The road to including lifetime income options in the investment lineups of defined contribution (DC) plans was smoothed a bit by the 2019 SECURE Act. But the law didn’t remove every roadblock that annuity issuers face before 401(k) plans can become a thriving distribution channel for their products.

[Note: Factual errors about the Principal Pension Builder in the December 17 version of this story have since been corrected.]

To be sure, the Act did a couple of important things. It reduced the legal liability of plan sponsors for their choice of annuity provider, allowed participants to take their annuities with them when changing jobs, and made it easier for participants to see how much monthly income their current accumulations could buy.

But the Act didn’t remove a Catch-22 that complicates the introduction of annuities into 401(k)s. Annuity issuers can’t tailor annuities to fit 401(k) rules and still give full rein to the value of annuities.

The life insurers ideally hope that their 401(k) annuity offerings can be bundled into qualified default investment alternatives (QDIAs), so that participants can be auto-enrolled (defaulted) into them. At the same time, pension law requires life insurers to make their 401(k) annuities liquid—i.e., convertible to cash instead of to an income stream in retirement. Current QDIAs are target date funds (TDFs), managed accounts and stable value funds.

But, to check both of those boxes, annuities must become a bit less annuity-like. Part of an annuity’s yield advantage—their “alpha,” so to speak of—depends on their illiquidity (locking money into higher-earning, long-term investments). Additional yield depends on pooling effects (risk-sharing among participants that could entail forfeiture of assets to other pool members).

Because those key characteristics conflict with the rules governing 401(k)s, life insurers must adapt their annuities in various ways to fit the 401(k) world. Luckily, they don’t have to start from scratch. They’ve had several years of practice with this challenge, which is part legal, part behavioral (popular resistance to illiquidity and pooling).

Principal Pension Builder

Principal Financial and TIAA are bullish about their in-plan annuity designs, which involve deferred income annuities (DIAs). Contributions to the DIAs would grow in value during the participant’s accumulation years. Later, if they desire, participants would need to actively choose to convert the assets to lifetime income or cash them out gradually all at once.

These products allow participants to enjoy the relatively high returns and low volatility that come from investing in a life insurer’s general fund instead of in an ordinary bond fund. The general fund achieves higher returns by adding a dash of high-yield investments to a portfolio consisting mainly of highly rated corporate bonds. The general fund mitigates volatility by holding bonds to maturity.

The Principal Pension Builder, first introduced in 2015, has been reintroduced as the in-plan annuity option for companies that join Principal EASE, which is Principal’s Pooled Employer Plan, or PEP. (PEPs are plans that dozens or hundreds of unrelated companies can join; the SECURE Act made PEPs possible.)

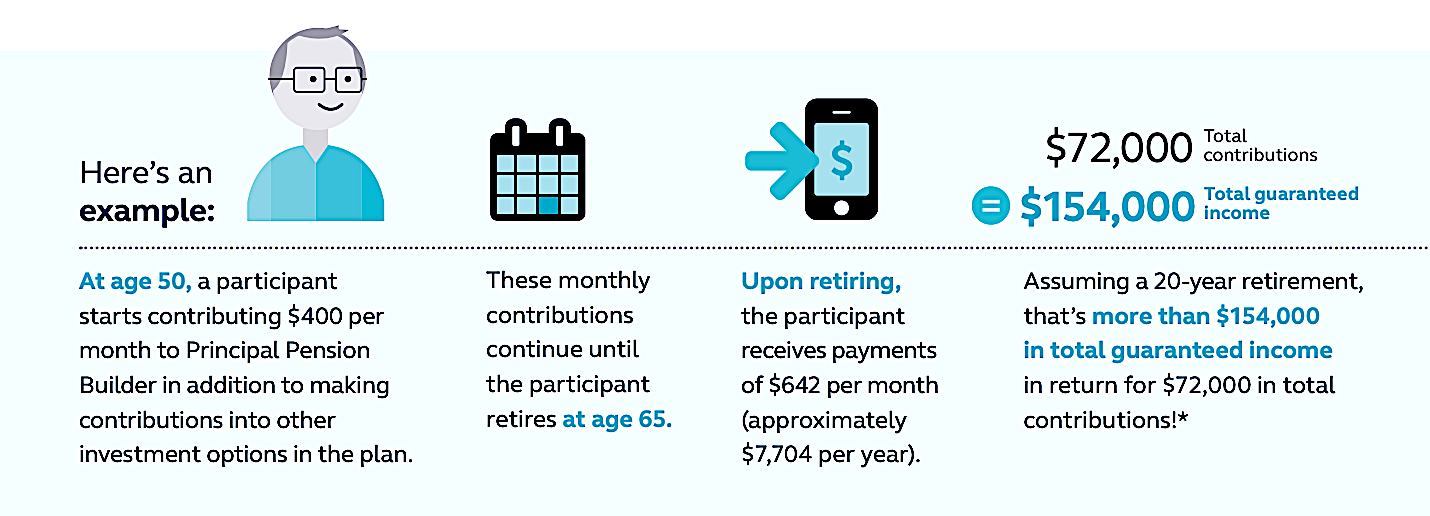

EASE participants can’t be defaulted into the Pension Builder DIA; they must choose it and allocate part of their contributions to it. With each contribution, they buy a slice of guaranteed lifetime income in retirement. In the hypothetical example from Principal’s Pension Builder brochure, a participant might begin contributing to the DIA at age 50.

