More than 40 million Americans have invested $1.8 trillion in target date funds (TDFs), which appeared in the 1990s in the US. Yet, despite effort and experimentation by firms that offer TDFs, these funds-of-funds still aren’t designed to convert savings to retirement income.

Those efforts include “glide paths” that reduce investors’ equity exposure as they age, as well as guaranteed lifetime withdrawal benefits (GLWBs). Lately, a handful of asset managers have modified their TDFs to help plan participants to buy annuities at retirement.

These measures haven’t caught on, and probably won’t, because they’re not optimal. They are one-size-fits-all solutions that reduce volatility around the retirement date at the cost of reducing investors’ returns and potentially lowering their incomes throughout retirement.

iTDFs: Smooth transition from accumulation to distribution

Per Linnemann

To bolster retirees’ confidence in investment-based retirement income products, as opposed to insurance-based products, the transition from savings to income needs to be managed in a more capital-efficient way. In Denmark, I’ve designed iTDFs (individualized target date funds) to do that. I think iTDFs could also work in the US.

iTDFs transition seamlessly from the accumulation (saving) to the decumulation (income) phases, providing both a savings vehicle and a regular smoothed retirement income. iTDFs eliminate the need for separate products for pre- and post-retirement; the use of separate products can create an artificial cliff edge at retirement. There is no need to disinvest and then reinvest, and no fear of locking in unfavorably low interest rates when converting savings to income.

Unlike competing products—earlier TDFs, variable income annuities (VIAs) and investment-linked tontines—the new iTDFs approach gives each investor a personalized, dynamically self-adjusting glide path. Asset allocations are automatically adjusted between a risky (diversified) investment fund and a less volatile (diversified) investment fund.

Those adjustments are governed by two variables: the performance of the underlying investments and the current funded status of the retirees’ future income (i.e., the relation between the value of the assets and the value of the liabilities). These factors determine when the retiree can afford to spend more and/or take more investment risk.

That said, the investment risk exposure of the iTDF is reduced as investors get older. Retirees typically have a gradually declining tolerance and capacity for risk. They may not have time to ride out a sharp downturn in the financial markets or to return to work and supplement their income or replenish their savings.

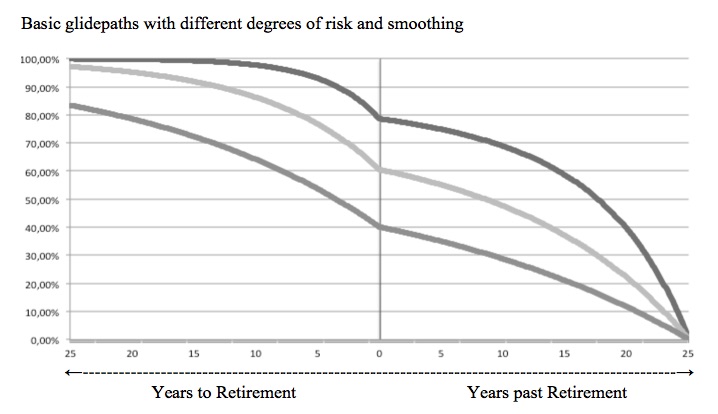

The y axis shows the equity allocation; the x axis shows years before and after retirement. iTDFs can accommodate alternative glidepaths with different starting equity allocations.

The built-in drawdown and investment strategies adapt automatically and dynamically to each other over time. They are integrated and coordinated by mathematical formulae and constitute a unified whole in an innovative way. The investment strategy supports the income-generation objective to smooth retirement income.

iTDFs are stochastic because they respond to changes in a dynamic and path dependent way. Path dependency (where the sequence of events influences the next step) is important to smoothing and sustainability of retirement income. In this way the balance between assets and future liabilities are being adapted and income can be smoothed while remaining responsive to financial markets’ performance.

Flexibility of iTDFs

iTDFs may be designed to provide income for a specific period, such as 10, 15 or 20 years. If the retiree wishes, he or she can eliminate longevity risk by purchasing a deferred income annuity at the start of the iTDF period or an immediate income annuity at the end. Spousal continuation may be added.

Retirees would not be required to buy a life-contingent annuity in advance. If they do choose an annuity, they would have the option to reverse the decision during the drawdown phase for any reason, e.g., deteriorating health. The surviving relatives may inherit the remaining savings if the participant passes away during the drawdown period.

Just as they offer a seamless transition from accumulation to decumulation, iTDFs also offer the option of a smooth transition between a drawdown and an annuity payout phase, avoiding a gap or other unintentional abrupt change in the level of retirement income.

The income stream from iTDFs is highly customizable. Income could be weighted towards the first stage of retirement, when retirees tend to be more active and spend more money. Alternately, income could be weighted toward the latter years to offset the effect of inflation.

Retirees could target a specific annual inflation adjustment to the payments or set an assumed interest rate (AIR) at the beginning of the income phase. The AIR is used to determine the initial payment. Subsequently, smoothed payments are automatically adjusted in response to the difference between smoothed investment returns and the AIR.

A solution to a nasty problem

iTDFs do not require expensive guarantees. The manufacturer does not have to assume investment and mortality risks. The same flexible framework can provide a platform for the creation of a family of products. Different versions of iTDFs can be tailored to local market conditions and modified to fit the needs of certain groups, such as low to medium earners. Relying on a robust algorithmic framework, iTDFs will fit easily into an increasingly digitalized and mass-customized world as fully automated solutions. The algorithm-based product design allows scalability, portability, and low cost.

Nobel economist William Sharpe called optimal decumulation the “nastiest, hardest problem” in retirement. iTDFs may provide a surprisingly simple solution. They provide the missing piece of the puzzle that stymies the asset management and retirement industries, and they could revive the life and pensions industry in a world without (expensive) guarantees.

For more about the author, see “Per U K Linnemann: The Pension Innovator.” To see more articles about iTDF, click here and here.

© 2021 Per U.K. Linnemann. All rights reserved.