Removing ‘Lapse Risk’ from Variable Annuities

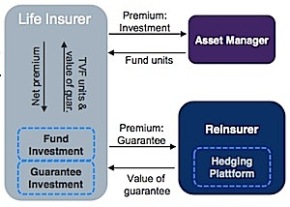

“Almost every major variable annuity writer has absorbed large write-downs on ‘policyholder behavior assumption updates,’” said a Munich Re executive. “So how do we take out that risk?”

“Almost every major variable annuity writer has absorbed large write-downs on ‘policyholder behavior assumption updates,’” said a Munich Re executive. “So how do we take out that risk?”