Brent Burns and Steve Huxley of Asset Dedication, LLC, like to compare their retirement income-generating unified managed account methodology to the Apollo moonshot, an event that most Boomers should have no trouble recalling.

The spacecraft’s wobbly moonward path required a lot of course corrections along the way, say the Mill Valley, Calif., entrepreneurs. Similarly, a retirement portfolio won’t adhere to its intended 30-year trajectory without frequent adjustments by an advisor.

That’s one way to describe what they do. But you could also visualize their program as a five-year extension ladder built out of bonds. Each year, if they wish, retired investors and their advisors can keep extending the ladder—presumably until their portfolios are more or less safe from ruin.

“It’s liability-driven investing for individuals,” said Huxley and Burns in a recent interview with RIJ. “We call it Dedicated Portfolio Theory. It relies on the same institutional concepts that foundations and endowments have used for years.”

“It’s liability-driven investing for individuals,” said Huxley and Burns in a recent interview with RIJ. “We call it Dedicated Portfolio Theory. It relies on the same institutional concepts that foundations and endowments have used for years.”

In recent years, entrepreneurs, insurance companies, and even trade groups have introduced a flock of outcome-based, liability-matching planning methodologies for retirement income generation, offering them as potential alternatives to systematic withdrawals from balanced portfolios. Some employ annuities and some don’t.

Huxley and Burns were pioneers in that movement. With their book, Asset Dedication (McGraw-Hill, 2004), they identified the weaknesses of traditional asset allocation during retirement early on. Even earlier, in 2002, they formed a company with the same name, but didn’t signed up their first client until 2007. Now, having allied with BondDesk Group LLC in November, they’re ramping up their marketing.

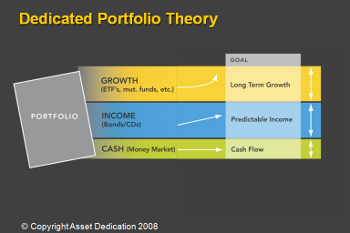

Building a “bond bridge”

To a layman’s ears, Asset Dedication’s UMA sounds like a bucket system that’s built around a proprietary bond laddering technique, coupled with an illustration system and integrated with back office support. It includes a one-year cash bucket, a five-year to 10-year bond bucket, and a long-term equity bucket.

The product’s strongest points, its creators say, are that it can deliver predictable inflation-adjusted income year after year and can be customized for each client. Systematic distributions from a bond fund would be a lot more risky, and laddered zero-coupon bonds or a period-certain immediate annuities would be more expensive, they claim.

“Technically, it’s a bond ladder but we call it a bond bridge,” Huxley told RIJ. “It smoothes out income in retirement. Our algorithm reduces the opportunity costs of buying bonds, so you get the most income for the least amount of money. It frees up resources that you can use to extend the bond-bridge or dump into stocks.”

On the other hand, there’s nothing magical about this methodology. While aimed at creating a rolling buffer zone between a retiree’s market-sensitive assets and his or her monthly cash flow, it doesn’t necessarily exempt advisors or clients from potentially difficult timing decisions during retirement, Huxley and Burns conceded.

On the other hand, there’s nothing magical about this methodology. While aimed at creating a rolling buffer zone between a retiree’s market-sensitive assets and his or her monthly cash flow, it doesn’t necessarily exempt advisors or clients from potentially difficult timing decisions during retirement, Huxley and Burns conceded.

“You may have to take a pay cut,” they acknowledged, if it became necessary to buy (“roll over”) an additional year’s income at a time when the portfolio’s equity investments are depressed. The alternative strategy would be to maintain current spending levels and accept an incrementally higher risk of portfolio “ruin.”

The minimum initial investment in the UMA is $250,000 for a household account and $100,000 for management of the bond assets alone. The fee is 35 basis points a year for the first $5 million invested, 25 basis points for the next $5 million and 15 basis points for money over $10 million. Huxley and Burns say the system is designed for low turnover and high tax-efficiency.

Comparisons to funds and annuities

How would Asset Dedication’s five-year bond bridge compare to a five-year period certain immediate annuity? In one of the firm’s published examples, a hypothetical client receives an inflation-adjusted income averaging about $98,000 a year over the first five years of retirement, for an initial cost of $468,000. By comparison, an annuity that produced $98,000 a year for five years, assuming a two percent annual growth rate and no fees, would cost $471,157, according to an annuity calculator at bankrate.com.

Earlier this year, PIMCO introduced a TIPS-based payout fund that provides predictable inflation-adjusted income for 10-year or 20-year intervals. Huxley and Burns were asked to compare it to their product.

“Pimco’s funds are designed as a mutual fund for thousands of clients,” Burns said. “Our strategy generates income specific to each client based on their financial plan. We match the cash flows needed—usually to within one percent—and do this dynamically through the use of rolling horizons. We can use TIPS, Treasuries, AA or better corporate, or munis.

“The best and cheapest solution shifts over time as the spreads between the different fixed income securities change,” he said. “There are times when it is much more expensive to generate the same income profile using TIPS. Right now they are relatively cheap, but two years ago, they were expensive and we have certainly seen them shift that way over the last few weeks.”

But couldn’t an advisor build his or her own bond ladder? “It is not as easy as it sounds,” said Huxley, who teaches at the University of San Francisco School of Business and Management. “Determining the precise number of bonds to buy so as to match cash flows over a period of years can be extremely difficult and time consuming, particularly if cash flows are not steady.”

If investors want to avoid the stress or risk of funding five years of retirement income all at once when they retire, the Asset Dedication system allows them the option of buying a series of five-year bonds, starting five years before retirement.

Target market

Independent fee-based advisors, as opposed to registered reps, are Asset Dedication’s target market. “We dovetail with people who are true financial planners, who are the financial quarterbacks for their clients who provide comprehensive advice, not just investment advice,” Burns said.

“We’re just a piece of what they do. They drive the strategy and we drive the implementation. We can’t build our portfolios unless there’s already an investment plan in place,” he added. Asset Dedication has made several presentations to NAPFA (National Association of Personal Financial Advisors), an organization of fee-only advisors.

Advisors should feel at home with Asset Dedication’s choice of strategic partners. Its affiliation with BondDesk Group, begun last month, gives Huxley and Burns access to a large inventory of bonds. (Also based in Mill Valley, Calif., BondDesk is described by BusinessWeek as an odd-lot fixed-income electronic trading platform for broker dealers in North America.)

The low-fee custodians of the UMAs—Schwab, Fidelity and TD Ameritrade—are obviously familiar to advisors. For the equity bucket of their system, Asset Dedication relies on investments managed by Dimensional Fund Advisors (DFA), which sells low-cost funds only to select advisors.

© 2009 RIJ Publishing. All rights reserved.