- “Participants who purchase PPB on a payroll basis are purchasing slices of annuities with each purchase,” a Principal spokesperson said. “The monthly guaranteed income amount purchased will not change in value during the participant’s accumulation years, as the deposit has purchased a deferred income annuity for that participant and the value is no longer exposed to the market. Participants are given the opportunity as they approach the income start date to choose a different income start date or a different form of annuity, which will provide them with the actuarial equivalent of the monthly guaranteed income amount they were promised at the time of deposit.”

TIAA RetirePlus

TIAA deals with the liquidity/general account conflict differently in its RetirePlus program for 403(b) plans at non-profit institutions. Participants can be defaulted into RetirePlus, which is a kind of custom target-date managed account that each employer can fill with its own investment lineup. If the employer wishes, the fixed income option in the program is a TIAA group fixed deferred annuity instead of the usual bond fund.

In its RetirePlus solutions, TIAA offers a modified version of TIAA Traditional, the fixed deferred annuity that TIAA plans have offered for decades. The difference is that the fixed annuity in RetirePlus plans is fully liquid (to satisfy the QDIA requirements) and the classic TIAA Traditional annuity is much less so.

But there’s a cost to adding liquidity. Yields vary, depending on the version of fixed annuity contract RetirePlus a plan sponsor uses, the prevailing interest rates, and a participant’s own longevity with TIAA, but the yield of the fixed annuity in RetirePlus solutions will always generally be about 75 basis points (0.75%) less than TIAA Traditional. If a participant wants to cash out of the fixed annuity, TIAA pays them out of reserves.

There is no penalty for participants who take the fixed annuity portion of RetirePlus as cash, but they’d be giving up a valuable annuity if they didn’t take their account value as a retirement income stream. That’s because the TIAA income annuity continues to accrue dividends for the life of the contract, creating the potential for a rising income in retirement. While RetirePlus is currently marketed to 403(b) plans, TIAA sees no reason why a similar solution can’t be used in the 401(k) market.

From a TIAA RetirePlus video

Which product design will win?

Other DIA-based 401(k) annuity offerings have appeared recently, notably from BlackRock and Wells Fargo. Participants who invest in BlackRock’s LifePath target date funds would see part of their contributions shift into an in-plan group annuity at age 55. At retirement, they could turn on an income stream that combined payouts from the annuity and systematic withdrawals from their remaining investments.

Participants in Wells Fargo Retirement Income Solutions program can contribute to a target-date Collective Investment Trust (CIT). At retirement, 15% of their account balance would be applied to the purchase a qualifying longevity annuity contract, or QLAC. A QLAC is a deferred income annuity whose payouts can be delayed until age 85 without violating the rule on required minimum distributions at age 75.

DIAs received a vote of confidence recently from Cerulli, the global consulting firm. Cerulli recently reported that, of all 401(k) in-plan annuity designs, DIAs may offer the best value. “[We believe] annuitization products, where an investor converts a lump sum to a guaranteed income stream, represent the better solution for DC plans,” according to The Cerulli Edge U.S. Monthly Products Trends report for November 2020.

Cerulli is less enthusiastic about the guaranteed minimum withdrawal benefits that characterized the first generation of 401(k) annuities. These were target date funds with a living benefit rider attached. At about age 45 or 50, participants were defaulted into paying 1% per year for a rider that offered a lifetime income guarantee and liquidity. The value-add of this product comes from allowing retirees to stay invested in equities and get exposure to the equity premium throughout retirement. Many people have difficulty understanding these products, which have two sleeves: the cash value of the contract and the “benefit base,” a notional amount used as the basis for calculating the owner’s minimum guaranteed annual income in retirement.

But those products, all introduced before the SECURE Act, did not find a significant market. “There are a handful of target products that offer guaranteed retirement options, most notably guaranteed minimum withdrawal benefits (GMWBs),” the Cerulli report said, but added that “GMWBs often have Byzantine rules and restrictions associated with them, making them challenging for less sophisticated investors to understand.”

© 2020 RIJ Publishing LLC. All rights reserved.