Followers of what RIJ calls the “Bermuda Triangle” trend may have spotted a couple of large deals in that space this past summer—during that deceptively peaceful lull between mass vaccinations and the Delta surge.

On August 9, the recently created Bermuda-domiciled reinsurance arm of $600 billion asset manager Brookfield Asset Management bought Texas-based American National Group, a closely held publicly traded life insurance company group, for $5.1 billion. American National Life had $28.6 billion in assets at the end of 2019.

On July 13, Global Atlantic Financial Group, a US-focused annuity, life insurance and reinsurance company majority-owned by KKR, the $342 billion global asset manager, reported a new USD $4.8 billion reinsurance transaction.

In the deal, Global Atlantic’s Bermuda-based subsidiary Global Atlantic Assurance Limited will reinsure blocks of life insurance policies issued by subsidiaries of French insurer AXA: AXA China Region Insurance Company Ltd and AXA China Region Insurance Company (Bermuda) Ltd. It was Global Atlantic’s first block reinsurance transaction sourced outside the United States, according to a release.

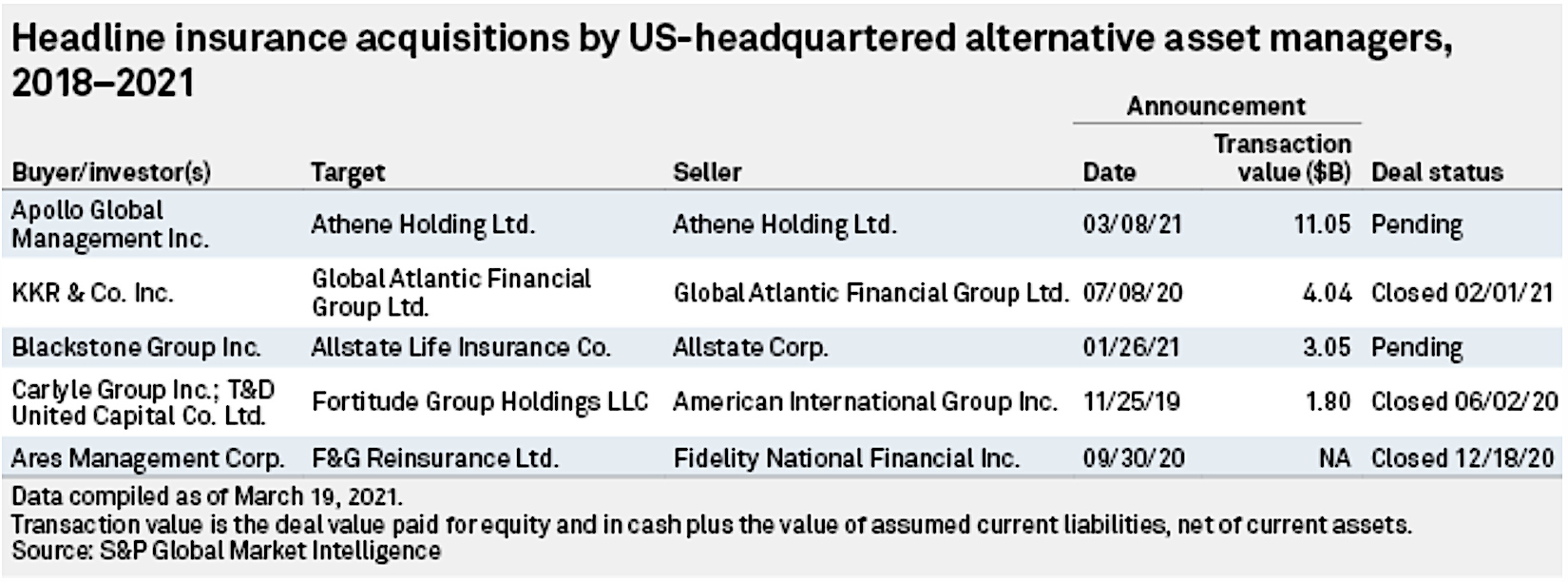

RIJ uses the term Bermuda Triangle to refer to the trend, not entirely new but accelerating as we speak, that involves complex three-way arrangements between a US life/annuity company, a Bermuda-based reinsurance company, and a large asset manager like KKR, Apollo, Blackstone, Carlyle, Ares, or Brookfield.

These wealthy firms are buying insurers or reinsuring blocks of business because it gives them several opportunities to make money. They can earn fees managing the assets (insurance and annuity premiums), they can take advantage of Bermuda’s GAAP accounting regime to economize on capital and invest in riskier, higher-yielding assets, or they can borrow against a life insurer’s assets to finance new deals, bringing in more institutional investors. Since annuity premiums doesn’t move for years at a time, they can earn an “illiquidity premium” from investing in long-dated assets, either for sale to life insurers or other investors.

This is heralded on Wall Street as a win-win-win. Private equity firms are said to know how to get more yield from the insurance assets, thus putting the liabilities (promises to policyholders or contract owners) on a firmer financial footing.

When they own life insurers, the PE firms are said to pass higher yields on to annuity owners by offering them higher crediting rates on fixed deferred or fixed indexed annuities. Since they are using these assets to make higher profits, they’re also helping their own shareholders. Bermuda, by the way, welcomes all this commerce.

So why aren’t I ready to celebrate the Bermuda Triangle? Because some of these deals, unlike the Bermuda weather, often lack for sunshine. Financial activity in Bermuda isn’t as transparent as it is in the US, and the synergies enjoyed by affiliated dealmakers there might be viewed as conflicts-of-interest if they were within view of US regulators. More generally, the life insurance business is looking more like the investment business, and I’m not convinced that’s a good thing.

© RIJ Publishing LLC. All rights reserved.