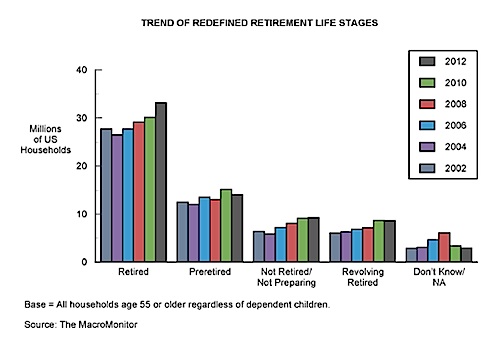

You’ve heard of the revolving-door syndrome. Now a “Revolving-Retired” syndrome has been identified.

According to a recent edition of The MacroMonitor, a publication of SRI Consulting-Business Intelligence, Revolving-Retired households are those with a primary head age 55 or older who has gone from full-time to part-time work, or has retired and returned to the workforce, or has retired and plans to return to the workforce. Heads of households with less than $100,000 in savings and investments and those who rely on Social Security for most of their retirement income are most likely to fit this description.

This may represent a new market niche. According to SRI-BI, “A gap exists between the products and services that financial institutions offer to pre-retired and retired households and the needs of Revolving-Retired households. As retirement evolves into a more flexible yet complicated life stage, financial services providers could benefit from understanding the multiple stages of retirement better.”

Some Revolving-Retired households, as well as households preparing for retirement, continue to support dependents; households with dependent children no doubt postponed forming families in their thirties, The MacroMonitor said.

© 2013 RIJ Publishing LLC. All rights reserved.