Chris Blunt has held C-level positions in asset management, marketing or annuities at Merrill Lynch, New York Life and other top firms over a 34-year career. In 2018, he became CEO of Blackstone Insurance Solutions. About a year ago, he became president and CEO of Fidelity & Guaranty Life.

That makes Blunt, who is 58, well-qualified to comment on the evolution of the life/annuity industry since the Great Financial Crisis of 2008, and on the new business model that some companies, including F&G, have adopted. RIJ calls it the “Bermuda Triangle” model. The businesses call themselves “insurance solutions” providers.

It’s an investment-driven model. Powerful asset managers like Blackstone Group, Apollo Holdings, and KKR are helping certain insurers invest a portion of the assets backing their in-force fixed or fixed indexed annuities (FIAs) in relatively high-yielding, illiquid, long-dated asset-backed securities, or ABS. The asset managers are partnering with life insurers or making equity investments in them.

The asset managers make customized “leveraged loans” to high-risk borrowers, and/or bundle those non-investment grade loans into securities called collateralized loan obligations, or CLOs. Life insurers then buy the senior, investment-grade segments (“tranches”) of CLOs—which pay higher returns than the high-rated corporate bonds that make up a large chunk of a life insurer’s assets.

Chris Blunt

This strategy, especially when linked to the sale of troubled blocks of in-force annuities to offshore reinsurers, has helped mitigate the damage dealt to certain life insurers by a decade of low returns. Some annuity veterans worry, however, that while solving problems for annuity issuers, asset managers are bringing an overly aggressive style to the historically cautious life industry, that CLOs might prove too risky for life insurers to buy and hold, and that private equity culture may not be policyholder-centric enough.

An insider’s view

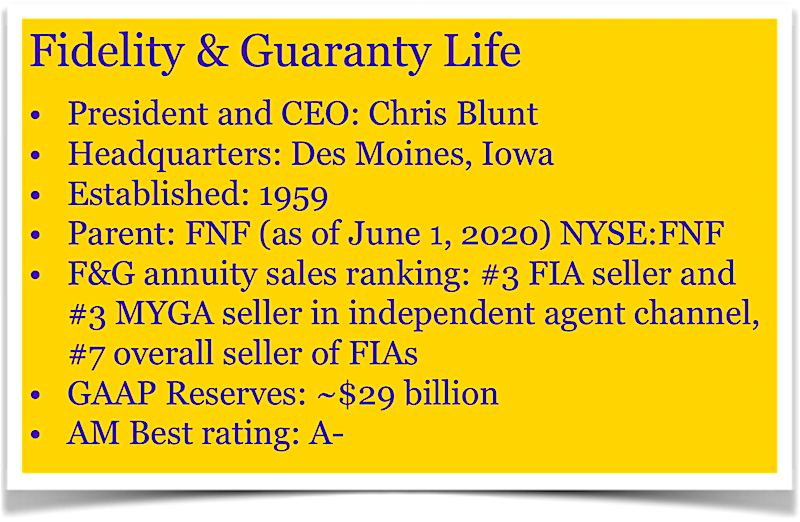

Fidelity & Guaranty Life (F&G)—built on the old USF&G and recently acquired by FNF, the title insurance giant—didn’t pioneer the “insurance solutions” strategy. (Apollo and Athene did, in 2010.) But, working with Blackstone, F&G has used the strategy to become the #3 FIA seller in the independent agent channel, where half of all FIAs are sold. It has nipped market share from established FIA issuers like Allianz Life, American Equity, and Great American.

Blunt recently talked with RIJ about F&G and Blackstone and about the insurance solutions business. Although private-equity companies created this new business, Blunt said, making private equity purchases isn’t the chief skill they bring to annuity issuers. It’s their ability to create private credit.

By buying bank loans or placing bespoke loans to businesses with weak credit ratings but real assets (like machinery or cellphone towers) or contractual cash flows (from, for example, music royalties), F&G can add 20 basis points to the average return of a life insurers general account investments, producing 5% to 10% more investment income. That’s a meaningful competitive advantage, especially when pricing fixed indexed annuities in a low interest rate environment, consulting actuary Tim Pfeifer told RIJ.

