President Trump recently flummoxed the liberal henhouse by mentioning the possibility of stimulating the economy by legislating a payroll tax holiday—which at an annual rate would eliminate about a trillion dollars a year in revenue from Social Security and hasten its insolvency—at least technically.

On August 19, four Democratic Senators (Bernie Sanders, VT; Chuck Schumer, NY; Chris Van Hollen, MD; and Ron Wyden, OR) sent a letter to Stephen C. Goss, the Chief Actuary of Social Security, asking for his analysis of “hypothetical legislation” that cut off payroll taxes as of January 1, 2021.

In a response this week, Goss wrote that the Social Security and Disability Insurance Trust Fund reserves “would become permanently depleted by the middle of calendar year 2023, with no ability to pay OASI [Old Age and Survivors Insurance) benefits thereafter.”

But he prefaced that remark by also writing that “the projected depletion date of the trust fund reserves [~2034] would be essentially unaffected by the legislation,” if the trust funds were “held harmless” by further provisions in the legislation—as they were during payroll tax abatements in 2010 to 2012 recession.

Eugene Steuerle

Here at RIJ, this exchange naturally raised questions. As we often do, we took our Social Security questions to Eugene Steuerle of the Urban Institute, a Social Security expert with many years’ experience in the federal government. Our interview with Steuerle follows.

RIJ: When Social Security doesn’t have enough revenue to cover benefits, doesn’t it “sell” those bonds to Treasury and receive “cash” so Social Security can pay benefits (all for accounting purposes)?

Steuerle: Yes. But the trust fund doesn’t have enough bonds to pay “full” benefits after 2035 or so. If it takes in less taxes, that date gets moved up.

RIJ: Other than interest, in what sense does the trust fund have income?

Steuerle: Trust fund income includes Social Security payroll taxes or “contributions,” plus interest from the trust fund bonds, as well as taxes collected through income taxation of Social Security benefits. The payroll taxes dominate.

RIJ: Doesn’t Social Security simply “lend” money to Treasury when there are surplus payroll taxes and then “redeem” the “debt” when there is a shortfall in payroll taxes (all strictly for accounting purposes)?

Steuerle: Yes, but eventually there will be no bonds left, and the law requires that benefits must be paid only out of the trust funds, thus preventing borrowing from Treasury absent new legislation.

RIJ: Has Social Security already begun to sell its special bonds to Treasury, thus reducing the “trust fund”? If so, when exactly did that begin? How far has the trust shrunk since its peak value?

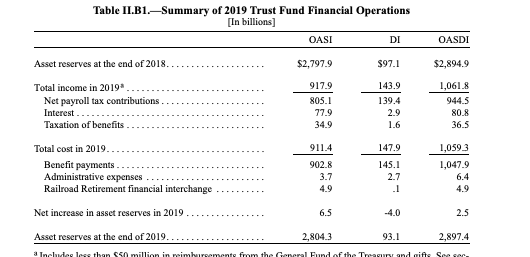

Steuerle: This past year taxes and interest just about matched benefit payments. Benefit payments are roughly $1.05 trillion; asset reserves are about $2.9 trillion. In the future, trust fund bonds will increasingly be sold. And trust fund income from all sources will increasingly fall short of benefits.

See the table below for 2019. The unemployment associated with the current pandemic and its aftermath also adds to the gap for 2020 and probably the next few years.

RIJ: So payroll tax is “income” for the trust fund? Has payroll tax ever flowed into the trust fund before being paid to beneficiaries or “loaned” to the Treasury general fund?

Steuerle: This is all definitional. The taxes come in mainly to the IRS, which credits them to the Social Security trust fund. The trust fund then holds special purpose Treasury bonds for any reserves arising from past surpluses. The federal government then “writes checks” against the trust fund balances.

RIJ: If Congress were to pass the President’s “hypothetical legislation” for a payroll tax holiday in 2021, then would Social Security have zero revenue and zero remaining trust funds within the next couple of years?

Steuerle: If you take away payroll taxes and trust fund interest, the trust funds [now at $2.9 trillion] would be depleted quickly. Losing one year of payroll taxes would deprive the trust fund about $1 trillion of income, plus future interest on that income.

RIJ: What about the previous forecast, or conventional wisdom, that Social Security, as is, can pay 100% of promised benefits to 2034 and 75% of promised benefits thereafter? Is that forecast now obsolete?

Steuerle: Yes, unless Congress would pay back Social Security for payroll tax revenue lost during a suspension. which is what has done in the past. But the President’s authority on deferring taxes does not extend to this matter—though that appears to be what he is counting on.

In a sense, the President’s position is not very different from that of some Democrats, who seem to feel that, if they can delay reform until close to 2035, Congress would not allow everyone’s benefit to be cut by 25%. That is, at that point, there would be no money in the trust funds. Essentially all revenues would derive from the payroll tax, and those taxes could only cover 75% of scheduled benefit payments to current retirees and disabled persons.

RIJ: So Social Security will not be able to pay any benefits from 2023 onward if the hypothetical legislation passes?

Steuerle: Yes—unless, as I said, Congress pays Social Security back and the payroll taxes start flowing again.

RIJ: Can’t Congress just pass a law that says payroll tax shortfalls will be covered by appropriations from the Treasury general fund? After all, today’s retirees paid income tax in addition to payroll tax for decades.

Steuerle: Yes, Congress can convert Social Security deficits to non-Social Security deficits. The effect on the unified deficit is essentially the same.

RIJ: Why is the public still led to believe that Social Security has the same constraints as a private pension fund, when the truth is that the U.S. Treasury can always meet its obligations; that only self-imposed constraints, and not lack of resources, would stop the US Treasury from paying promised benefits?

Steuerle: This goes all the way back to the Roosevelt administration. Roosevelt himself argued that he did not believe that the system should be set up with shortfalls that would force future Congresses to legislate new tax increases on future taxpayers. He supported the “private pension” analogy. He wanted people to believe they had “earned” their benefits even though, in a pay-as-you-go system, each generation’s taxes largely go to pay their parents’ benefits and are not saved for their own. Even those who argue that ‘deficits don’t matter’ seldom if ever suggest that we run government without ever collecting taxes. Where’s the limit?

RIJ: No, that would invite inflation and eliminate a policymaking tool. But I’ll defer to you for the last word on that.

Steuerle: The bottom line is that we benefit from government and we pay for it. Leaving more bills to our children, regardless of which government account is used, doesn’t negate that fundamental logic.

RIJ: Thanks, Gene, as always.

© 2020 RIJ Publishing LLC. All rights reserved.