The co-founders of ALEXIncome, Ramsey Smith and E. Graham Clark, believe they’ve “built the best process for integrating annuities into retirement accounts.” Their philosophy is similar to the TIAA/Nuveen Secure Income Account (SIA), which combines a group deferred income annuity with a Nuveen target date fund.

As an application of the now-familiar internet platform model, ALEXIncome will try to serve would-be players in the rapidly expanding 401(k) annuity space—like target date fund (TDF) providers and annuity issuers—by connecting them with partners, capabilities, or data that will help them get started.

Ramsey Smith

“We’re a product design firm,” Clark said in a phone interview. “We can work with an asset manager, carrier, or recordkeeper to design an annuity that fits into their target date structure and hook up all the other components.”

In an email, Smith added, “We call our product a ‘flexible premium deferred annuity. We chose the structure for its simplicity and scalability, in the face of a retirement income opportunity that will eventually test the capacity of the life insurance industry.”

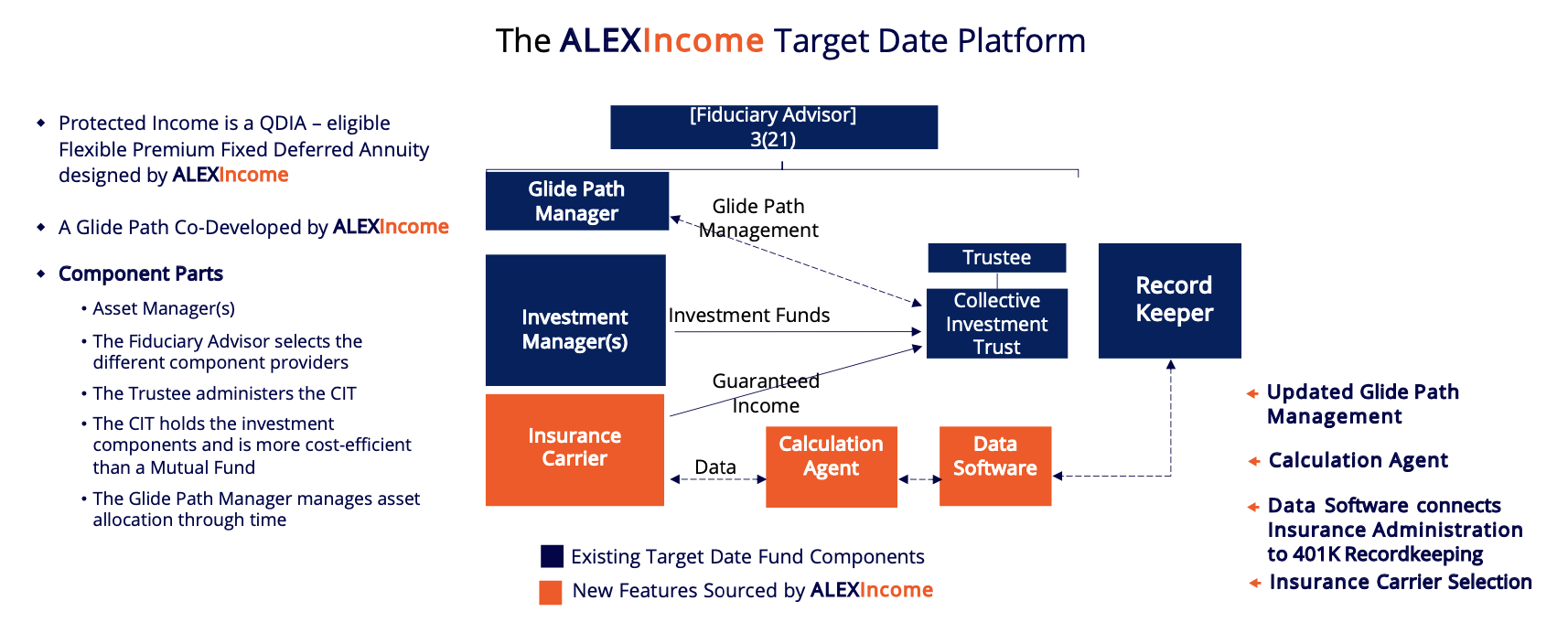

ALEXIncome embeds a deferred group annuity into a TDF. Since TDFs can be “qualified default investment alternatives,” 401(k) plan participants who neglect to choose their own investments can be automatically assigned to invest in them. ALEXIncome would modify TDFs to allocate participants’ contributions from bond funds to the deferred annuity, starting as early as age 40. Individual group annuity accounts would be marked to book value, not market value.