Questions and answers

Questions and answers

RIJ: F&G was a public company when CF Corp.—a company started and financed by William P. Foley III, owner of FNF title insurance, and Chinh Chu, a former co-chair of Blackstone’s Private Equity Group—bought it from HRG Group, formerly Harbinger, for about $1.84 billion in 2017. FNF took F&G private this year and CF Corp became FGL Holdings. How would you describe F&G as it stands today?

Blunt: We’re a life and annuity company, and we have been from our beginning as US F&G Insurance. The company used to be bigger in life insurance than it is today. Now we’re overwhelmingly a fixed deferred and fixed indexed annuity company.

RIJ: What inspired Foley and Chu to buy it?

Blunt:At the time [2017], everyone was aware of how Apollo had partnered with Athene. CF Corp. said to Blackstone: You guys have access to even bigger fixed income opportunities than Apollo does. As such, F&G should be able to become even more successful as a life and annuity company than Athene/Apollo, given Blackstone’s ability to source attractive investment-grade private debt.

RIJ: At what point did you get involved with this project, and in what capacity?

Blunt: I was hired by Blackstone in Jan 2018 and tasked with building a third-party asset management unit serving insurance companies. They knew I understood the nuances of both insurance and investments. By the fall of 2018, they saw that the key to success in the US would be to help scale F&G. At the same time, the board of F&G approached me about becoming CEO. So I left Blackstone (with their blessing) entirely at the end of 2018 and in January 2019 I became the CEO of F&G.

RIJ: What enticed you to make the move?

Blunt: It was a difficult decision to leave Blackstone, but I knew what Blackstone’s impact on the investment portfolio of F&G would be. I knew they could give F&G at least a 20 basis-point investment edge. I knew that was unbelievably meaningful, and I liked the size of the company, and the executives I had come to know there. So, in January 2019, I became CEO.

RIJ: And why did FNF decide to take F&G private this year?

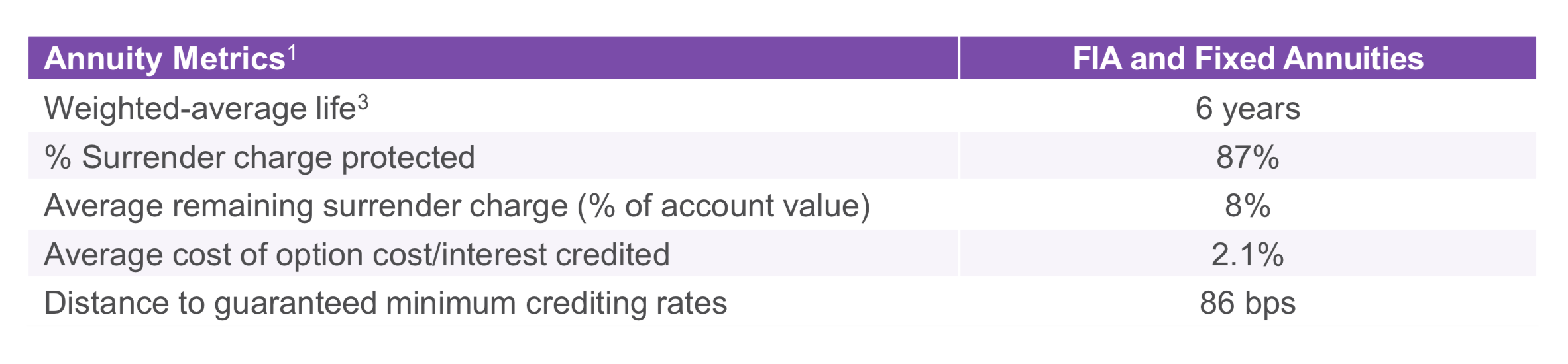

F&G’s annuity business; source for charts: F&G 6-16-20 presentation.

Blunt: FNF’s insight was, ‘We’re currently the largest provider of title insurance. We do title insurance well and do really well in a low rate environment, but eventually rates will rise.’ In addition, FNF felt F&G would have a harder time raising capital in a low rate environment as a standalone company. So its thought was, ‘Why don’t we buy F&G?’ It’ll provide a buffer to FNF when rates rise, and FNF can help scale it faster.

