One comment in particular caught my ear during an online presentation last week by Lionel Martellini and Shahyar Safaee, the director and research director, respectively, of the EDHEC Risk Institute in France.

EDHEC, a business school and financial research institute, is probably the most important hotbed of decumulation studies that that you haven’t heard of.

Shahyar Safaee

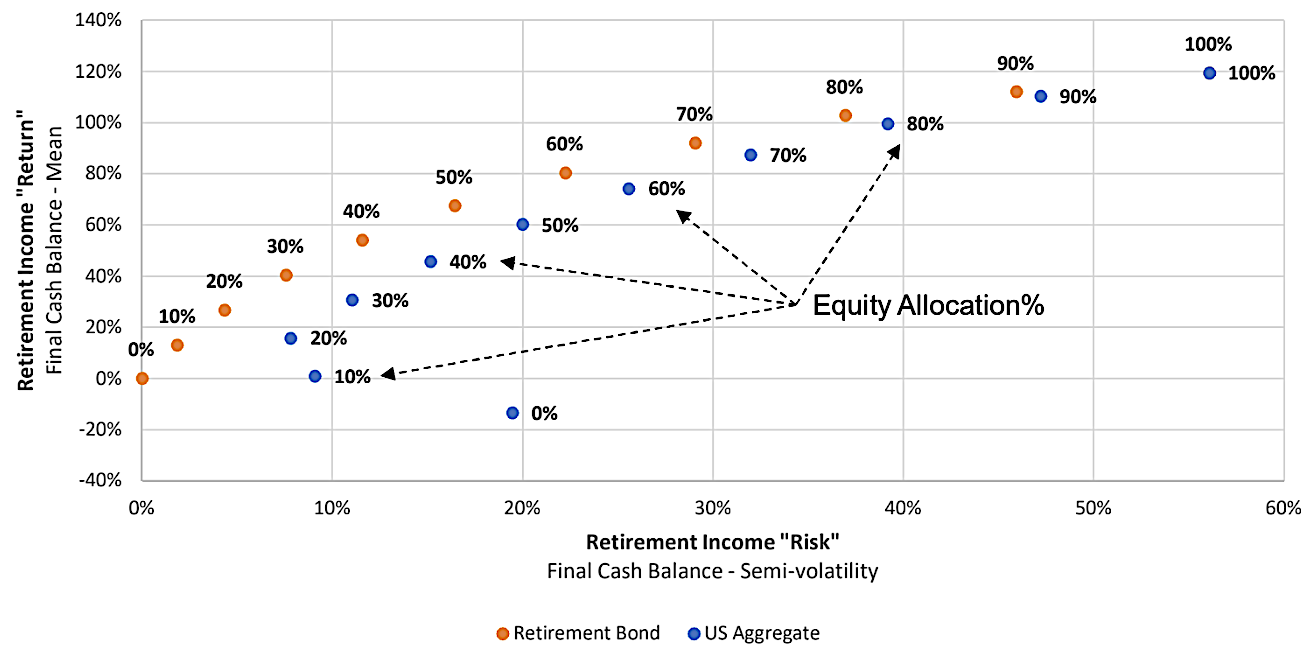

In his presentation, Safaee clicked to a slide showing a graph with the familiar rainbow of the “efficient frontier” of investing, with which we are all familiar. But on this particular slide the graph showed a double-arc rainbow: one arc composed of orange dots and the other of blue dots. (See below.)

The chart showed that at any given equity allocation, hypothetical retirees could get more income (on average, over a finite, 20-year window) with less risk if they put the balance of their assets into the “Retirement Bond” (more on that in a moment) that Safaee and Martellini were proposing—as opposed to investing in a standard fixed-income product assumed to be benchmarked by/represented by the US aggregate bond index.

“If you’re at 30% equity allocation in retirement, that would bear the same level of retirement income risk as a 39% equity allocation, leaving an extra 9% of equity allocation available,” Safaee said in a live Zoom meeting from his office in Nice, on the French Riviera.

“Using the Retirement Bond as the fixed income allows for more equity allocation for the same level of retirement income risk… and leads to a lower probability of a negative final cash balance,” the slides showed.

Note: This chart shows that using EDHEC’s Retirement Bonds for income during the first 20 years of retirement allow a higher equity allocation and higher final cash balance than using the bonds in the US aggregate bond index.

During my years in annuity marketing at Vanguard, we often promoted the idea that the addition of an income annuity to a retirement portfolio enabled retirees to take more risk with the remainder of their assets. This EDHEC research gives academic support to that idea. Martellini and Safaee’s slides also show the importance of knowing the yield of the zero-risk asset (the value of the y-axis at zero on the x-axis) in interpreting an efficient-frontier (EF) chart. When the risk-free yield increases (in this case Retirement Bonds are assumed to return more than the US aggregate bond index), the EF arc shifts upward. Zvi Bodie first pointed out to me the importance of the risk-free yield; it shows that the risk of portfolio failure associated with a given equity allocation is lower when the yield of the bond allocation is higher.

Lionel Martellini

So what exactly is this Retirement Bond that would make up the rest of a retiree’s portfolio for the first 20 years of retirement? Martellini said it would resemble the SeLFIES bonds that Robert Merton and Arun Muralidhar have proposed.

SeLFIES, as RIJ reported earlier this year, are risk-free, consumption-indexed government bonds for sale to individuals or plan participants before retirement. SeLFIES resemble ladders of zero-coupon TIPS. Each one might pay out $5 a year for 20 years, starting at retirement. The price of each bond would depend on the number of years until retirement and on interest rates at the time of purchase. To eliminate longevity risk, SeLFIES could be combined with a deferred income annuity with payments starting, for instance, at age 85.

EDHEC’s Retirement Bonds would correct a shortcoming of diversified bond funds as the “safe asset” in a retirement income strategy. The average duration of the fixed income component in target date funds, Martellini said, is too short for long-term investors; they would earn higher yields by investing in bonds with longer maturities. To make the bonds risk-free, they’d have to be issued by a government.

He defined EDHEC’s Retirement Bond as a “fixed income security paying constant (or cost-of-living-adjusted) cash-flows for the first 20 years of retirement; it is the true risk-free asset for the first two decades of retirement.” It could be created by building a ladder of risk-free bonds whose durations span the maturities of the Retirement Bond cash flows.

Asked if a 20-year period-certain annuity could replicate the income from his Retirement Bonds, albeit without the liquidity that Retirement Bonds would allow, Martellini said, “A period certain annuity has pretty much the same payoff as a retirement bond, without the flexibility offered by market traded instruments.”

He suggested that asset managers are missing an opportunity to meet retirees’ needs for safe income during the first two decades of retirement.

“It actually seems highly inefficient for the investment industry to stay away from addressing the needs of their clients once they reach retirement,” he said. “Insurance companies are critically useful to provide longevity risk protection via late life deferred annuities, but simpler and cheaper asset management solutions should be made available for the first 20 years in retirement.”

© 2021 RIJ Publishing.