Shunned in U.S., Income Annuities Thrive in the U.K.

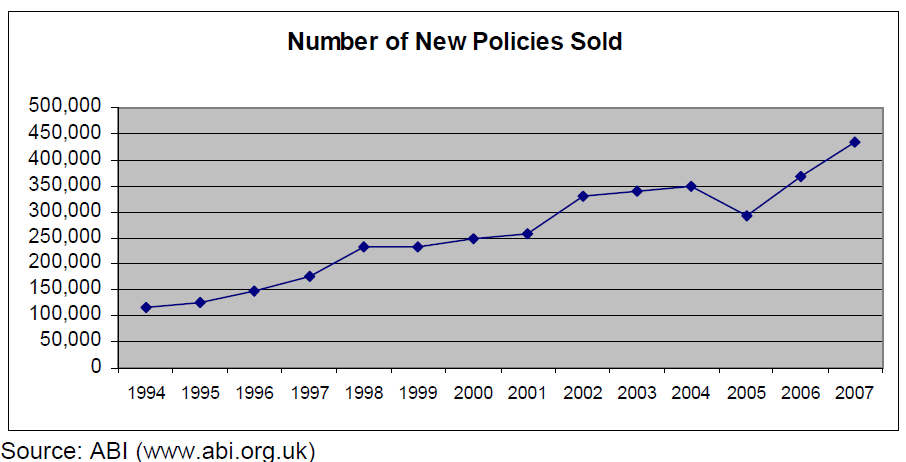

The "at retirement" market for annuities in the U.K. topped £14 billion in 2008 and is expected to reach about £23 billion in five years.

The "at retirement" market for annuities in the U.K. topped £14 billion in 2008 and is expected to reach about £23 billion in five years.