It’s too soon to say if, when or how it will affect the way Americans save for retirement, but the trend is undeniable: asset managers are creating target-date collective trust funds at a rapid rate and pitching them to 401(k) plan sponsors.

“They still have issues, but they’re gaining traction,” said one 401(k) platform provider who asked not to be identified. His firm offers a range of exchange-traded funds, CTFs, and mutual funds to plan sponsors.

Of the 159 collective trust funds (CTFs) that were launched in 2009, 115 (72%) were formed as vehicles for lifecycle or target date investing strategies. From 2007 to 2009, 439 CTFs were formed, of which 241 (55%) were target date CTFs.

Both collective trusts and target date funds—especially TDFs—were handed a ready-made market when they were approved as QDIAs (qualified default investment alternatives) for 401(k) plans by the Pension Protection Act of 2006.

| Top-20 US Collective Trust Fund Managers and Total Assets, 2Q 2009 ($ billions) |

|||

|---|---|---|---|

| Rank | Firm | 2Q 2009 Assets | Q 2009 Marketshare |

| 1 | BlackRock1 | $388.2 | 37.8% |

| 2 | State Street Global Advisors Ltd. | $123.4 | 12.0% |

| 3 | Northern Trust Global Investment Services | $118.9 | 11.6% |

| 4 | BNY Mellon | $110.6 | 10.8% |

| 5 | Fidelity Investments | $65.0 | 6.3% |

| 6 | Invesco National Trust Co. | $40.8 | 4.0% |

| 7 | Old Mutual Asset Management Trust Co. | $26.2 | 2.5% |

| 8 | Galliard Capital Management Inc. | $17.8 | 1.7% |

| 9 | The Vanguard Group, Inc. | $13.1 | 1.3% |

| 10 | UBS Realty Investors LLC | $10.3 | 1.0% |

| 11 | Capital Guardian Trust Company | $10.0 | 1.0% |

| 12 | Ameriprise Trust Company | $9.5 | 0.9% |

| 13 | Wilmington Trust RISC | $6.3 | 0.6% |

| 14 | Schroders Investment Mgt North America | $5.6 | 0.5% |

| 15 | Amalgamated Bank | $4.8 | 0.5% |

| 16 | Fortis Investments USA, Inc. | $4.4 | 0.4% |

| 17 | Genesis Asset Managers, LLP | $4.4 | 0.4% |

| 18 | Morley Financial | $4.0 | 0.4% |

| 19 | Prudential Private Placement Investor, L.P. | $3.5 | 0.3% |

| 20 | AFL-CIO Housing Investment Trust | $3.6 | 0.3% |

| Total CTF market | $1,027.7 | ||

| 1Formerly Barclays Global Investors NA | |||

| Sources: Morningstar Direct, Cerulli Associates | |||

Leading the charge

The largest CTF provider is BlackRock, which has a 38% market share, according to Cerulli Associates. Just four firms, BlackRock (formerly Barclays Global Investors), State Street Global Advisors, Northern Trust, and BNY Mellon, account for 72% of the $1 trillion-plus CTF business in the U.S.

“It’s my understanding that the bigger firms are leading the charge into target-date CTFs,” said Jake Hartnett, senior analyst, Institutional Asset Management, at Cerulli Associates. “Pyramis, Fidelity’s institutional money manager, has come out with them. BlackRock also has a TDF-CTF product.”

“We have cloned a Freedom Fund collective trust,” said Beth McHugh, a Fidelity vice president, referring to Fidelity’s proprietary line of target date funds. “They’re fairly recent and they’re not available to everyone. We also have other multi-fund collective trusts.”

“The trend has been shared among various providers,” said Steve Deutsch, who tracks CTFs for Morningstar, Inc. “BlackRock, Putnam and Nuveen are there, but also smaller firms like Avatar Associates and Manning & Napier. Since CTFs are unregistered, you’ll see a mix of established firms as well as boutiques and smaller firms that can’t afford to go through the cost and time of registration.”

According to Cerulli, CTF assets peaked at $1.43 trillion in 2007 after five years of steady growth. The “flight to quality” in 2008 and 2009 cut their assets to $1.07 trillion in 2008 and $1.03 trillion last year. Of that trillion, about 28% is in DC plans and 72% in DB plans. Morningstar estimates the CTF total at about $1.6 trillion, with about half in DB and half in DC.

That’s still only a fraction of the $13.4 trillion that Americans hold in retirement accounts, in the form of mutual funds, exchange traded funds, variable annuity separate accounts, and individual stocks, as well as CTFs.

