The Federal Reserve’s Board of Governors released its annual Financial Stability Report this month. Portions of the 72-page document were devoted to statistics on the financial health of the US life insurance industry, which includes the annuity industry.

The report noted an overall increase in the liquidity of the industry’s liabilities and a trend toward holding less liquid assets—a potential cause of difficulty. Rising interest rates, the report said, could make life insurers more profitable, but also more susceptible to surrenders.

According to the report:

- Leverage at life insurers remained near its highest level of the past two decades. Life insurers continued to invest heavily in corporate bonds, collateralized loan obligations (CLOs), and commercial real estate (CRE) debt, which leaves their capital positions vulnerable to sudden drops in the value of these risky assets.

- Gradually rising interest rates improve the profitability outlook of life insurers, as their liabilities generally have longer effective durations than their assets, and higher interest rates may reduce life insurers’ incentives to invest in riskier assets.

- However, a large and unexpected increase in interest rates could induce policyholders to surrender their contracts at a higher-than-expected rate.

- If the increase in surrenders is substantial enough, it could put downward pressure on life insurers’ financial performance.

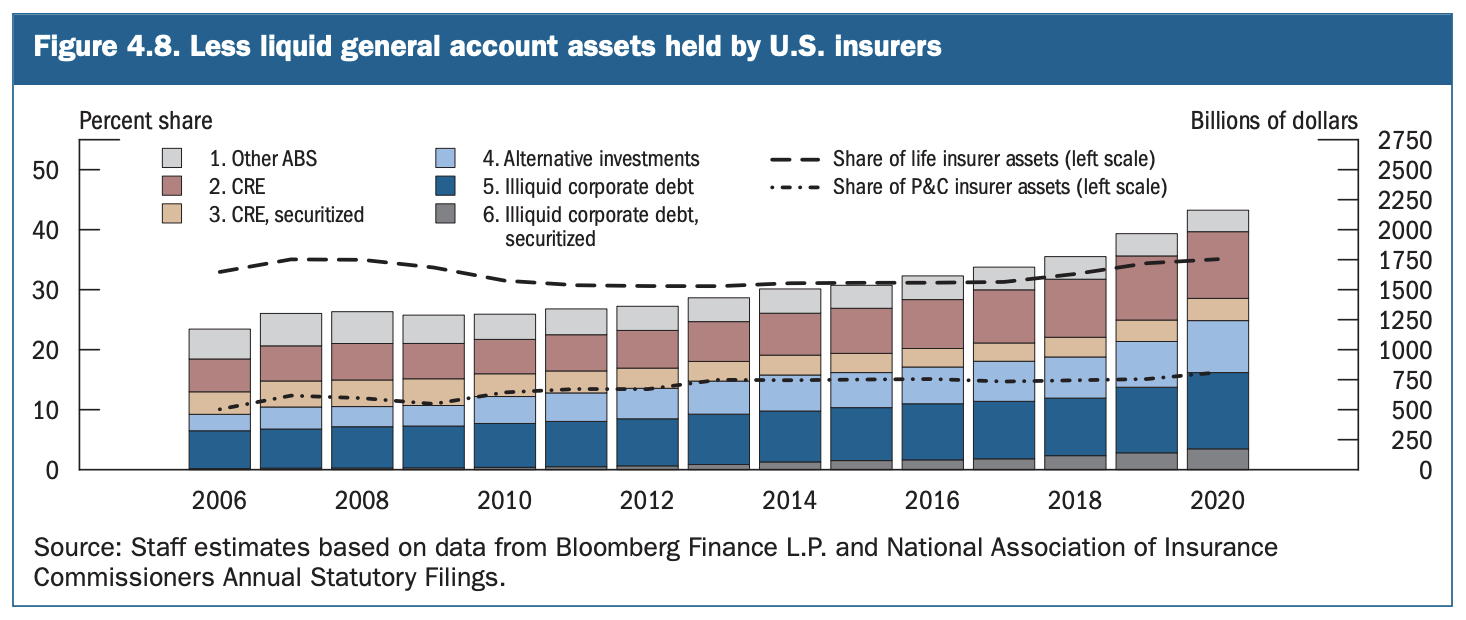

- Over the past decade, the liquidity of life insurers’ assets declined and the liquidity of their liabilities increased, potentially making it more difficult for life insurers to meet a sudden rise in withdrawals and other claims.

