Dana Anspach, founder of a Phoenix-based advisor firm called Sensible Money, rides a Harley-Davidson Softail Slim, recommends bond ladders to take the worry out of retirement, and deals firmly with clients who question her floor-and-upside methodology.

“Some people say, ‘Why are you telling me that I will earn less than 5% when my other advisor says I can get 8%?’” she said. “They missed the point.”

Anspach was a featured speaker at the Investment & Wealth Institute’s Retirement Management Forum. Held this week on Amelia Island, Florida, the event was the first in what will presumably be an annual forum based on the curriculum of the Retirement Management Advisor designation. The IWI (formerly IMCA, the Investment Management and Consulting Association) recently bought that designation from the Retirement Income Industry Association (which is no longer).

Anspach

Besides Anspach, experts like Michael Kitces, Moshe Milevsky, Brett Burns and Stephen Huxley shared their retirement planning insights with some 200 IWI advisors. About 40 of them came to take the exam for the Retirement Management Advisor (RMA) designation, which IWI bought from the Retirement Income Industry Association (RIIA).

For many attendees, the event was likely their first exposure to the client-centric, open architecture post-retirement planning model that RIIA (now disbanded) spent the past decade refining. The model emphasizes “outcomes” over probabilities, promotes a holistic view of the entire “household balance sheet,” and encourages retirees to “build an income floor, then seek upside.” In other words, it gives priority (subject to the client’s needs and goals) to the creation of safe income over further accumulation.

The topic of annuities rarely came up. The roster of corporate sponsors reflected a tilt away from these income-producing products. Nationwide was the sole annuity issuer, while fund companies (Capital Group’s American Funds, Invesco, and Russell Investments). Anspach mentioned them as a possible solution for less-wealthy households. It will be interesting to see if insurance sponsors and presenters play a bigger role at future Retirement Management Forums.

The barbell approach

Anspach was one of the first advisors to obtain the RMA designation, and she has used its principles, along with her visibility as the author of the “Money Over 55” page at About.com, to build a $175 million practice. Rather than relying on traditional safe withdrawal rates from balanced portfolios, she likes to build income “runways” for clients.

Typically, she’ll recommend a bond ladder to provide reliable sleep-easy income for the first six to eight years of retirement. The client’s other assets go in equities for the long run. To err on the safe side, she assumes a 4.25% minimum required growth rate for the entire portfolio, including bond ladder and equities.

It’s essentially a bucketing strategy. Each year, the proceeds from the maturing bond ladder are poured into a cash bucket. When the equity portfolio does well, Anspach might recommend adding another year or two to the bond ladder. When the equity portfolio doesn’t do well, she might recommend less spending until the portfolio recovers.

Her charge for an initial retirement income plan is typically $6,900. That’s aggressive, but she applies the payment to future expenses if the prospect becomes a long-term client and switches to an assets-under-management billing basis. She doesn’t measure client risk “tolerance,” but instead their capacity to endure losses and still maintain their necessary spending levels.

She assesses her clients’ portfolios every year to make sure that their current assets can generate at least 110% of required annual income for the rest of their lives. The length of a client’s bond ladder and the division of assets between bonds and equities depends on whether he or she wants to maximize consumption or bequests.

Anspach shared a few observations about communicating with clients more effectively. “We develop spending plans for our clients,’ she said. “It sounds so much better than budget.”