Made for each other

Because CTFs are marketed only to institutions, and not to the public as mutual funds are, they do not need to submit a prospectus to the Securities and Exchange Commission for approval and provide one to every potential investor. They are supervised by banking regulators rather than by the SEC.

Advertisement

But TDF-CTFs aren’t merely wholesale, bank-regulated versions of target-date mutual funds.

“We have compared target date mutual funds and TDF-CTFs from same firm,” Deutsch said. “While they may have the same name and the same target date in their objective or strategy, you’ll get completely different money managers running them, different investment decision processes, different allocations and different return streams. They’re not just low-cost clones of mutual funds.”

Cerulli’s Hartnett thinks the CTF structure will actually enhance the target date strategy, because it will make it easier than ever for target date fund managers to hold alternative assets as they seek more sophisticated, institutional-style diversification.

“The target date format and the CTF structure are made for each other,” he said. “Part of the TDF solution, which even in the mutual fund format includes getting exposure to non-correlated assets, is to bring a more institutional level of management to DC plans.”

Presenting the target-date investment strategy in a CTF wrapper will also relieve some of the fiduciary burden from plan sponsors, Hartnett said. By statute, the trustees of CTFs have fiduciary responsibilities that mutual fund managers do not. They can relieve that burden from plan sponsors, or at least share it.

“Because [CTFs] are bank-registered products, you have an external fiduciary joining the plan sponsor,” he added. “Plan sponsors like that. If the asset manager is using a ‘40 Act’ [i.e., Securities Act of 1940] mutual fund format, there’s no co-fiduciary. From what we’ve heard, that makes the CTF an easier sell. We’ve also heard that Taft-Hartley plans [multi- employer union-sponsored DC plans] are more comfortable with CTFs.”

“Because [CTFs] are bank-registered products, you have an external fiduciary joining the plan sponsor,” he added. “Plan sponsors like that. If the asset manager is using a ‘40 Act’ [i.e., Securities Act of 1940] mutual fund format, there’s no co-fiduciary. From what we’ve heard, that makes the CTF an easier sell. We’ve also heard that Taft-Hartley plans [multi- employer union-sponsored DC plans] are more comfortable with CTFs.”

The percentage of defined contribution plans offering mutual funds declined to 54% from 65% over the six-year period from 2003 to 2008, according to Morningstar. Meanwhile, a higher percentage of plans are using institutional mutual funds (to 80% of plans from 72%), of collective trusts (to 45% from 32%) and separate accounts (to 29% from 24%).

Ironically, CTFs were the investment structure of choice in defined contribution plans during the early days of the 401(k) phenomenon—a holdover from DB practices.

But as the mutual fund business grew, mutual funds supplanted CTFs in DC plans. Mutual funds, which were built for the retail market, have traditionally been more transparent than CTFs in terms of offering prospectuses and daily valuations. But they are more expensive.

Back to the future

Now the pendulum has swung the other way. Precisely because they don’t market to the general public and don’t have to meet a heavy regulatory burden, CTFs operate more cheaply than mutual funds—especially actively managed funds.

In response to consumer and government pressure to cut plan costs, plan sponsors have become increasingly receptive to a variety of low-cost alternatives, including index funds, institutional mutual funds, exchange traded funds, separate accounts, and CTFs.

“Collective trusts, separately managed accounts and institutionally priced mutual funds all have advantages,” said David Wray, president of the Profit Sharing Council of America, an organization of large 401(k) plan sponsors. “There is no single right answer.”

The positioning of target date funds in collective trusts won’t necessarily resolve certain problematic aspects of target-date funds, however. The problems, which were reviewed in Senate hearings last year, include the wide variation in TDF design and the difficulty that investors have in benchmarking TDF performance.

The hearings also revealed that many investors believed that by investing in target date funds, they would reach retirement with adequate savings and that the volatility of their savings would taper off by retirement.

In fact, until they experienced steep losses in 2008, many TDF investors had no idea that so much of their money was at risk. The very fact that TDFs were dated created a false impression that they would protect investors from the market risk associated with an ill-timed retirement.

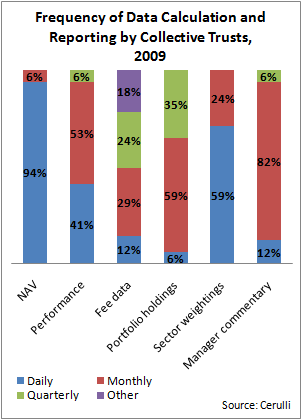

When packaged inside CTFs, which are less transparent than mutual funds, TDFs are not likely to be any more understandable to the average plan participant than they were before. Whether there’s the seed of a crisis in the wedding of these two strategies remains to be seen.

© 2010 RIJ Publishing. All rights reserved.