Picture this: You have a client who is ten years away from retirement. He comes to you for retirement advice. You spend several hours, maybe even a full day with him. You consider many different retirement scenarios.

At the end of this exercise, you prepare a plan that’s as thick as a phone book. In your next meeting, you review the plan with your client.

One of your suggestions is that he buy disability (a.k.a. income replacement) insurance, in case he can’t work and earn income. But your client says that his employer already gives him similar insurance. He has no interest in purchasing his own disability insurance. After some intense discussions, you fail to convince him.

“Oh well,” you think, “maybe he’ll come around soon.” After your meeting, you decide to hand over the plan to your client.

Perhaps the client was just being stubborn. Perhaps he thinks you’re only angling for a big, undeserved commission. Perhaps he genuinely believes that his company hired him for life and their plan is all he needs.

The bottom line is, you weren’t able to demonstrate clearly why he needed disability insurance in his overall retirement plan. But you might have been more persuasive if you had been able to show him the precise impact of a loss of income on his retirement accounts.

Advertisement

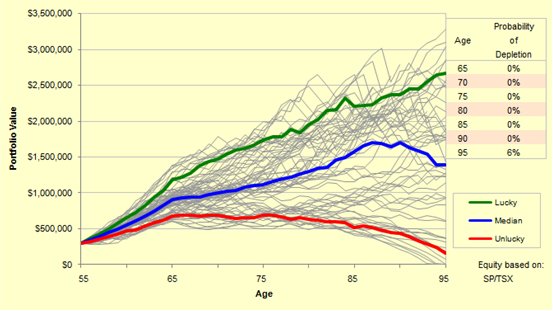

If you haven’t done that before, here’s an example: A couple, Bob and Sue, both 55, have about $300,000 in their retirement accounts. Their asset allocation is 40% equities and 60% fixed income. They intend to save a combined $25,000 each year until they retire at age 65. After retirement, they expect to need $50,000 a year, indexed to inflation. They anticipate $25,000 in combined Social Security benefits. They want their income to last until age 95.

In my case, I run this information through my retirement calculator, which is based on actual market history, and discover that they have a good plan (Figure 1). If they are lucky (top decile of all historical outcomes) and catch a good, long-term uptrend in the market, their portfolio will be worth about $2.7 million in 40 years. Even if they are unlucky (bottom decile of all historical outcomes), they’ll have about $165,000 at age 95.

Figure 1: Bob and Sue’s Retirement Assets over time

Well, not so fast. What if Bob loses his job? In that case, he also loses his disability insurance. Now he’s on his own. If he experiences a health problem or an accident and can’t earn income for awhile, he and Sue won’t be able to save $25,000 every year. Worse, they may have to spend some of their retirement savings to make ends meet. Their meticulous retirement income plan would go down the drain.

Figure 2 depicts the impact of a disability that lasts two years. The blue line on the graph in Figure 2 indicates the portfolio value if Bob has no disability insurance and he suffers no disability. Bob earns income continuously until age 65. Everything looks great; the portfolio lasts at least until age 95.

The red line depicts the portfolio value if Bob has no disability coverage and he becomes disabled during ages 55 and 56. Note that the portfolio life is shortened by 7 years. If Bob were single that might be acceptable, because a disability lasting two years might also reduce his life expectancy. But he needs to consider Sue. There is a 36% chance that she will be alive when their money runs out at age 88. This is not an acceptable retirement plan.

The red line depicts the portfolio value if Bob has no disability coverage and he becomes disabled during ages 55 and 56. Note that the portfolio life is shortened by 7 years. If Bob were single that might be acceptable, because a disability lasting two years might also reduce his life expectancy. But he needs to consider Sue. There is a 36% chance that she will be alive when their money runs out at age 88. This is not an acceptable retirement plan.

Finally, the green line on the chart indicates the portfolio value if Bob does have disability insurance. Even though he earns no income at ages 55 and 56, the portfolio value is only slightly lower than the blue line, because of the cost of the disability insurance. In this scenario, Bob and Sue still have income until age 95. This is a good retirement plan.

| Duration of total loss of income: | Portfolio life is reduced by: |

|---|---|

| 1 year | 1 to 7 years |

| 2 years | 5 to 11 years |

| 3 years | 8 to 14 years |

| 4 years | 12 to 17 years |

This table shows the impact of loss of income to portfolio life.

Remember that these numbers are only approximate. In this example, the assets were just barely adequate to cover the retirement income. If the client had already in been in what I call the “Red Zone,” the impact would be more severe.

Many factors can reduce the number of years in a portfolio’s life. These include the amount of excess assets already in the portfolio, the amount each spouse earns, when the disability occurs relative to retirement age, the amount of additional expenses the disability makes ne cessary, and whether or not one can collect government disability benefits.

However, the numbers in the table above might help you convince your client that, during the accumulation stage, disability insurance is not a luxury but a necessity for proper retirement planning. A retirement plan isn’t complete or comprehensive until you have carefully examined and covered the risk of disability.

Jim Otar, CMT, CFP, is a financial planner, a professional engineer, a market technician, a financial writer and the founder of retirementoptimizer.com. His articles on retirement planning won the CFP Board Article Awards in 2001 and 2002. He is the author of “Unveiling the Retirement Myth – Advanced Retirement Planning based on Market History” and “High Expectation and False Dreams” Your comments are welcome: [email protected].

© Copyright Jim Otar 2010