- On the asset side, life insurers increased the share of risky, illiquid assets—including CRE loans, less liquid corporate debt, and alternative investments—on their balance sheets.

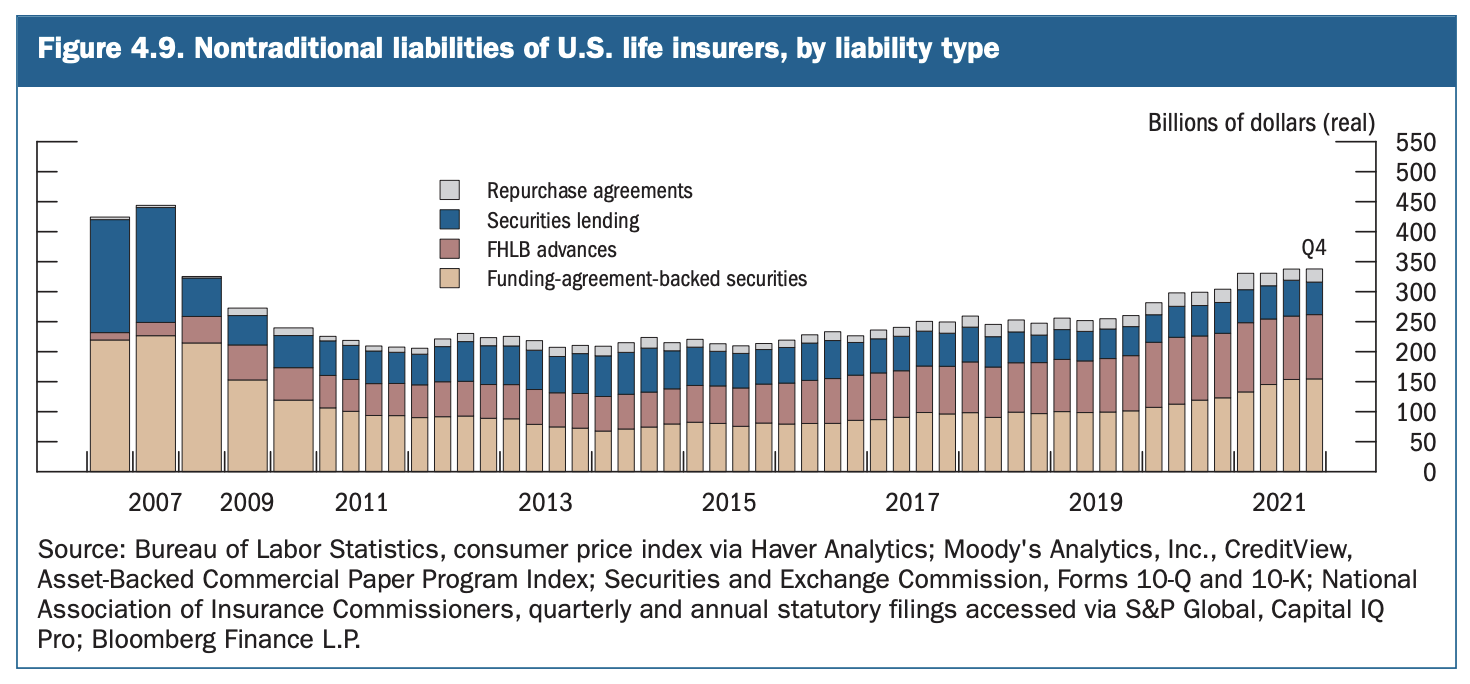

- Life insurers increasingly relied on nontraditional liabilities, such as funding-agreement-backed securities, Federal Home Loan Bank advances, and cash received through repurchase agreements and securities lending transactions.

- These liabilities, which are generally more vulnerable to rapid withdrawals than most policyholder liabilities, have grown steadily in recent years.

© 2022 RIJ Publishing LLC. All rights reserved.