Motoring past the red-gold grain fields of the Mississippi valley a decade ago, Iowa insurance man Curtis Cloke cultivated an idea that would soon make him very successful and, in the process, demonstrate that Americans will buy guaranteed income if you spin the right story around it.

His idea is as simple as the difference between “wheat” and “chaff,” apparently. And it champions a hitherto obscure insurance contract, the deferred income annuity.

Since 1999, Cloke has used his Thrive Income Distribution System to sell about $20 million worth of deferred period-certain income annuities (DIAs) to about 200 clients. He and RISE Enterprise, the retirement consultants, have packaged it into a scalable sales program that they are now offering to insurance marketing organizations.

Starting this month, some 23,000 insurance producers associated with Crump Group, Inc., the organization formed by the 2007 merger of Crump Insurance and BISYS, will be able to use it. Crump Group identifies itself as the largest insurance wholesaler in the U.S.

“I say ‘bull’ to people who say income annuities aren’t marketable,” said Cloke from his cell while driving in the Quad-City area of eastern Iowa and western Illinois. A “Top of the Table” member of the Million Dollar Roundtable, Cloke started out as an advisor with Prudential Financial in 1987.

“In 1999, I became somewhat fearful about what I saw happening in the tech sector,” he told RIJ. “A number of potential clients were bitten by the tech crash, and I decided there must be a better way to secure income and perpetuate accumulation in retirement. The solution was to separate the assets and allocate portions to income and accumulation prior to retirement.”

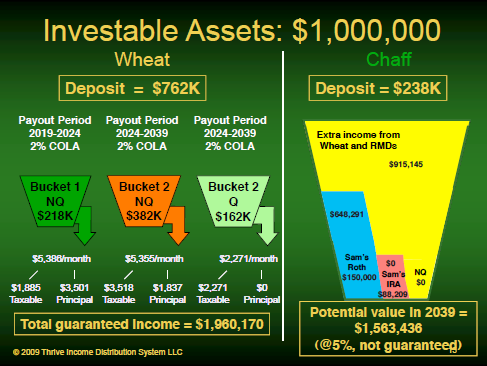

In broadest terms, the Thrive system involves dividing a client’s savings into two parts, which it calls the “wheat” and the “chaff.” The client uses about 75% of the total, to build an income floor with a ladder of income annuities. That’s the wheat. He invests the rest in mutual funds for upside potential, emergencies, splurges or bequests. That’s the chaff.

It’s a variation on the old laddered annuity system. But instead of waiting until retirement to buy an immediate income annuity, Cloke’s clients start 10 years early. At age 55, for instance, they lock in income streams that will them a handsome income from age 65 to age 85.

Here’s an example from Thrive’s literature: A hypothetical 55-year-old has $1 million, including $600,000 in non-qualified accounts, $250,000 in qualified accounts, and $150,000 in a Roth IRA. He wants to retire at age 65 and expects to live until age 85. He needs $7,500 a month in retirement, of which Social Security will provide $1,625, plus annual cost-of-living increases.

The Thrive client spends $218,000 of his nonqualified money on a deferred five-year period certain income annuity that pays $5,386 per month with a 2% annual inflation adjustment starting ten years from now, and another $382,000 on a deferred 15-year period certain annuity that pays $5,355 per month starting in 2024. With $162,000 in qualified money, he buys a 15-year annuity that pays $2,271 per month from 2024 to 2039. The rest of the qualified money and the Roth IRA assets stay in mutual funds or cash.

This system touts several plusses. First, it allows a 55-year-old to eliminate sequence-of-returns risk by locking in 20 years of guaranteed income. Second, there’s 30% discount associated with deferring income for 10 years or more relative to a SPIA, according to a comparison with a Vanguard income annuity.

A 65-year-old client applying to Vanguard for a five-year, period-certain SPIA with a 2% inflation adjustment that pays $5,386 per month would be quoted about $313,280, or about $95,000 more than the person in Thrive’s example who postponed income from his five-year annuity for 10 years. (Quotes obtained from Vanguard’s online calculator June 1.)

