The economic expansion just celebrated its ninth birthday and is far healthier today than it has been in some time. It has shrugged off two years of stagnation and is chugging along at nearly a 3.0% clip. At this time next year, it will enter the history books as the longest U.S. expansion on record.

But the naysayers continue to see a dark side. They believe that the recent stimulus from tax cuts and deregulation will prove to be temporary. Furthermore, there is a widespread consensus that the next recession will occur in 2020.

Not so fast. As we see it, good policy and rapid technological advancements can keep the economy humming for some time to come. While it will eventually end, the end is not yet in sight.

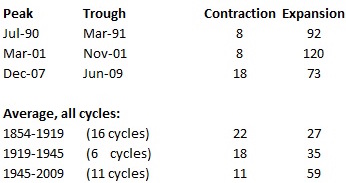

It does not always feel like it, but policy makers have gotten better at extending periods of growth. Between 1850 and 1900 a typical business cycle lasted four years to two years of expansion followed by two years of recession. But in the eleven business cycles since the end of World War II the average expansion now lasts six years followed by a one-year recession. Expansions have gotten far longer, and recessions do not last nearly as long. That was not an accident. Why? Good policy.

In the past 50 years economists’ understanding of macroeconomic policy has gotten better. Policy makers at the Fed have gotten smarter. They seem better able to determine the level of interest rates required to keep the economy on track. Fiscal policy has also improved, and economists better understand the impact of government spending, tax, and trade policies on the economy. Good policy can extend the life expectancy of an expansion.

For example, not long ago the unemployment rate was 5.0%. Most economists thought that the labor market had reached full employment and worried that wage pressures and inflation would soon rise. But Janet Yellen and her colleagues at the Fed argued that there were still many “underemployed” workers who wanted full time jobs but could only get part-time employment. Hence, the Fed concluded that the economy was not yet at full employment and it elected to raise rates very cautiously for the next 15 months. The Fed got it right. Smart implementation of monetary policy prevented the Fed from prematurely raising rates and inadvertently choking off growth.

In 2015 and 2016 the economy grew at rates of 2.0% and 1.8%, respectively. Business leaders were frustrated by the political gridlock in Washington. They lacked confidence and chose not to deploy their vast cash holdings on new technology or to refurbish the assembly line.

Recognizing the lack of investment, Trump campaigned on a promise to lower taxes and significantly reduce the then stifling regulatory burden. He has done both and suddenly investment spending has picked up to a double-digit pace and GDP growth accelerated to a 2.6% pace last year and is expected to reach 3.0% this year which would be the fastest annual growth rate since 2005. Thus, good fiscal policy has provided a welcome boost to the pace of economic activity.

However, most economists believe the recent stimulus will prove to be temporary and within a year or two, growth will revert to its old 2.0% potential growth path. But why should that be the case? A lower corporate tax rate and the ability to repatriate money from overseas should stimulate investment for many more years.

Businesses should be further encouraged to spend if Trump continues to eliminate unnecessary, overlapping, and confusing Federal regulations. And rapid technological advancements in artificial intelligence, autonomous vehicles, personal robots, 3-D printing, nanotechnology, and genome research will keep businesses spending for the foreseeable future, and that type of investment will boost productivity growth.

Thus, we believe that potential growth will pick up from 1.8% in the 2000’s to 2.8% by the end of this decade. There is no reason that today’s surge in investment spending should be regarded as a short-lived event.

Furthermore, what is magic about this expansion reaching the 10-year old mark and becoming the longest recession on record? The 120-month long expansion during the 1990’s surpassed the previous record (of the 1960’s) by 14 months. Why can’t the current expansion do the same? Expansions do not die from “old age.” They end because of policy mistakes.

Many think that a 10-year is expansion is a big deal. Certainly by U.S. standards that is the case. But the Australian economy just completed a world record 27th year of expansion. Why can’t the U.S. duplicate that astonishing achievement? Suddenly a 10-year expansion seems modest.

© 2018 Numbernomics.com.