To teach young people “about basic economic principles and the Federal Reserve’s role in the financial system,” the New York Fed has published an Educational Comic Series. The pdfs of three of comic books are available for download from the New York Fed’s website.

These fanciful cartoon books use elements of science fiction (space travel, weird extraterrestrials, robots) to make the story of money entertaining and simple. But there’s a problem with the series. It repeats the myth that coins were invented to solve the inefficiencies of barter.

In one of the three books, “Once Upon a Dime,” the population of a planet called Novus barter with each other for what they need. A fisherman trades a fish for a jar of honey mustard. An E.T.-type swaps three small gears to a robot in exchange for the cakes the robot made. An octopus-like creature trades clock repair for a new pair of socks.

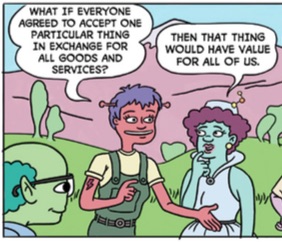

“This system of trading goods and services is called ‘barter’ and it works pretty well–as long as things don’t get too complicated,” the caption says.

The comic goes on to tell a familiar story, sometimes attributed to the 18th century Scottish economist Adam Smith: How coins (un-counterfeitable river stones, in this case) provided a common medium so that people could exchange goods for money at one place and time and then exchange that money for different goods at a different place and time.

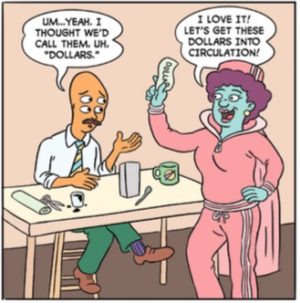

In this telling, money gradually made large-scale commerce possible. People accumulated rocks and, when they had too many, banks were created to safeguard the accumulations. The banks loaned out the idle rocks at interest. Paper money and checks were later created to eliminate the need to carry hundreds of rocks.

Eventually, a central bank was needed. As credit expanded, inadvertent over-lending and defaults led to panics and bank runs. So the residents of Novus decided to create and fund a central bank that would serve as the banks’ bank. It would also monitor all the other banks so that they didn’t create too much or too little credit.

The inaccuracy—not just the over-simplification—of this version of the money-and-banking creation story has been known for at least a century. In 1913, British diplomat and economist Alfred Mitchell-Innes pointed out the shortcomings of the barter theory of money in two essays published in the Banking Law Journal. The first essay was called “What is Money?” The second, “The Credit Theory of Money.”

In Innes’ account, markets existed long before the introduction of metal coins. Trade was financed by credit and debt obligations based on a combination of IOUs, trust, reputation, laws and enforceable contracts. Most importantly, the development of large-scale commerce preceded the use of money by many centuries.

“The idea that to those whom we are accustomed to call savages, credit is unknown and only barter is used, is without foundation,” Innes wrote. “From the merchant of China to the Redskin of America; from the Arab of the desert to the Hottentot of South Africa or the Maori of New Zealand, debts and credits are equally familiar to all, and the breaking of the pledged word, or the refusal to carry out an obligation is held equally disgraceful.”

Scholarly research has since supported Innes’ premise. In his 2011 book, “Debt: The First 5,000 Years,” David Graeber writes, “There’s no evidence that [a barter economy] ever happened, and an enormous amount of evidence suggesting that it did not.” In a more recent example, Harvard law professor Christine Desan studied the history of the issuance of coins in Britain for her 2015 book, “Making Money: Coin, Currency, and the Coming of Capitalism,” and didn’t find support for the barter story.

Scholarly research has since supported Innes’ premise. In his 2011 book, “Debt: The First 5,000 Years,” David Graeber writes, “There’s no evidence that [a barter economy] ever happened, and an enormous amount of evidence suggesting that it did not.” In a more recent example, Harvard law professor Christine Desan studied the history of the issuance of coins in Britain for her 2015 book, “Making Money: Coin, Currency, and the Coming of Capitalism,” and didn’t find support for the barter story.

It’s “a myth that money emerges naturally from the trades of enterprising individuals or their agreement on a common symbol of value,” she wrote. Coins, she discovered, were always in short supply, were not always durable, needed frequent revaluation, and were subject to hoarding. The big breakthrough in economics was, she found, was the 17th century discovery that governments (and, by extension, banks) could create large amounts of IOUs based on their anticipated receipt of taxes.

Desan characterizes modern money as a “political project” by which a sovereign government spends its IOUs (Treasury bonds, which pay interest, or Federal Reserve Notes, which don’t) into circulation and then cancels them as people and companies pay taxes. At the retail level, the government licenses banks to create dollar deposits out of thin air when they make loans, allow them to circulate at interest, and then extinguish the liabilities when borrowers repay the loans.

Does it make a difference whether we think that merchants spontaneously created gold coins and other “commodity money” to replace barter or whether we think of it as government-backed credit money (like the Continental dollars printed in the Revolutionary War, the greenbacks printed in the Civil War, or the “expansion of the Fed balance sheet” by trillions of dollars during the financial crisis)?

It makes a big difference. If money is a commodity originating in the private sector, then taxes can be characterized as confiscation—something parasitic to be resisted and avoided. But if a nation’s money is a kind of public utility, where the government and banks release money that never existed before, then taxes are essential. They complete the cycle of credit creation and destruction on which the global economy runs.

Your politics, in fact, is likely to be determined by the version of the story you believe. Whether you think that Social Security can or can’t “run out of money,” or whether you believe private banks should receive more or less government oversight, depends on whether you think money is primarily a private, a public matter, or both.

Desan thinks that we, as Americans, need to get the story right. Otherwise, we won’t be able to make smart decisions about our financial future. We’ve lost the “visibility of money as a political project,” she writes. With that disappearance, we also lost our ability to discuss “the role of fiscal action in supporting the value of money, the distributive stakes in the modern arrangement, and the alignment of rights and interests acted out in the ethics of capitalism. That absence, a void of history and theory, undermines the effort so urgent to our present moment to understand the political economy we inhabit.”

[Note: A spokesman for the New York Fed told RIJ this week that the central bank has been publishing educational comic books intermittently since the 1950s. He said he didn’t know if the comic books were historically accurate or inaccurate. The content of the newest comic books may have been based on the content of the older comic books, he said, which were written when the barter story still went largely uncontested.

© 2019 RIJ Publishing LLC. All rights reserved.