Despite the continuing global financial crisis, the uprisings in the Middle East and the Japanese disaster, global stock markets delivered very good results in the first quarter of 2011.

These upheavals test the mettle of investment managers, so you need the proper perspective to evaluate investment performance. The question, “Is performance good?” requires an answer to yet another question: “Relative to what?”

As usual, some styles, sectors and countries performed better than others in this first quarter. Have your managers seized upon the better segments and/or selected exceptional securities? Where have they succeeded and failed?

Bottom line: Have they earned their fees?

Of course, one quarter is too short a timeframe to get excited about winners and losers, but we should get excited about the emerging importance of real due diligence, which is about to become a fiduciary obligation.

In October of 2010, the Department of Labor issued a recommendation to remove a 35-year old fiduciary exclusion for advisors who select investment managers. If adopted, many advisors who prefer to not be held to a fiduciary status will have a decision to make: stop providing manager recommendations or get serious about manager research.

Those of you who accept this responsibility will want to tighten up your due diligence processes. You will need to conduct manager research like it’s never been done before. When you do, you will discover something you’ve never had before, namely good active management performance versus passive alternatives. Clients will finally get what they deserve.

Insights into the first quarter of 2011

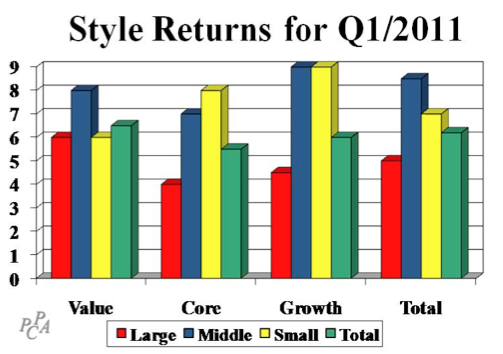

U.S. markets in the first quarter of 2011 delivered three consecutive positive monthly returns, although March was a squeaker, eking out a modest 0.2% gain. As the chart on the right shows, every US style posted a positive return for the first quarter of 2011, continuing the recovery that began in March of 2009.

This quarter’s 6.2% market return brings the 25-month return from March 2009 to March 2011 to a whopping 100%. Consequently we’ve turned the corner in recovering from 2008 losses; the 39-month return for January 2008 through March 2011 is a positive 1.4% un-annualized, or about 0.4% per year. It’s taken all the running we can do to stay in the same place.

As the optimist plummeting off a skyscraper said, “so far, so good.” We might not continue this recent recovery. A look at what has been working, and what has not, offers some clues. Mid-sized companies fared best, while value and growth styles fared about the same in aggregate, although core lagged.

This was one of those time periods where the stuff in the middle surprised by not performing in between the stuff on the ends—mid-cap outperformed large and small while core underperformed value and growth. I use Surz Style Pure® style and country definitions throughout this commentary, as described here.

Performance by sector

On the sector front, energy stocks fared best, earning 15% in the quarter, as concerns about the Middle East drove up oil prices. Industrials and healthcare were the next best performers, earning 9% and 7% respectively. Rounding out the range of sector results, the remaining sectors returned around 3.5%, far less than the leaders.

Looking outside the US, foreign markets earned less than half as much as the US in US dollars, delivering a 2.7% return, led by Canada and Europe ex-UK, each with 8.5% returns. Europe ex-UK benefitted from a weakening dollar, so currency effects added 5% in the quarter.

Several regions lost value in the quarter: Japan, Emerging Markets and Latin America. For Japan, which lost 3.5%, it was a continuation of a decade-long sequence of disappointing returns, in this case caused by the earthquake and nuclear reactor problems. For Emerging Markets and Latin America, this quarter marked a reversal because these regions had been leading foreign markets. As a result, the EAFE index, which had been lagging the total foreign market for some time, was in line with the total market for the quarter.

Now you have several frameworks for evaluating investment manager performance in the first quarter of 2011. But this is only one small aspect of the overall due diligence process – a process which should be forward looking, focused on developing confidence in managers’ abilities to add value. After all, clients always have the choice between active and passive management. Your recommendations of active managers are very important, which is good, and they are likely to become much more important.