In November 2008 Her Majesty The Queen visited the London School of Economics to open a new building. During a briefing on the calamitous chain of events that had recently brought the global financial system to near ruins, the Queen asked, “If these things were so large, how come everyone missed them?” Quite.

A few months later a broad group of leading academics, politicians, members of the Bank of England, finance journalists and investment bank economists attempted to answer the question in an open letter to the Queen.

Any attempt, in just two-and-a-half pages, to admit all the hazards in the run-up to the Great Financial Crisis (GFC) could hardly be called definitive, but the authors made a decent and honest stab at it. They zeroed in on four areas:

- The global savings glut—as they called it—and very low returns on safer long-term investments which led many investors to seek higher returns at the expense of greater risk

- Inflation remained low and gave no warning sign the economy was overheating

- The failure to see collectively a series of interconnected imbalances over which no single authority had jurisdiction, combined with the psychology of herding and the mantra of financial and policy gurus

- And ultimately that the crisis was principally a failure of the collective imagination of many bright people (their words), globally, to understand the risks to the system as a whole

So, perhaps inadvertently, Her Majesty helped in the very public debunking of several myths at once. (Click here to see the unabbreviated original article.)

The situation today

Although the letter slayed a few of the myths of policy-making (and efficient markets) that unravelled in 2008, surveying the investment landscape today one cannot help but wonder if others have proved more enduring. There are aspects of the world today that will feel eerily familiar to investors who lived through that crisis.

One striking lesson from 2008 was that the price stability targeted by central banks did not, in itself, generate financial stability. That is, a period of very low and stable inflation did not lead to a new era of financial prosperity. In fact, a long period of macroeconomic stability and exuberance in asset prices and credit markets helped build up instability in the financial system.

Many central banks in the world support an even more activist approach to price stability today (their inflation targets) than in the run up to the GFC. This trend quickened during the global pandemic as central banks, rightly, gave life support to economies in lockdown.

But if the financial cycle is heavily influenced by monetary policy, then that influence is far greater today than before the GFC. It would be extremely dangerous to assume that very easy monetary policy today does not bring the potential for broad macroeconomic shocks later.

I do believe that central banks are completely alive to these risks and that the bad side effects of unconventional monetary policy for financial stability (and inequality) are important in their thinking around policy choices. In a world of below-target inflation and zero policy rates the idea that ‘There Is No Alternative’ means central banks (and therefore we) walk a tightrope. Sometimes, the problem is just knowing when to stop.

