Before income-generating annuities can become a common feature in 401(k) plans—as they are in TIAA’s 403(b) plans—plan recordkeepers will need an easier way to swap data with the life insurers who badly want to market annuities through those plans.

The SECURE Act of 2019 partly relieved plan sponsors of legal anxiety about offering annuities. But it didn’t solve the need for headache-free administration of annuities, which, like molting insects, are born in plans and take flight after participants retire.

“With the passage of the SECURE Act, the fiduciary concern is no longer the primary concern,” said Mike Westhoven, who has worked for years on this issue. “So the top concern now is about administration. All parties know they can’t have messy one-off connections. They want one place to access data on a variety of products.”

Westhoven now works for Micruity, a tech startup with a blueprint for the much-needed data hub. He and Micruity CEO Trevor Gary have been running demos of their “middleware” solution for asset managers and life insurers, who could include it in their proposals to plan sponsors.

Trevor Gary

Micruity’s solution can accommodate the inclusion of any type of annuity in a 401(k) plan. That flexibility is essential, because 401(k) annuity can take many shapes. The annuity can be purchased in or outside the plan, and with multiple premiums or a lump sum. It can require an “opt-in” by the participant or use a default.

As for the contract itself, it might be a permanently liquid deferred variable annuity, or an irrevocable life annuity, or a tax-deferred QLAC (qualified longevity annuity contract). The participant might switch on the guaranteed income stream at retirement, or after 10 to 20 years, or never. The plan sponsor might offer annuities from one insurer or from two or three. Given the evolving state of this industry, all options are on the table.

The ‘admin’ problem

Selling one annuity to a retail client can be complicated; scaling the sale of dozens or hundreds annuities to waves of retiring plan participants every year is much more so. The plan’s existing stakeholders—the recordkeeper, asset managers and participants—need to accommodate the data needs of one or more annuity providers.

“You need a system to keep the books and records straight,” said Mark Fortier, who in 2012 helped add income riders from three life insurers to an AllianceBernstein TDF in United Technology Corp.’s 401(k) plan. “Someone needs to connect the recordkeeper data with the insurer data, the way it’s currently done on the investment side. You need an entity in the middle.”

Ideally, there should be a single point of contact where every entity can access all the data that’s required to fund participants’ annuities, close the sale of the annuity at retirement, and make sure participants receive checks at the correct addresses throughout retirement.

Enter Micruity

Less than three years ago, Toronto native Trevor Gary was on the pension actuarial team at Deloitte Canada working on longevity risk swaps. Recognizing the need for personal pensions in the U.S., he decided to build a retail app with which individuals could calculate the gap between their expected retirement expenses and their expected Social Security benefits.

“Then on the back end of the app, our system would enable people to pay as little as $100 would be the Micruity system, where people could contribute $100 every payday to an annuity,” Gary, who is 30, told RIJ recently. “We would have annuities from eight different providers. I wanted to build it on the blockchain. Everybody took a meeting with me but they all said, ‘You’re nuts.’”

Instead, Micruity spent four months in a tech incubator program in Des Moines, the Global Insurance Accelerator, getting mentored by life insurance executives. There Gary learned about the opportunity in the 401(k) annuity space for a service that could track participant data to and through retirement. after they’d bought annuities and retired.

“The [life insurers] said, ‘When people leave the plan, we need to be able to track them.’ That was the Eureka moment for me,” Gary said. “From there, we built our current system from scratch.”

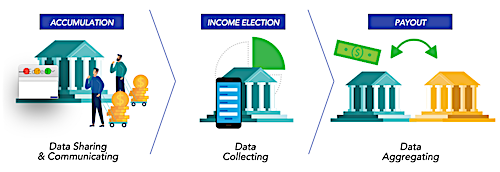

Last April, Micruity made presentations of his system to an audience at SPARK, the association of recordkeepers. This spring, Gary and Westhoven produced a webinar on the Micruity system called, “Making Lifetime Income Real.” As they explain in the webinar, Micruity’s product has three components:

- ‘Accumulation’ product. The most common in-plan annuity design is a deferred variable annuity with a guaranteed lifetime withdrawal benefit (i.e., a target date fund with a GLWB). When a participant in such a fund reaches age 50 or 55, Micruity would start collecting data from the plan recordkeeper and sharing it with a life insurer, which would begin assessing an annual fee in return for putting a floor under the participant’s “benefit base”—the basis for calculating the participant’s minimum annual income in retirement.

