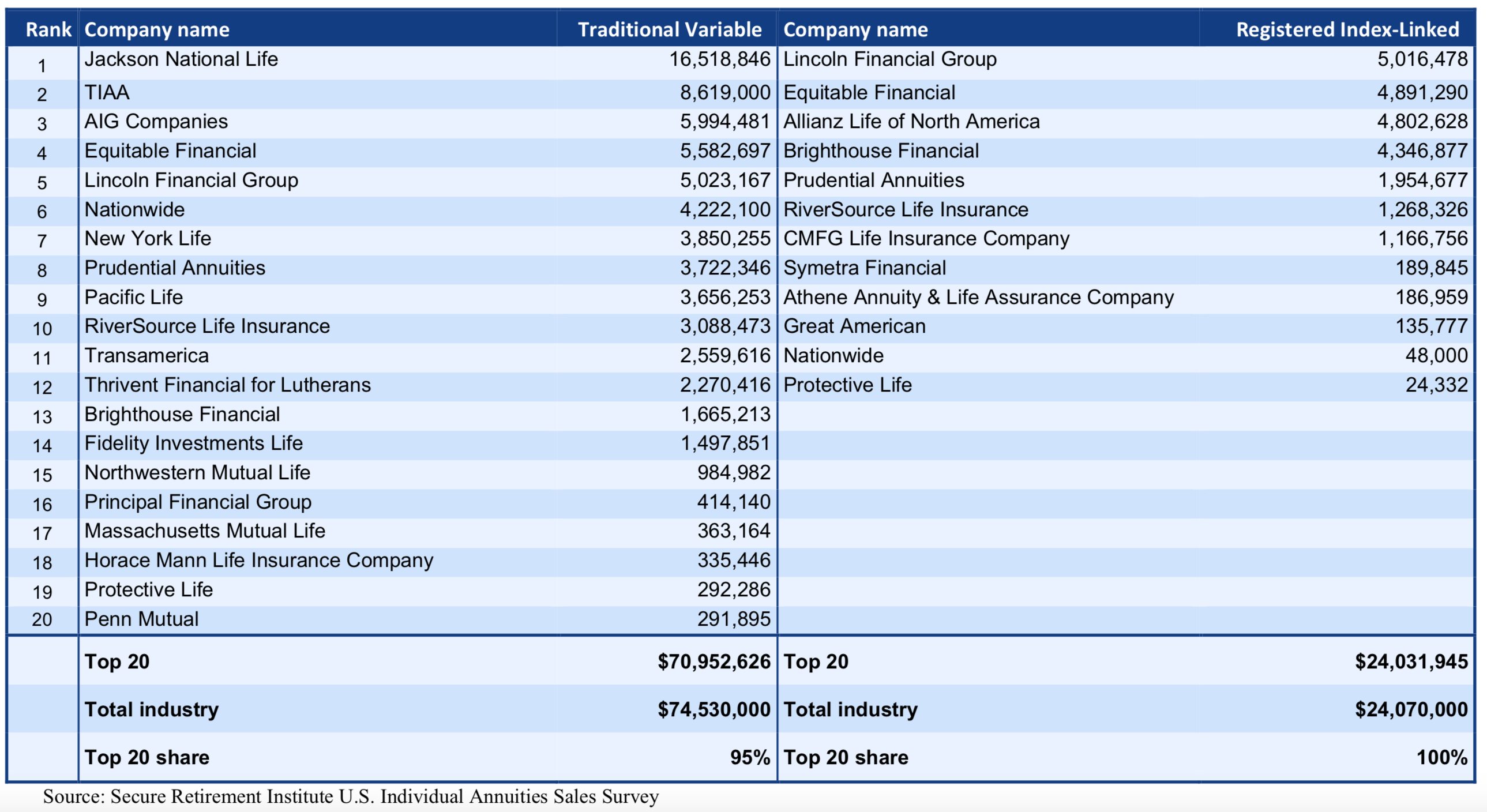

AIG, New York Life, and Lincoln Financial are the three companies with the most equal balance between sales of variable annuities and sales of fixed annuities. In overall annuity sales, they are #2, #3, and #4 after Jackson National. Almost all of Jackson’s nearly $18 billion in sales came from traditional VAs. New York Life is the top issuer of fixed annuities and Lincoln is the top issuer of registered index-linked annuities (RILAs).

RILAs are in a league all their own, with an appeal that probably has nothing to do with the fact that they are annuities. They continued their decade-long climb in sales with a 38% increase in 2020. The other bright spot in 2020 was fixed-rate deferred annuities, with sales up 10% in response to investor jitters.

Just four companies account for about 80% of the $24 billion RILA market. They are (in order of sales volume): Lincoln Financial, Equitable, Allianz Life and Brighthouse Financial, each with over $4 billion in sales. This peloton is followed by Prudential Annuities, RiverSource Life and CMFG (Cuna Mutual), each with between $1 million and $2 million in 2020 sales.

Jackson National, partly on the strength of its Perspective II contract, continues to dominate the sale of conventional variable annuities, where contract owners directly hold tax-deferred versions of mutual funds in separate accounts. (RILA returns are based on the performance of options on the movement of indexes.)

With more than $16.5 billion in VA sales for the year, Jackson National has more than 20% of the traditional VA market. Jackson National has 24% of the individual conventional VA market, since TIAA’s $8.62 billion in VA sales consist mainly of group annuities. Jackson National is in the process of de-coupling from its long-time Asia-focused foreign owner, Prudential plc (no relation to Prudential Financial in the US).

Sales of income-focused annuities—the only annuities that pool longevity risk and offer so-called survivorship benefits—fell 28% because low interest rates raise their prices relative to the amount of retirement income they pay out. Combined sales of single premium immediate annuities and deferred income annuities fell more than 30% each for the year.

A year ago, “The yield on the 10-year treasury fell to 56 basis points and the equities market contracted 32%,” said Todd Giesing, senior annuity research director, SRI, in a release. “Worried investors turned to RILAs and fixed-rate deferred annuities for protection and growth. Protection-focused products represented more than half of all retail annuity sales in 2020.

“The cost of guaranteed income was very expensive under the economic conditions in 2020,” he added. “Investors who would have been in the market for guaranteed income products are likely turning to other annuity contracts—like short-duration fixed-rate deferred products — to wait for interest rates to normalize.”

Part of the growth in RILAs comes at the expense of the variable annuity products with guarantee lifetime income riders, an income-focused product, according to LIMRA SRI. Low interest rates have forced life insurers to lower the payout rates of income riders, which makes the products less attractive.

Despite the year-long bull market in equities, volatility and uncertainty has dampened growth in accumulation-focused products — primarily VA contracts without income riders. Sales of these products, though stable in 2020, have dropped more than 30% since 2015.

© 2021 RIJ Publishing LLC. All rights reserved.