RIJ: It feels like a number of life insurers are becoming sources of stable investment capital for private equity companies.

Blunt: It’s misleading to refer to the new wave of life insurers as ‘private equity-led.’ The relationships between the asset managers and life insurers have taken a variety of shapes. For instance, a private equity holding company might own or have stakes in the insurance company itself or simply manage part or all of their general account. Or, as in one case, a life insurer partners with two or more asset managers. Each relationship is structured differently. In the case of F&G/FNF, FNF and Blackstone have had close dealings with each other, but are completely independent entities.

RIJ: So private equity companies are not at the center of this model?

Blunt: We’re talking about the private-credit arms of the private-equity companies. Rather than taking equity positions in high-risk companies, the asset managers like Blackstone, which re-deploy fixed annuity investments, are more likely to buy or originate private investment grade loans as well as package below-investment grade loans into CLOs and sell the investment-grade senior tranches to life insurers.

RIJ: I see.

Blunt: The question we ask asset managers is, ‘Do you have access to unique private debt deals that are investment grade?’ Not everyone can do that. You have to be in that private deal world, and you need lots of people with specific expertise. Blackstone knows how to access these deals and, more importantly, how to analyze them. If you asked, ‘What’s the most impactful part of this business,’ that’s the most important piece.

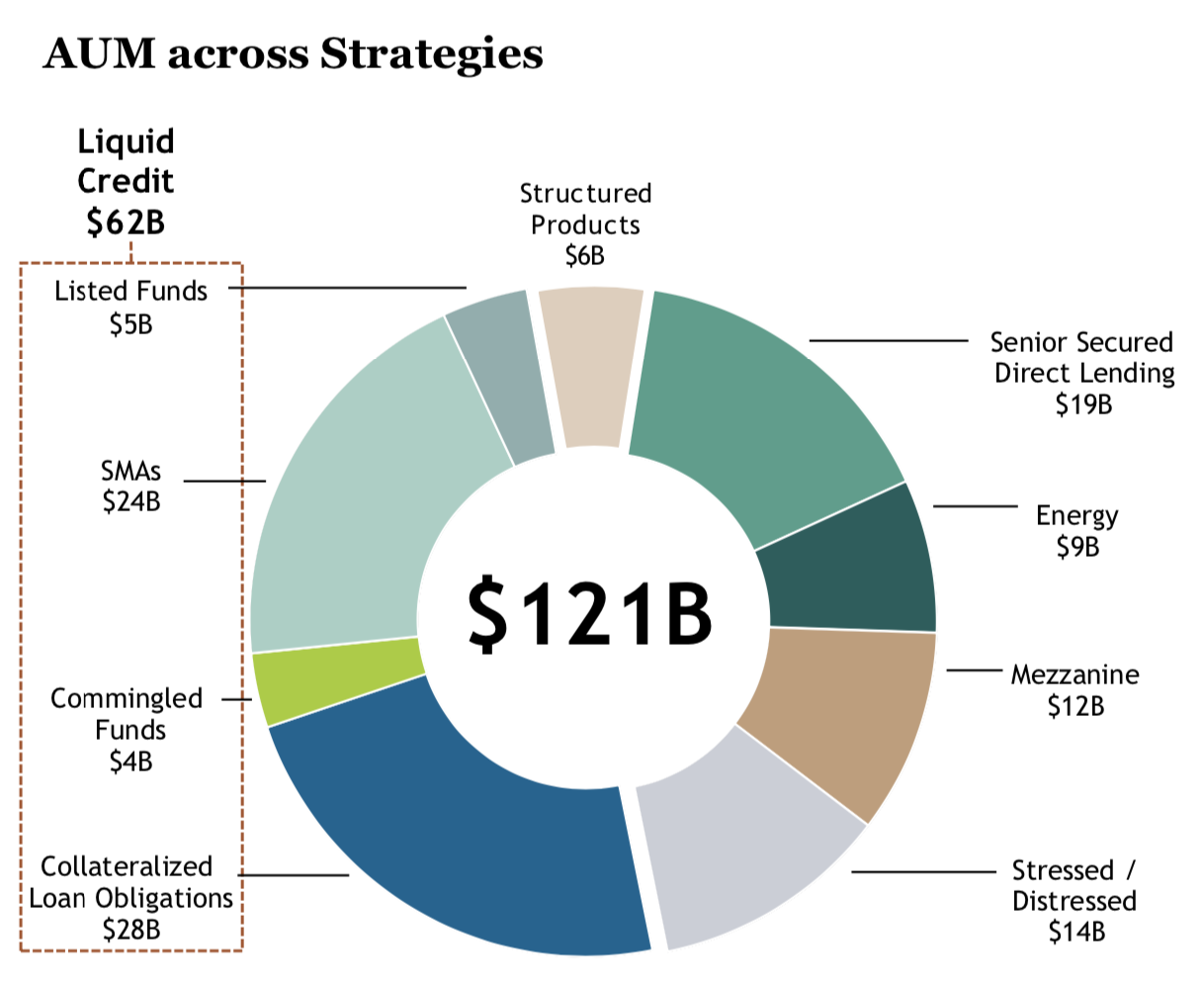

Blackstone’s assets under management

RIJ: Impactful in what way, exactly?

Blunt: Maybe I pick up 20 basis points in total yield right there. We’re not taking more credit risk, but rather liquidity risk. They’re typically 4-5 year loans that are not easily tradable. By investing in private loans and structured securities, we’re picking up an illiquidity premium, a complexity premium and a size premium.

RIJ: So exactly how does this play out?

Blunt: Rather than wait for the phone to ring on a public deal, F&G will go to Blackstone Insurance Specialty Finance for example and say, ‘We want to place $1 billion in a diversified portfolio of loans, we want investment grade, we want no more than Y percent in BBB, with an average duration of X.’ Within those parameters, Blackstone goes out and sources deals for us.

RIJ: What’s Blackstone’s appeal to those borrowers?