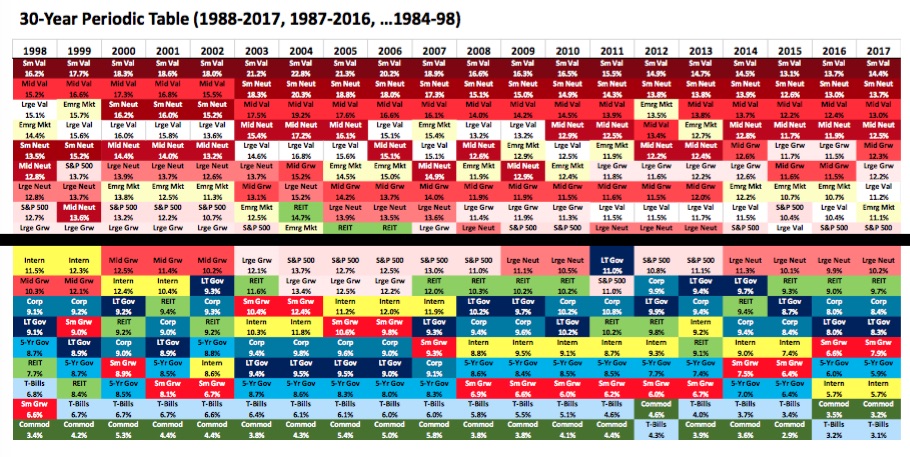

Small-cap funds for the long run

A time-segmentation strategy like Anspach’s offers an important benefit: It allows retirees to take more risk with the money they won’t need to touch for a while. Brent Burns and Stephen Huxley of Asset Dedication LLC—a turnkey asset management platform that, among other things, builds bond ladders for Anspach’s clients—suggested that the best asset class for anyone with at least a 15-year time horizon is small-cap value.

In their slides, Burns and Huxley showed that various mutual fund asset classes mutual show no consistent pattern of returns from one year to the next. But a distinct pattern began to emerge as the time horizon grew longer. Over rolling periods of 15 years or more, small-cap value funds consistently produce the highest returns, followed by small-cap neutral funds and mid-cap value funds. (See the image below).

(Note: A $10,000 investment in Vanguard’s small-cap value fund 10 years ago would be worth more than $25,000 today. Fidelity’s small-cap value fund has averaged almost 15% a year since 2008 and 10.3% a year since inception in 2004. The Russell 2000 Index has returned an average of 12.50% over the past 10 years and 7.52% since inception. All figures are before taxes and fees.)

Stocks in IRAs?

Taxes can be the single largest annual expense for a high net worth retiree, so tax minimization is an essential skill for almost every advisor. Celebrity advisor and presenter Michael Kitces tackled two important tax topics at the IWI-RMA conference. The tax optimization of product placement—the ideal assignment of assets to taxable or tax-favored accounts—was the first.

The conventional wisdom is that stocks belong in taxable accounts. That’s true for buy-and-hold single stocks that can benefit from a step-up in basis at death, of course. It’s also true for S&P 500 index funds, MSCI-EAFE index funds, and master limited partnerships. There’s a limit to that rule of thumb, however.

Even equity investments, Kitces said, will do better in a tax deferred account under certain circumstances: if the growth rate is high, the holding period is long, the dividend rate is high, the turnover rate of the fund is high, or if there are in-the-money currency hedges or embedded losses. Don’t attempt tax/asset optimization without software, he noted.

The second topic involved the question of optimal withdrawal sequence. In this case, the conventional wisdom is to spend taxable money first, then traditional IRA or 401(k) money (so that the assets compound longer on a tax-deferred basis) and then, at the end, take the tax-free Roth IRA distributions.

Alternately, as Kitces recommends, you could take smaller withdrawals from both taxable and traditional IRA accounts. This strategy allows clients to spend only enough from tax-deferred accounts to fill up the lower tax brackets, and then, if necessary, spend from taxable accounts where withdrawals won’t be taxed at ordinary income rates.

Biological age v. chronological age

Healthy, wealthy people with access to great medical care tend to live about 10 years longer than average, the data shows. But getting clients to recognize that they should plan on living to age 95 isn’t easy—perhaps because it cost so much more to finance a 30-year retirement than a 20-year retirement.

Moshe Milevsky’s presentation focused on helping advisors make this reality more “salient” to clients. The finance professor, longevity expert and author from York University, talked about his study of the phenomenon of “biological age.” When clients learn their biological age, he said, it might shock them into planning to be around longer.

Milevsky, who is 50, recently sent his personal medical metrics to a consulting firm that calculates biological age. Tests indicated that he’s living in a 42-year-old’s body. He suggested that advisors might warn their healthy, 65-year-old high net worth clients: “You’ll probably live until you’re biologically 85. But that’s 30 years from now, because you’re biologically 55 today.”

© 2018 RIJ Publishing LLC. All rights reserved.