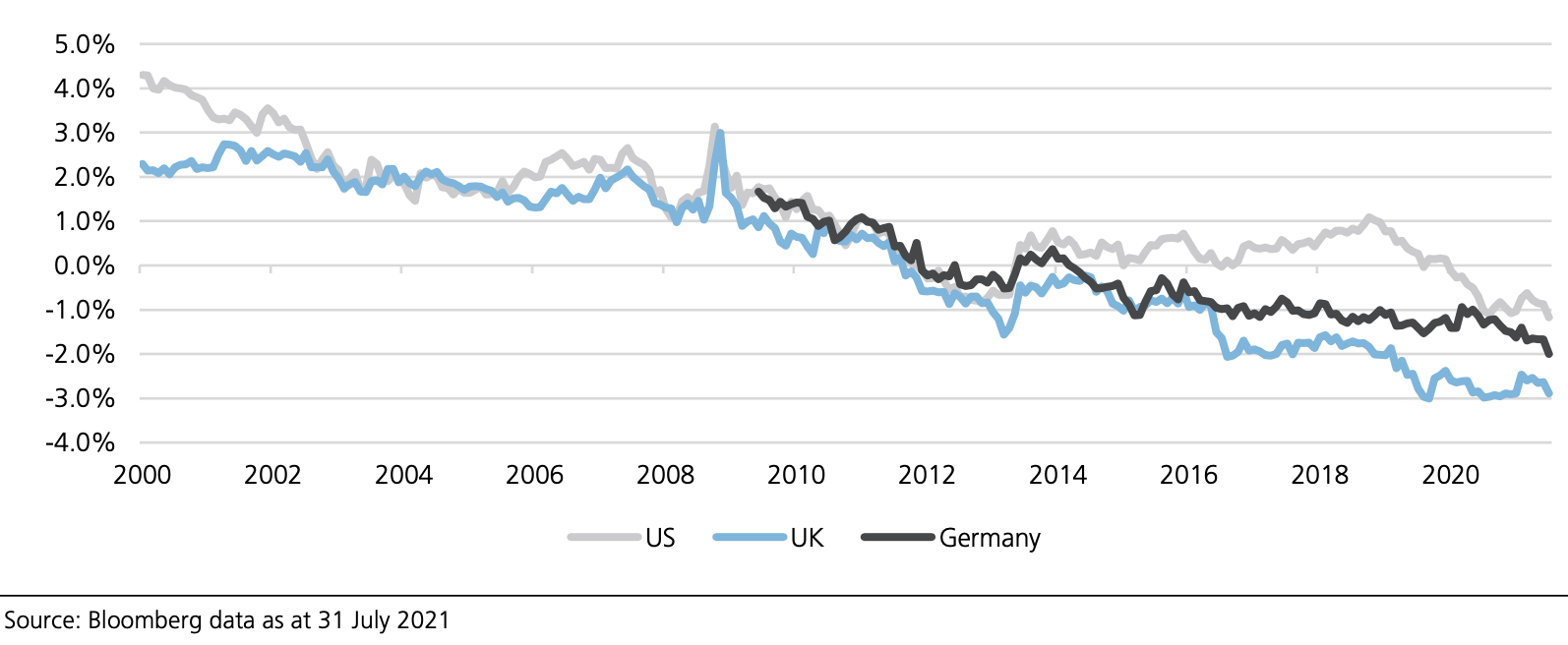

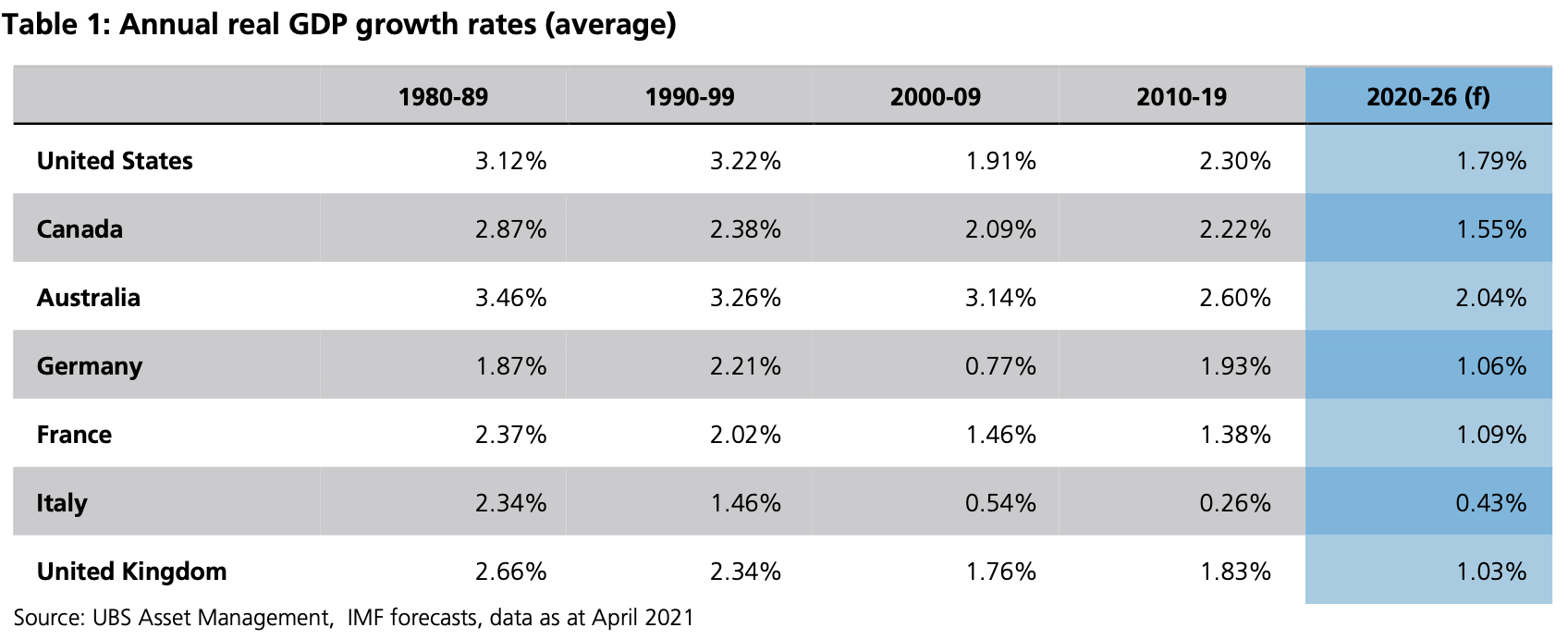

As the chart below illustrates, the global savings glut is still a fact of life; private sector savings exceed desired investment, and so drive very low interest rates. It has been a key reason behind progressively lower real growth rates around the world over the last 30 years. I referred to Table 1 earlier this year to make the same point that, based on IMF data, average forecast growth rates from 2020-26 will be lower than each of the preceding four decades. In the IMF’s view, developed economies will be facing the challenges posed by low aggregate demand for many years to come.

US, UK and German 10-year real yields

Don’t zig-zag

So, in summary, we must learn to live with an expansive monetary policy framework with a relentless focus on price stability that might in fact contribute to systemic risk: Very low real growth rates and associated yields that drive investors out along the risk curve; and global imbalances that in some ways are larger than 2008 and still unresolved.

To be fair, meaningful steps have been taken to clean up some risks. For banks, this means stronger solvency levels, counter-cyclical capital buffers, liquidity and stress tests to help build resilience. Centralized clearing and better reporting have helped reduce risks in some derivative markets.

But ongoing innovation brings risk and complexity anew. The central banks and regulators that drove these reforms had probably not imagined the crypto-exchange traded funds, meme-stocks, high-frequency algo-trading, weapons-grade day-trading accounts and SPACs to come. Markets are not always in equilibrium or efficient, but can be opaque and interlinked in ways that are not fully imagined by regulators, policymakers and investors. High leverage, funding mismatches, complex and opaque funding structures and off-balance sheet liabilities create problems for the assessment of market efficiency.

Perhaps there is an even more fundamental problem. If asked, many people in the US, UK or Europe would describe their economies as capitalist, or market economies, where pricing and investment flow from the interactions of private citizens and businesses for profit. I just wonder how valid a description that can still be, in a world where:

- The combined balance sheets of major central banks total $25T

- Bond markets are routinely used as a policy tool

- Prices and yields are no longer set by a freely trading liquid market based on fundamentals

- Some economies teeter so close to deflation that aggressive monetary expansion is the only answer

- Bad news on the economy can lift markets in expectation of more central bank largesse

It is not to say these interventions are wrong, far from it — much of the GFC and pandemic response was crucial — it’s just that, given how deep and structural in nature the challenges are, we may even be in the process of rethinking what capitalism actually means.

Of course, identifying and writing about these risks is one thing (the easy thing) but knowing when and in what form they will show, quite another. For now, I advise staying with some time-honored approaches: diversification, avoiding the overly complex or the ‘black-box,’ being wary of leverage in illiquid positions, stress-testing portfolios and staying alive to the changing environment. Keep to a straight line, not a zig-zag.

© 2021 UBS. Adapted by permission.