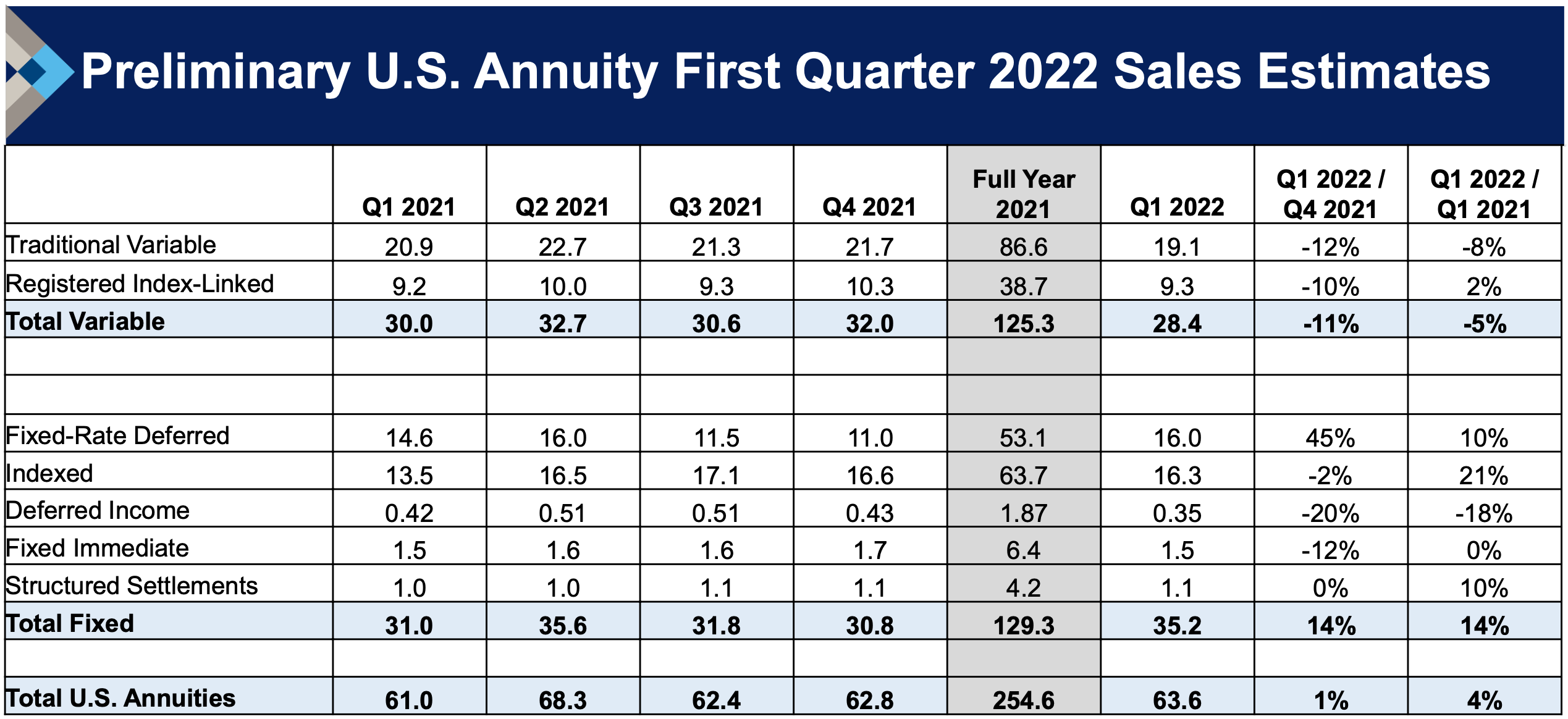

Total US annuity sales increased to $63.6 billion in the first quarter of 2022, up 4% from the first quarter of 2021, according to preliminary results from the LIMRA Secure Retirement Institute (SRI) US Individual Annuity Sales Survey.

At their current quarterly sales pace, annuities would post 2022 full-year sales of $254.4 billion, or just shy of the all-time record sales of $254.6 billion in 2021.

“First quarter annuity sales tend to be a bit slower,” said Todd Giesing, assistant vice president, SRI Annuity Research. “While sales in the first two months of 2022 were a bit sluggish, annuity sales in March were at record-high levels. Rising interest rates and increased market volatility shifted the product mix this quarter with fixed annuity products driving the overall growth.” SRI has tracked monthly annuity sales since 2014.

Total fixed annuity sales were $35.2 billion in 1Q2022, up 14% over first quarter 2021. Double-digit growth for fixed indexed annuities and fixed-rate deferred annuities returned the overall fixed annuity sales to pre-pandemic levels.

$ in billions. Source: Secure Retirement Institute, May 3, 2022.

Fixed indexed annuity (FIA) sales were $16.3 billion, 21% higher than in prior year quarter but down 2% from 4Q2021. Fixed-rate deferred annuity sales increased 10% in the first quarter, year-over-year to $16 billion. They were up 45% from 4Q2022.

“Both FIAs and fixed-rate deferred products benefited from the significant interest rate increases in the first quarter,” said Giesing. “Coupled with a nearly 5% equity market decline, investors sought out principal protection and steady growth, which these products offer.”

Sales of fixed-rate annuities and FIAs were $32.3 billion in 1Q2022, compared to $28.4 billion for all variable annuities. Combined sales of indexed products—FIAs and registered index-linked annuities, or RILAs—were $25.6 billion.

Index-linked annuities are, from that perspective, the single best-selling class of annuity products. The two occupy very different niches: FIAs are distributed through insurance marketing organizations and require an insurance license to sell, while RILAs are distributed through broker-dealers and require a securities license to sell.

Both are distinct from all other annuities, however, in that they are structured products. That is, their performance is tied to the performance of options on equity market indexes or hybrid indexes.

FAs and FIAs, especially those with longer contract terms, are the products favored by life/annuity companies that have close partnerships with alternative asset managers. The annuity companies are stoking their profitability by reducing exposure to capital intensive products like variable annuities with living benefits, investing in higher-yield private assets, and making strategic use of reinsurance in havens like Bermuda.

Traditional variable annuity (VA) sales were $19.1 billion in the first quarter, down 8% year-over-year. Registered index-linked annuity (RILA) sales were $9.3 billion. While this is 2% higher than first quarter 2021, it reflects a 10% drop from the fourth quarter of 2021.

“Market conditions in the first quarter have made FIAs more attractive than RILAs. As a result, the remarkable growth RILAs experienced over the past three years has leveled off,” Giesing said in a release.

Immediate income annuity sales were $1.5 billion in the first quarter, level with first quarter 2021. Deferred income annuity sales fell 18% to $300 million in the first quarter.

“We finally are beginning to see payout rate increases for income annuities as interest rates improve,” said Giesing. “However, because the Fed has signaled additional rate hikes later this year, we expect investors to wait to lock in rates so sales will likely remain muted in the second and third quarters.”

Preliminary first quarter 2022 annuity industry estimates are based on monthly reporting, representing 85% of the total market. A summary of the results can be found in LIMRA’s Fact Tank.

The 2021 top 20 rankings of total, variable and fixed annuity writers will be available in May, following the last of the earnings calls for the participating carriers.

© 2022 RIJ Publishing LLC.