At its heart, the fixed index annuity is a simple product. About 96% of premiums go into a life insurer’s general account, which earns about 4% a year. The rest is split between the cost of overhead and the cost of put and call options on the performance of an equity index or exchange-traded fund. Over the long run, FIAs can be expected to yield about two percentage points more per year than bonds.

But the indexed products themselves, and their distribution through insurance agents, brokerages and banks, and their regulatory controversies over the past quarter-century is much more complicated than that. Given the product’s rising success—and its record sales in 2018—we thought it was time for a close, sustained look at the FIA phenomenon.

Retirement Income Journal and Wink, Inc., the Des Moines-based independent life insurance and annuity market research firm, are recognizing FIA’s steady rise in sales with a four-week series of articles about them. Over the next month, we’ll look at the leading issuers of FIAs, at the mechanics of the products, and, finally, at their potential role, relative to other solutions, in Boomers’ retirement income strategies.

This week we’ll take a deep dive into the latest FIA sales numbers, as reported in Wink’s Sales & Market Report, 1st Quarter, 2019. The numbers show a new group of life insurers, relatively new to the FIA business, challenging the long-time leaders. On the distribution side, half of all sales still go through the insurance agent channel, but a big chunk of the flow has shifted to the brokerage and bank channels in recent years.

The FIA products themselves have gradually gotten a bit less flamboyant over the past two decades. Their design depends on the business model of the issuer, the channel through which they’re sold, and how that channel is regulated. Products for the big state-regulated agent pipeline tend to have longer surrender periods and a carnival of features. Products for brokerage and bank distribution, which come under federal supervision, tend to be a little more conservative in terms of compensation and surrender period.

Over the past few years, life insurers have been dangling no-commission FIAs (with more upside potential than commission products) in front of registered investment advisors (RIAs), hoping to break into that still-skeptical fee-based market. The future of the FIA industry may well depend on whether that foray is successful. (In two weeks, we’ll look under the hood at the design of the simplest as well as the most complex FIA contracts.)

Sales by life insurer

The FIA market has had remarkably stable leadership, with Allianz Life the consistent leader, followed by Athene (which leapfrogged to the first rank by buying Aviva in 2013), the AIG companies and American Equity Investment Life at the top of the leader board.

Led by Allianz Life (having purchased the FIA pioneer Life USA in 1999), which has held at least a 10% market share for 17 of the last 18 years, these four firms accounted for 36.7% of sales in 1Q2019. Just as the life insurance business overall is concentrated, so is the FIA business, with the top 10 companies (out of 68 FIA manufacturers) accounting for about two-thirds of sales.

Recently, however, the composition of the peloton behind them has changed, as major variable annuity (VA) issuers have shifted some of their production to FIAs. These include Nationwide, Pacific Life, and Lincoln National, which have climbed to the 5, 6, and 7 spots in sales. Great American, Midland National, and Fidelity & Guaranty appear to have moved down to make room for them. (Although still far behind the leaders, other VA veterans like Transamerica, Jackson National, and Prudential showed triple-digit sales growth in the first quarter of 2019 from the first quarter of 2018).

Overall, the FIA industry saw an 8% drop in first quarter 2019 sales (to $17.7 billion from a record $19.2 billion in 4Q2018), mainly because December’s flight to safety (in response to the Fed-inspired equity sell-off) ebbed in 1Q2019. But the past three quarters have been the three best in the history of FIAs. Last year also enjoyed a rebound from 2017 sales, when the threat of regulation by the Department of Labor temporarily chilled sales.

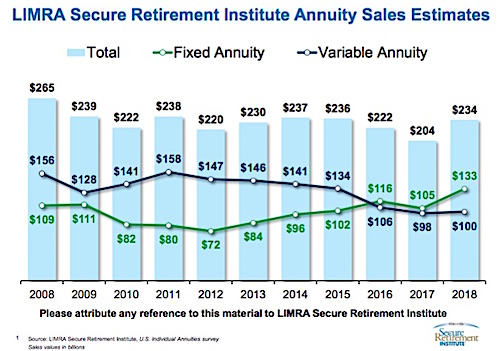

As noted above, however, the FIA market has grown in part because of retooling by VA manufacturers. The chart below shows that trend within the annuity market from VA sales to fixed annuity sales began long ago, in 2011. The overall annuity market has not been growing, despite Boomer aging.

“Are there agents who are registered reps who used to sell VAs but are now selling FIAs? Absolutely,” said Sheryl Moore, CEO of Wink, Inc. “That’s because the VAs were totally de-risked,” which took away much of their upside potential. “But I doubt that there’s a ton of 1035 transfers from FIAs,” she added, because many in-force VAs are too valuable to justify a transfer.

Sales by distribution channel

Until not long ago, the independent agent channel accounted for more than 90% of FIA sales. But the agent channel’s share has fallen to about 54%, in part because of regulation, as we’ll explain below. Much of its sales flow now passes through registered reps in independent brokerages (16.6%) and bank advisors (17.1%).

The wirehouse (also registered reps) and career agent have 5.9% and 6.6% of sales, respectively. The newest channel, which consists of online platforms that distribute no-commission FIAs and other insurance products to RIAs, is just getting started.