Blunt: For a $300 million to $400 million loan, those borrowers wouldn’t go to a big investment bank. It’s too small a loan to be worth [the big banks’] while and they would, appropriately, charge a mark-up. Whereas Blackstone can say, ‘We have multiple insurance clients who would love this kind of yield/credit profile.’ The assets backing these deals can range from cellphone towers to machinery to music royalties—anything with real assets or contractual cash flows. Blackstone says, ‘Work directly with us and we’ll get all of your financing done in one place.’

RIJ: Why is it hard to find those deals? Can’t Blackstone just go into the bond market to find assets for F&G?

Blunt: The investment-grade public deals are massively oversubscribed. If we were F&G in the old days, a big life insurer would have already soaked up all the attractive investment-grade deals that were available [before we could get to them]. I’m not picking on the big insurers, but this is the dilemma in insurance.

![]() RIJ: Which tranches of asset-backed securities does F&G buy?

RIJ: Which tranches of asset-backed securities does F&G buy?

Blunt: With F&G, Blackstone is looking mainly for investment-grade debt tranches. As a life insurer, we can’t own more than five percent in non-investment grade debt. That means 95% of our fixed income is investment grade. Blackstone can originate private asset-backed loans and can choose to securitize them or not. Blackstone can, for example, manage a portfolio of CLOs for us that includes Blackstone-structured CLOs as well as CLOs from other CLO creators.

RIJ: What’s your response to academics and others who feel that CLOs are too risky for life insurers?

Blunt: A lot of people don’t like securitized products. They say, ‘Oh, this could be the next disaster.’ But a single CLO has hundreds of loans from a variety of industries. They’re senior financings; which means, as the creditor, I can liquidate your property if I have to. Frankly, we believe it’s a better risk than an unsecured BBB bond from a single company in a single industry.

RIJ: So, is F&G buying BBB tranches of CLOs?

Blunt: Mainly we’ve bought the single A tranches of a CLO. The BBB grade clearly has more risk whether it’s a CLO or a bond, but we haven’t seen massive downgrades or defaults on them. I’d rather own a BBB tranche of a CLO than a BBB corporate. So where does all the handwringing come from? There’s no historical basis for it.

RIJ: Thank you, Chris.

© 2020 RIJ Publishing LLC. All rights reserved.