- ‘Income Election’ product. As groups of participants reach retirement age, Micruity would facilitate an “Income Election Decision Experience.” “We’re the data conduit sitting in the middle,” Gary told RIJ. “We can move that data in a frictionless, secure way. In a single sitting, we validate the participants’ identification and banking information. We enable them to e-sign a contract or certificate and provide a digital notary. We digitize the whole process.”

- ‘Payment Aggregation’ product. Depending on the kind of annuity purchased, the retiree might receive regular income from multiple insurers. Income might begin immediately after retiring, at a specific age, or whenever the retiree wishes. With GLWB products, the asset manager handles the payments. For non-GLWB products, Micruity would keep track of address changes, aggregate payouts from the several life insurers and issue checks. It also provides an online service center and call center support. Micruity’s fees for the TDF provider and life insurer could be AUM-based or transaction-based, and “could range from five to fifteen basis points depending on the product design and Micruity services,” Gary said.

“The sponsor is thinking, ‘This is a new product, so how do we make the process as frictionless as possible?’ Westhoven said. “They don’t want to add a speed bump that makes it difficult to use. With participants, there’s no such thing as a speed bump; every obstacle to usage is more like a brick wall.”

Mike Westhoven

Outside observers are encouraged by Micruity’s efforts so far. “The data hub and administration is the foundation, but Micruity could probably help on the participant experience and education, if stakeholders desire,” said Fortier. “Data-privacy, administration, and the regulatory aspects of education between recordkeepers and insurers have risks that have challenged the unbundled approach in the past.”

Robert Melia, the executive director of the Institutional Retirement Income Council (IRIC), a coalition of plan providers started by Prudential when it launched its IncomeFlex TDF/GLWB, told RIJ that Micruity could bring standardization to what is still a disjointed business.

“Micruity could say, ‘Let us provide these services, and we’ll establish the standardization that’s needed to drive annuities in DC plans,’” Melia said. “They have the credibility, the reputation and the knowledge to put it all together. Standardization, more than anything else, might propel the income part of the DC industry into the future.”

Not much demand yet

Legal liabilities and data gaps are not the only things stopping plan sponsors from adopting annuities. Participants aren’t demanding annuities, or pressuring employers to offer them—though that’s not necessarily a deterrent for Micruity and its clients. (“The plan sponsors say that participants aren’t asking for annuities. But participants didn’t beg for TDFs either,” Westhoven told RIJ.)

Micruity’s End-to-End Service

Lack of active demand for annuities could be a problem, however. The target market for annuities includes participants who’ve been defaulted into TDFs. Their very passivity makes them attractive to annuity vendors, since they can be defaulted into a GLWB rider as they near retirement. But will plan sponsors acquiesce to such an arrangement, especially if the rider costs as much as 100 basis points per year?

Efforts by full-service plan providers like Prudential and Empower to market TDF/GLWB products to their institutional clients have yielded lackluster results. Westhoven’s former employer, DST Systems (since acquired by SS&C Technologies), created middleware called RICC (for “Retirement Income Clearinghouse Calculator”), but it has remained largely on the shelf.

Historically, annuities have shown the most promise in two distinct types of plans. They appear to work well in 403(b) plans, where millions of people have access to TIAA annuities. They also seem to be a good fit at large companies that recently closed defined benefit pensions and where a critical mass of employees misses an income option. United Technologies is the singular example of such a company.

Micruity will be aiming its future marketing efforts at just such large firms. “We’re looking at the top 1,600 plans, with a combined 20 million or more participants, Gary told RIJ. “These plans have strong human resource teams, and often have a unionized or union-like environment. They employ a lot of mid-market Americans, and their turnover rate is low as they get closer to retirement. These are the plans where it will start. And once momentum catches on, changes will trickle down to smaller plans.”

© 2020 RIJ Publishing LLC. All rights reserved.