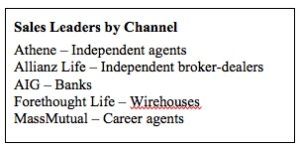

Some of the major FIA issuers, such as AIG, Lincoln National, American Equity, Pacific Life, sell across multiple channels. Others tend to specialize. While it also sells through banks, Athene sends most of its sales through (and currently leads) the independent agent channel, while Allianz Life is always a dominant factor, if not the leader, in both of the two largest channels (independent agents and broker-dealers). Global Atlantic (Forethought) focuses on the bank and wirehouse channels. MassMutual leads the career agent channel.

In the first quarter of 2019, AIG led in the bank channel, and was #2 or #3 in the independent broker/dealers, wirehouse and among career agents; it is not a leader, however, in the largest channel (independent agents).

Global Atlantic Financial Group (it owns Forethought, which acquired Hartford’s annuity business in 2013) leads the wirehouse (national full-service broker dealers) channel. Massachusetts Mutual leads in the career agent channel.

Regulatory pressures account for much of the shift in sales flow out of the independent agent channel to the independent broker-dealer channel. Many of the agents who sold FIAs also had securities licenses and were registered with broker-dealers. But they identified their FIA sales as “outside business activity” and didn’t submit the transactions to their broker-dealers for review and approval.

In 2007, the Securities & Exchange Commission tried to reclassify FIAs as securities, in what was seen by some in the insurance industry as a grab for FIA businesses by the brokerages. The SEC failed in its attempt, but brokerages began insisting on reviewing FIA sales. As a result, the amount of flow reported through the agent channel began to be reported through the independent brokerage channel.

“Independent broker-dealer sales of FIAs have gone from zero to 17%,” said Jeremy Alexander, CEO of Beacon Research, an annuity data aggregator. “That’s the regulatory impact. It may be that the same guys are selling FIAs, except now they’re selling them through the IBD channel instead of through their FMO.”

“Most independent broker-dealers are taking FIA sales through the grid,” said Moore. “But I wouldn’t say that there’s no absolute growth in the FIA market. The percentage of total sales through the independent B/D channel is growing, but so is the absolute dollar amount. The whole pie is growing.”

Sales by product

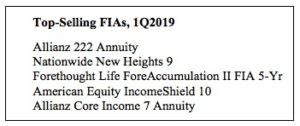

The five best-selling FIAs in the first quarter of 2019 were the Allianz 222 Annuity; the Nationwide New Heights 9; Forethought Life’s ForeAccumulation II FIA 5-Year 4, the American Equity IncomeShield 10; and the Allianz Core Income 7 Annuity.

The Allianz 222, a big, all-in-one product with tempting bonuses and a built-in (non-optional) rider that provide lifetime income ten years after purchase, is the leading product in the independent agent and the independent broker/dealer channels. Two other Allianz Life products were among the top ten sellers in the independent broker/dealer channel: Allianz Core Income 7 and Allianz 360.

ForeAccumulation II 5-year (the #3 seller overall) was the top seller in the bank and wirehouse channels. The 7-year version of the product was among the top ten best-selling products in both of those channels. The C.M. Life Index Horizons contract, which is issued and distributed by MassMutual was the most popular product in the career agent channel.

ForeAccumulation II 5-year (the #3 seller overall) was the top seller in the bank and wirehouse channels. The 7-year version of the product was among the top ten best-selling products in both of those channels. The C.M. Life Index Horizons contract, which is issued and distributed by MassMutual was the most popular product in the career agent channel.

Consumers will see different types of products in different distribution channels. In the independent agent channel, products with 10-year surrender periods dominate. That’s partly because competition in those spaces demands (and mild state regulation allows) products with high incentives for agents and alluring premium bonuses. Ten-year deferral periods give the insurers time to cover the costs of commissions and bonuses.

It’s precisely those products, with their complex designs, overwhelming number of choices, sensational claims and long waiting-periods for benefits that may never fully materialize, that drew the attention of regulators. And that’s why FIAs sold through banks and broker-dealers are more likely to have five-year to seven-year terms, which are considered more client-friendly.

Conclusion

Regulation may be shaping FIA product design and distribution channels, but consumer demand for FIAs ultimately depends on two factors outside of the control of both the life insurers and the agents or advisors: Interest rates and stock market volatility.

Historically low interest rates, beginning with the plunge in the Fed funds rate to 1% in 2003 and back to almost zero in 2008, foster the sale of FIAs because the insurers’ long-date assets out-yield money market funds and certificates of deposits. At the same time, tremors in the equity markets send investors in search of low-risk or guaranteed assets.

Boomer retirement, and the mountain of savings that it entails, has helped drive the purchase of all kinds of financial assets. But it does not seem to have delivered the bonanza that the annuity industry once anticipated. That may disappoint distributors, but it’s not clear if the life insurance companies disturbed by that or not.

The leaders of the industry may have acquired as much risk as they want right now. “It’s not like there’s not enough demand,” said Alexander, who points to the annuity sales plateau of about $220 billion a year. “It’s not like the carriers are saying, ‘How can we break $240 billion?’ The carriers know how much they will sell and they have levers to control it.”

Next week: A closer look at Allianz Life, the perennial leader of the FIA space.

© 2019 RIJ Publishing LLC. All rights reserved.