Third, Thrive’s period-certain DIAs have predictable yields, which life annuities don’t. The contracts pay out during the designated period, no matter what. Clients can arrange for a lump-sum commuted payment for beneficiaries instead of a monthly income, if they wish–but Thrive doesn’t call it a death benefit. If all owners die during the income period, their beneficiaries receive the remaining payments.

“It’s an investment play, not an insurance play,” Cloke said. “You’re buying an income based on a rate of return, whether you live or die. In this case, the longer you defer, the higher the return.” The internal rates of return range from 4.5% to 7%, he said.

Cloke believes that his system extracts more income from an initial investment than a variable annuity with a guaranteed living benefit. “We’ve looked at the annuitization rates of GMIBs (guaranteed minimum income benefits) and we’ve looked at the GMWB (guaranteed minimum withdrawal benefits). When you look at the payout they’ll produce as a cost of present value, they all require more present value than you’d need in the DIA,” he said.

There are other wrinkles to the program, such as tax and RMD strategies. Depending on a client’s preference, Thrive may also combine period-certain annuities with life insurance and/or pure longevity insurance that pays life-contingent income beyond age 85. But the essence of the product is the ladder of consecutive or overlapping period certain deferred income annuities, or DIAs.

So far, several life insurers, including Hartford and Symetra, offer DIAs or plan to, according to Garth Bernard, president of THRIVE and partner in RISE Enterprises, which built the Thrive software and marketing materials. Other carriers are considering offering DIAs, he added. “No other IMOs are selling these products. We’re creating a new market.”

Symetra, whose DIA is called the Freedom Income annuity, is bullish on DIAs. But the company’s annuity marketers have learned that it’s easier to sell a DIA with a death benefit (or, as in Thrive’s case, similar protection) than to sell a life-contingent DIA, even though a death benefit can add “30% to 60% to the price,” said Rich Lindsay, senior vice president of the Life and Annuities division at Symetra Financial.

“We created an earlier deferred income annuity as a non-death benefit product, but the feedback from the field was that [life-contingency] is a tough hurdle to overcome—although less so in the last six months” as a result of investors’ flight to safety, he added.

Even with a death benefit, a DIA strategy is cheaper than, say, buying a 10-year fixed-rate deferred annuity and then annuitizing it on a 10-year period certain basis. Symetra, which is part-owned by Warren Buffett’s Berkshire-Hathaway, thinks DIAs have a big future. “We’re putting a lot of emphasis in our distribution system behind these concepts,” he said. “There will be other good ones coming down the pipe.”

Moshe Milevsky, the York University finance professor who has written widely about retirement income creation, gives two cheers to Thrive.

“I think [Garth] has approximately 66.6% of the solution worked out,” Milevsky said. “Mutual funds and ETFs will continue to be a very important first component of income planning. Income annuities, both life-contingent and period certain, will be the second component. To that end, you can build fancy ladders, simple SPIAs, ALDAs or some combination of these.

“However, I think such an approach is missing 33.3% of the retirement income solution. In my opinion the third and missing leg is variable annuities with guaranteed living income benefits, or GLiBs. Or, if you don’t want to buy a variable annuity per se, you can buy pure put options or other true downside protection,” he said.

Not just any variable annuity issuer will do, Milevsky added. “The caveats are three: credit risk, increasing fees, and asset allocation restrictions. Make sure [to the extent possible] that the company backing the GLiB will remain in business for the 30-year duration of the contract. Make sure they can’t increase fees to existing policyholders, and make sure they can’t change your true asset allocation after the fact, by acquiring more bonds, less equity, etc.”

“We believe that [Dr. Milevsky] missed the point,” said Bernard after learning of the York University professor’s comments. “Thrive provides complete flexibility to incorporate an advisor’s favorite vehicles in the ‘Chaff’ component. In other words, a VA with GLWB, protected growth instruments, target date funds or any favored income or accumulation vehicles can be installed in the Chaff component.”

© 2009 RIJ Publishing. All rights reserved.