Follow the money. That adage was true for Woodward and Bernstein (first and second wave boomers will recall them) and it’s true for just about everyone who plays in the retirement income space.

Right now, retirement savings is moving into IRAs from 401(k) plans faster than ever. According to a new Cogent Research survey called “Assets in Motion 2010,” for the first time there’s more retirement money in IRAs than in employer-sponsored plans (ESRPs).

According to the Investment Company Institute (ICI), there was $4.2 trillion in IRAs and $4.1 trillion in defined contribution retirement plans.

Mutual fund companies/IRA custodians have been competing for rollover dollars for years. The dynamics are changing, however, with plan sponsors and providers saying they want to retain plan assets—perhaps because they’re feeling an increase in the negative flow.

Winners and losers have already emerged in the rollover battle, Cogent’s survey shows. Fidelity Investments and the Vanguard Group, for instance, are disproportionate recipients of rollover money, both as IRA custodians and as asset managers.

Almost 40% of affluent investors who expect to execute a rollover in the next 12 months told Cogent they plan to take their money to just five companies: Fidelity, Vanguard, Charles Schwab, Wells Fargo/Wachovia and Edward Jones. Another 21% weren’t sure where they would take their money.

That leaves only crumbs for two dozen other large firms. Indeed, rollovers have been a net drain for most asset managers—despite years of marketing and advertising campaigns.

As Cogent points out, “While the asset management industry has spent millions promoting their Rollover IRA capabilities, very few firms have been able to acquire a large number of rollover assets.”

It will surprise few people that much of the rollover money flows to Fidelity and Vanguard. For millions of plan participants, it’s a quick and easy step from one of Vanguard’s and Fidelity’s 401k plans to their IRAs and their no-load mutual funds.

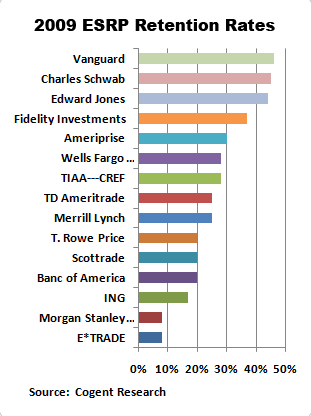

The ESRP providers with the highest retention rate (percentage of customers likely to choose the same firm as their IRA custodian are Vanguard (46%), Charles Schwab (45%), Edward Jones (44%) and Fidelity (37%).

The ESRP providers with the highest retention rate (percentage of customers likely to choose the same firm as their IRA custodian are Vanguard (46%), Charles Schwab (45%), Edward Jones (44%) and Fidelity (37%).

Each of those firms offers low costs, lots of investment options, powerful brands (read: a deep reservoir of trust) and robust online and toll-free telephone services. Schwab (“Talk to Chuck”) and Fidelity (The “Green Line”) have strong marketing themes. Vanguard, not a prolific advertiser, has some interesting taglines, like “Would you buy this newspaper if it costs five times as much?”

Cogent’s findings are based on a survey of 4,000 American adults of all ages with $100,000 or more in investable assets. The median age of the participants was 57, 30% were fully retired, and 36% had assets over $500,000. About two-thirds work with financial advisors.

The number of investors and account owners in IRAs is rising (31% and 37%, respectively) while participation in ESRPs is falling, (by 25% and 42%, respectively), the survey showed. Among affluent investors, ownership of ESRPs dropped to 59% in 2009 from 77% in 2006. It dropped to only 29% last year among the oldest (and presumably retired) investors. Three years ago, it was 63%.

Beginning around age 54, savers have more money in IRAs than in ESRPs, the study shows. Gen X&Y and Second Wave Boomers have more money in ESRPs, but First Wave Boomers have more money in IRAs.

But only about one in ten (11%) of affluent investors in the survey expected to roll over money from an ESRP to an IRA in the next 12 months. Among those, 44% were “very likely” or “extremely likely” to rollover.

Still, Cogent extrapolated that to mean 5.9 million households were at least contemplating a rollover soon. Of all age groups, the Second Wave Boomers were most likely (15%) to roll over. Their 401(k)s had an average value of about $111,000.

Asset managers and plan providers need to act before the money finds a permanent home, Cogent says. “Mutual fund and 401(k) providers with asset management capabilities should seek to partner with distributors that are likely to gain most of the Rollover IRA assets over the next 12 months,” the Assets in Motion report said.

“Smart 401(k) providers should help key distributors, particularly advisors, identify Rollover IRA candidates within the plan. In addition, smart DCIO providers should work directly with home office contacts and their financial advisors to create value-added Rollover IRA materials and campaigns that distributors can use to attract and retain assets,” the report continued.

Data from other organizations adds to the picture of rollover behavior. In late 2007, the Investment Company Institute (ICI) surveyed recent retirees who had actively participated in defined contribution plans about how they used plan proceeds at retirement.

Just over half (52%) took lump-sum distributions, and another 7% received part of their distributions as a lump sum. The remaining retirees either delayed their withdrawal, received their distribution as annuities or installment payments, or chose some combination of options that excluded a lump sum.

Of those who took lump sums, only 14% of respondents in the ICI study, with only 7% of the assets, spent their entire distribution. The other 86% reinvested their money. Of those, 65% rolled everything to an IRA and an additional 23% rolled part of the money to an IRA.

© 2010 RIJ Publishing. All rights reserved.