In sharp contrast to financial behavior in the U.S., hundreds of thousands of people in the United Kingdom convert their tax-deferred savings into income annuities as soon as they retire, according to a report from Watson Wyatt, the global consulting firm.

The so-called “at retirement” market for annuities grew to over £14 billion ($22.4 billion) in 2008 and is expected to grow 60% to about £23 billion ($36.8 billion) over the next five years. Britons buy roughly half of all income annuities sold worldwide, with a population of only 60 million. Prudential plc (no relation to Prudential in the U.S.) is the largest writer.

For those unfamiliar with the U.K annuity landscape, the report, “The UK Pension Annuities Market: Structure, Trends & Innovation” provides a detailed description.

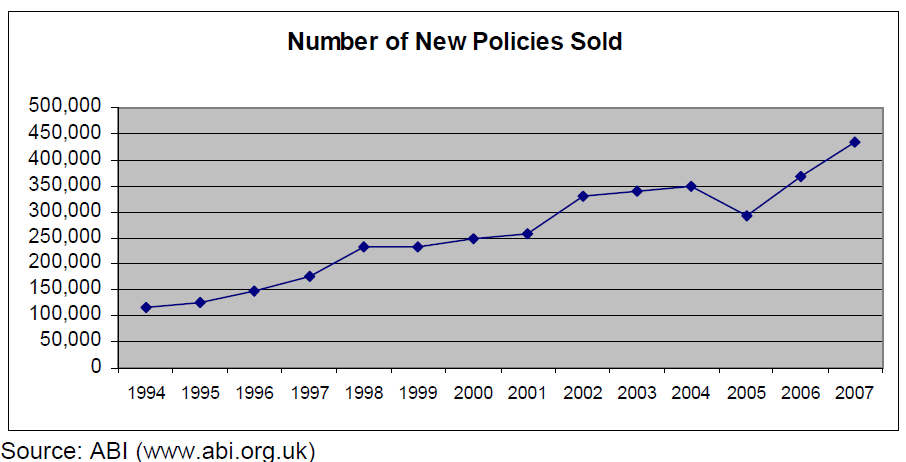

In 2008, the Association of British Insurers data indicates, over 450,000 pensions annuities were written, with an average “pensions pot” or retirement account balance of about £25,000 ($40,000). The median value was only about £15,000 ($24,000), with 75% of cases related to pensions pots worth less than £30,000 ($48,000). A pensions pot of £15,000 would generate a level income of perhaps £1000 ($1600) a year for a male aged 65, with no spousal entitlement.

In 2008, the Association of British Insurers data indicates, over 450,000 pensions annuities were written, with an average “pensions pot” or retirement account balance of about £25,000 ($40,000). The median value was only about £15,000 ($24,000), with 75% of cases related to pensions pots worth less than £30,000 ($48,000). A pensions pot of £15,000 would generate a level income of perhaps £1000 ($1600) a year for a male aged 65, with no spousal entitlement.

When they reach age 75, Britons are required to buy income annuities with their remaining tax-deferred savings-a requirement not entirely different from the U.S. required minimum distribution at age 70½.

Before then, when they first retire, British citizens can buy a “drawdown” product puts loose limits on the amount they can withdraw from savings, a “third-way product” like our variable annuities with lifetime income benefits, or an income annuity. Three types of income annuities are available, with fixed, variable, and “enhanced” payout streams.

Enhanced annuities, which accelerate payments for contract owners who have health issues that reduce their life expectancies, have been popular among retirees in the U.K. They don’t yet sell as well as standard income annuities, but their market share is 16% and growing. In the U.S., these products are known as “impaired risk” or “medically underwritten” annuities.

Enhanced annuities, which accelerate payments for contract owners who have health issues that reduce their life expectancies, have been popular among retirees in the U.K. They don’t yet sell as well as standard income annuities, but their market share is 16% and growing. In the U.S., these products are known as “impaired risk” or “medically underwritten” annuities.

The recent financial crisis has impacted the British annuity market in several ways. The European Union is requiring insurers to increase their reserves and invest more conservatively, thus putting downward pressure on annuity payout rates. But the collapse of the stock market after 2007 has helped drive sales of fixed income annuities by making investors and retirees more conservative.

In other U.K. developments, more Britons are taking advantage of the mid-2009 stock rally to swap their recently-recovered account balances for income annuities before stocks collapse again, if they do. “Managed and UK equity funds had jumped by an average of 29% and 38.5% respectively since March and a number of pension savers have had the opportunity to lock into these gains,” Professional Pensions reported.

A pension analyst at Hargreaves Lansdown, Nigel Callaghan, told Professional Pensions that individuals should also consider hedging risk by purchasing an annuity with part of their capital and leaving the rest invested. The EU Solvency Directive—which becomes effective in 2011, and will force insurers to hold greater reserves—could reduce annuity rates drop by as much as 20%. And it said government quantitative easing measures—the low interest rate policy—could lead to an inflationary environment causing annuities to rise in the medium-term.

© 2009 RIJ Publishing. All rights reserved.