Louis S. Harvey, the founder of Dalbar, a kind of J.D. Power for the financial services industry, analyzed stock market history and found that since 1940 US equities have always recovered, even in real terms, within five years of any crash.

He uses that finding—which might surprise a few people—as the basis for a portfolio asset allocation strategy that he’s now sharing with the world.

In a recent white paper, Harvey asks, Is an “Arbitrary Asset Allocation” more efficient than a “Prudent Asset Allocation.” By “arbitrary,’ he means setting a ratio of stocks and bonds according to an investor’s current risk tolerance and then rebalancing the portfolio back to the same ratio if the winds of volatility drive it off course.

By “Prudent Asset Allocation” Harvey means something different. His prudent approach involves two buckets. The first bucket should contain enough safe (“preservative” or “protection”) assets to cover cash needs (in excess of expected income) for the next five years.

The second bucket, including the rest of the client’s investable money, goes into growth assets. Once a year, the preservative bucket gets replenished with gains, if needed, from the growth bucket. The rolling five-year buffer, like the shadow of an eclipse crossing the landscape, moves one year forward.

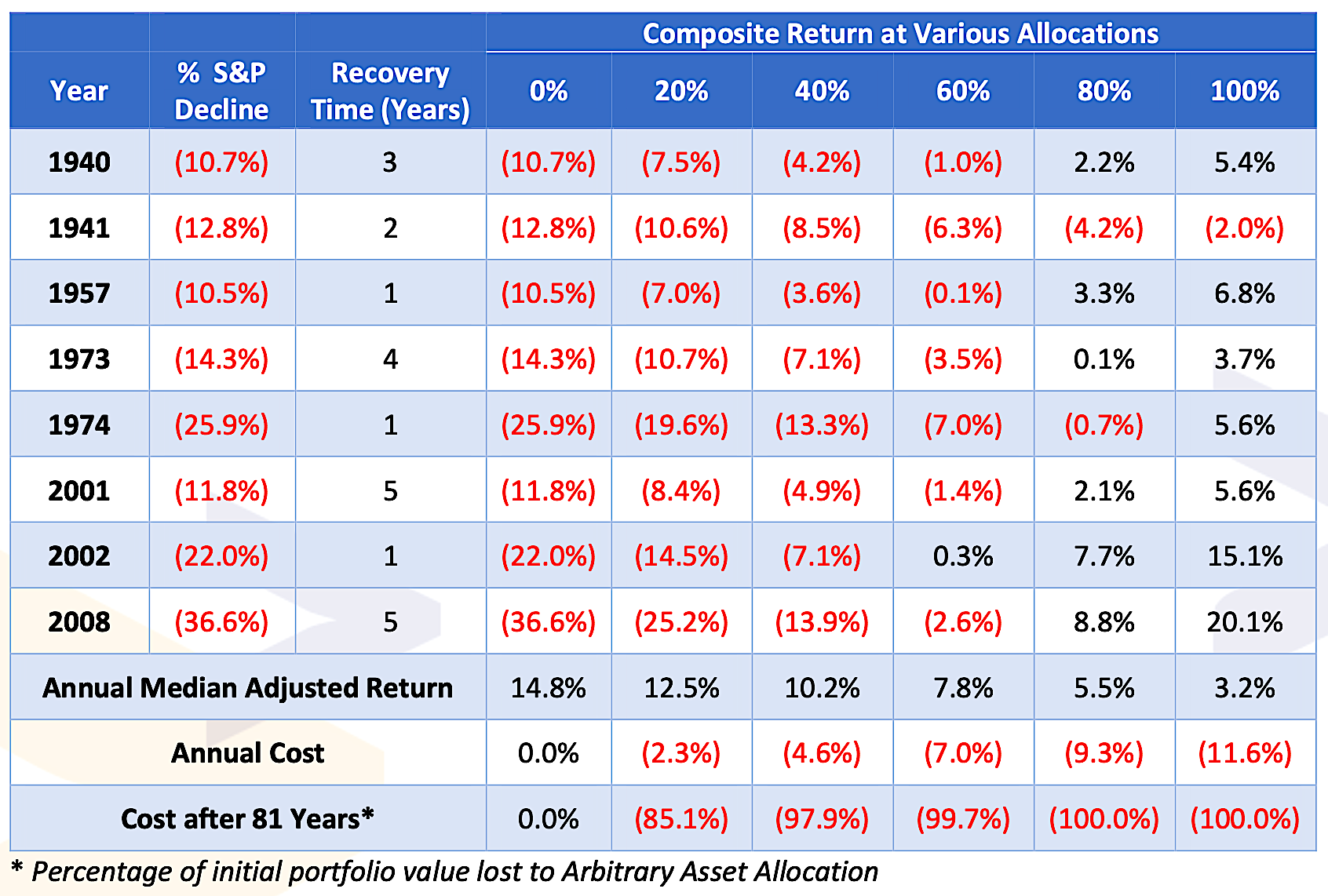

“We said, let’s examine every possible combination in history to find the maximum recovery period for stocks—the longest it ever took for equities to recover their pre-crash value—and it came out to about 4.9 years,” Harvey told RIJ recently. “In the worst case scenario, if you have a diversified portfolio, you are more than likely to recover your losses in five years or less.”

The five-year buffer

Born in Puerto Barrios, Guatemala in 1942, Harvey emigrated to the US with a degree in physics from the University of the West Indies. He started Marlborough, MA-based Dalbar in 1976. Dalbar surveys financial services providers, establishes benchmarks for quality, publishes syndicated research and gives out awards. Harvey based the “Prudent Asset Allocation” technique on his own experience as an investor.