As they do at TIAA, ALEXIncome’s group annuity accounts could grow faster than bond funds because they’d be less liquid—but still liquid enough to satisfy 401(k) requirements. At retirement, participants could apply the account value to the purchase of an immediate income annuity or perhaps (as a future ALEXIncome product extension) a Qualified Longevity Annuity Contract, which postpones the payout of monthly income until age 80 or so.

Over time, “we entirely replace the fixed income allocation with the annuity allocation, and we never sell the annuity [during the accumulation period]. The crediting rate resets every year. If you do it our way, and you start it early, this method will generally outperform bond-based and other guaranteed income-drive TDF strategies,” Clark told RIJ.

E. Graham Clark

“Our defining intuitions were,” he said, “that contributions to the group annuity inside the TDF should start earlier in the participant’s career and that the deferred group annuity would always be priced at book value. That’s what drives performance. That’s the secret sauce. Ideally, we would have allocated part of participants’ balances to traditional deferred income annuities [and lock-in chunks of future income prior to retirement], but that’s not eligible in an ERISA plan. So we did the next best thing.

“If the 401(k) plan sponsor decides to replace the annuity contract or the insurance carrier, the carrier will pay the assets back to the plan over six years at book value or pay the assets to the plan immediately with a market value adjustment. This protects the carrier from the risk of losing the entire liability at once and allows it to invest in a longer duration and hopefully a better crediting rate for participants.

“We believe that TIAA’s experience is that their annuity account in 403(b) have a low and stable annual surrender rate. We also have access to historical data about how many people will move in and out, because plans had already had that experience with their existing QDIA investment. We can pay participants a lump sum or partial lump sum at retirement,” Clark said.

ALEXIncome echoes the design of “SponsorMatch.” In 2007, MetLife and Barclays Global Investors proposed a plan where the participant’s own salary-deferral would go into a traditional 401(k) account while the sponsor’s matching contribution would go into a group annuity—leading to an optional income annuity at retirement. That program vanished in the Great Financial Crisis.

Kevin Hanney

Kevin Hanney, an independent pension trustee, told RIJ, “ALEXIncome is similar to what we were looking at when I left RTX. There’s a floor on the market value and guaranteed accrual. We arrived at similar conclusions: That participants must start contributing to the group annuity early and that, by reducing the variability of your performance, you improve your long term return.

“The tortoise and the hare is a pretty good analogy. A slow and steady pace can improve your compounded annual return by 50 to 100 basis points, even in less volatile conditions.” Hanney was in charge of pension investments at United Technologies (now RTX, since its 2020 merger with Raytheon) when it switched its retirement benefit from a defined benefit plan to a variable annuity with a guaranteed lifetime withdrawal benefit, underwritten by three life insurers.

The co-founders of ALEXIncome also have large-company experience. Clark and Smith each spent years with big Wall Street firms. Smith was a managing director at Goldman Sachs for more than 20 years. In 2018, he started Alexfyi, a digital insurance agency specializing in the distribution of fixed-rate annuities, including the Nassau Simple Annuity. (Alexfyi was named in honor of Alexander Hamilton.)

Alexfyi collaborated with Nassau Financial on the development of “That Annuity Show,” which has run for more than 200 episodes. Clark, an insurance solutions specialist, was a managing director at BNP Paribas, Merrill Lynch and Citigroup. A self-described “derivatives geek,” Clark is also a cigar aficionado and a model railroad hobbyist. Both men sport Ivy MBAs: Smith from Harvard and Clark from Cornell.

As for ALEXIncome’s own business model, “we offer ourselves as a consultant to help asset managers, insurers and recordkeepers get into the 401(k) business. Today we get a monthly retainer or a project fee. Our flexible deferred annuity is a spread product, with no fees, and the carrier can pay all of the component providers out of its spread because of the lower administration cost of the product,” Clark said.

Today, ALEXIncome’s primary customers are carriers. If Smith and Clark partner with a specific life/annuity company on a bundled solution, plan sponsors would become its customers as well. “If we do the ‘build’ all the way through—that is, if we partner with a carrier and bring in the other service providers—part of our contract would include some basis points on AUM for us. But that’s down the road,” Clark told RIJ.

© 2024 RIJ Publishing LLC.