Here’s how it works:

- Set up a bucket of safe assets equal to the difference between expected income (salary, Social Security, pension benefits, systematic withdrawals from a 401(k) plan) and spending needs over the next five years.

- Safe assets include principal-guaranteed products, guaranteed income investments, FDIC-covered savings, US Treasuries, money market mutual funds, other cash equivalent securities.

- When market conditions are favorable (anytime but right after a decline, before a full recovery), growth assets (individual securities, are sold to replenish the protection bucket.

- If there is a buildup of Preservative assets from rising income or windfalls (or appreciation of the Preservative assets net of spending), the excess goes into the Growth class.

- The process is applied during an annual reevaluation. The procedure is intended to continuously deplete the Preservative assets at a rate that is slower than the growth of the Growth class.

- Revisit the strategy when there’s a major change in circumstance, such as an inheritance, retirement, job change, birth or divorce.

“The procedure is intended to continuously deplete the Preservative assets at a rate that is slower than the growth of the growth class,” Harvey writes. “When market conditions are favorable, Growth assets are used to replenish the Preservative class,” the white paper said. “Favorable conditions are considered to be any time except immediately following a decline, before a full recovery is achieved.”

Stocks have always rebounded

Louis S. Harvey

The Prudent method is grounded in Harvey’s finding that stocks have crashed less often and their prices have bounced back faster than a lot of loss-leery investors tend to assume or imagine. According to his back-testing exercises, the S&P 500 Index fell 10% or more in only eight calendar years since 1940 (see chart below) and took no more than five years to recover the loss.

Ipso facto, an investor should be able to maximize returns and keep anxiety far away—a sustainable armistice between greed and fear—by hoarding enough cash to avoid a forced sale of depressed assets for up to five years and stretching for growth with the rest.

Before you run to your spreadsheets to prove that this two-bucket approach is an illusion (because a balanced fund performs the same as two one-asset funds), or purely behavioral (i.e., prevents panic-selling) or impossible to prove (because no two plans will ever perform identically), or rife with market-timing issues, remember that Harvey isn’t claiming that the Prudent method optimizes a portfolio. He’s saying that it outperforms the popular Arbitrary method and relieves stress.

Back-testing the Prudent allocation method vs the Arbitrary allocation method over the score of years from 2001 to 2020, Harvey found that his strategy beat an arbitrary portfolio of 60% stocks (S&P 500 Index) and 40% bonds (10-Year Treasuries) and found:

- In 13 (65%) of the 20 years, total return for a one-year time horizon was superior for the Prudent Asset Allocation

- In 12 (60%) of the 20 years, total return for a ten-year time horizon was superior for PAA

- For the years 2010 to 2020, PAA outperformed AAA in one-year returns (23.78% to 15.58%)

- For the years PAA outperformed AAA in ten year returns (98.62% to 60.94%)

- Where the Arbitrary method outperformed, the Prudent method allowed the investor to wait (up to five years) for a market recovery instead of selling in a down market

“The arbitrary method is not focused on what’s changing in the market place, or in the investor’s personal circumstances,” Harvey said. Instead, “We suggest that you have an annual schedule unless there’s an extraordinary event—such as the market going berserk. If it’s significant, go back and revisit your asset allocation.”

Good for decumulation or accumulation

Harvey’s approach is intended to work for people of all ages, in either the “accumulation stage” before retirement or the decumulation stage” after retirement. “People at older ages, who no longer have an earned income, can substitute their Social Security income for earned income and perform exactly the same calculation. It is most applicable in the decumulation stage, but also in the appreciation stage,” he said.

“When you look at society, you can see that so many people are in both stages. You can’t reasonably draw a line between the two. So many people are working and receiving retirement income at the same time. The same principle applies, regardless of how old you are, even if the numbers change.” [I assume that Harvey would recommend dealing separately with tax-favored accounts and not incorporating them into the Prudent method until after retirement.]

“If you have millions of dollars, you might need to hold only two or three percent of your net worth to cover the next five years. The method is also totally fluid; it’s just a function of your net cash needs,” he added. In other words, the more total savings you have, relative to your need for excess cash each year, the easier it is to run this strategy, and vice-versa.

The Prudent method accommodates almost any selection of growth assets. “It doesn’t have to be stocks,” Harvey said. “If you feel comfortable with alternative assets or options, go ahead and use them. You can make that determination yourself. The amount of risk you take will depend on your personal preference or gut and skill. Using risk ‘appetite’ to determine asset allocation, without segmentation, without consideration of income needs, is a cruel waste.”

Harvey acknowledges, without apology to the bucketing-skeptics, that the Prudent method is a kind of bucketing or time-segmentation. “It’s 100% supportive of time segmentation. One of our goals was to make it real simple. Using expressions like ‘bucketing’ or ‘time-segmentation’ can make it sound complicated. But any advisor and many individuals can implement it without rocket science.”

In calling for a rolling five-year window of safety, however, the Prudent method differs from retirement bucketing strategies that consist of, for example, four five-year buckets from age 65 to 85. In that strategy, each bucket’s assets grow for five, 10, or 15 years before they’re sold and the proceeds swept into the active spending bucket. The Prudent strategy calls for a rolling five-year buffer of safe assets.

“The bottom line of Prudent asset allocation is to have the confidence of knowing that over the next five years, you don’t have to worry about market conditions,” Harvey told RIJ. “It changes the character of your approach to risk, and it generally means that you can put more money into growth assets.”

© 2022 RIJ Publishing LLC. All rights reserved.