Money market funds win, alternatives lose in Q1 2020: Cerulli

Investor fear and uncertainty fueled a flight to equity index funds and money market funds and away from other equity mutual funds and exchange-traded funds (ETFs) in the first quarter of 2020, according to a new issue of The Cerulli Edge–U.S. Monthly Product Trends.

Highlights from the report include:

- In total, investors pulled about $320 billion from mutual funds and ETFs during March, although passive U.S. equity ($40.9 billion) was exempt from the general trend. The demand for passive U.S. equity likely stems from investors reallocating to low-cost equity index-tracking products to take advantage of bargains.

- Asset managers suffered double-digit asset declines, with mutual funds falling 13.6% and ETFs declining 12.4% in March. Net flows out of the vehicles totaled $335.2 billion, or 2.2% of February month-end assets.

- The decline in ETF assets was softened by the fact that investors held steady on a net basis, adding $9.3 billion in positive flows into the vehicle during March. Fixed-income ETFs struggled in March, suffering $20.7 billion in net negative flows. Alternative ETFs gathered significant flows YTD, especially relative to the small size of the category ($46 billion).

- Money market funds received net flows of $684.7 billion, raising assets 19% to $4.3 trillion. Taxable money market funds added $823.5 billion, while tax-free and prime bled $3.0 billion and $135.9 billion, respectively. The discrepancy in flows highlights investor demand for safety of government-backed securities.

- Despite a few bright spots for alternatives, Cerulli said the performance of key liquid alternatives categories in 1Q 2020 as well their long-term performance relative to stock and bond funds make them “a tough pitch.” One bright spot has been managed futures funds, which, after a long period of poor returns, were flat in 1Q 2020. Managed futures showed the lowest five-year correlation to equity markets.

Average tax-deferred retirement balance down 19% in Q1 2020: Fidelity

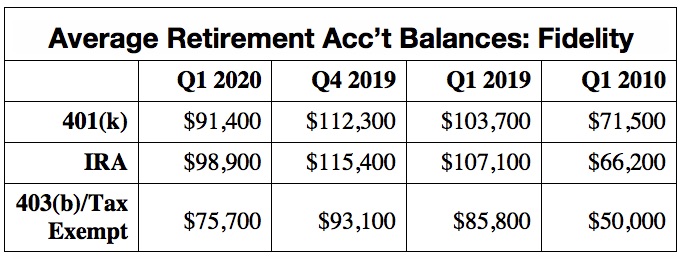

The major market downturn in March caused average 401(k), IRA and 403(b) balances to drop substantially across Fidelity Investments’ more than 30 million IRA, 401(k) and 403(b) accounts in the first quarter of 2020, according to an analysis by the Boston-based retirement giant.

The average 401(k) balance was $91,400, down 19% from the record high of $112,300 in Q4 2019. The average IRA balance was $98,900, a 14% decrease from last quarter. The average 403(b)/tax-exempt account balance was $75,700, down 19% from last quarter. (Note: Median account values, not provided, are typically substantially lower than average account values.)

Despite those setbacks, contributions to retirement accounts persisted, according to Fidelity. The average 401(k) contribution rate was 8.9% in the first quarter, consistent with Q4 2019; 15% of 401(k) participants increased their contribution rate in the quarter. The analysis also showed:

- The average employer contribution was 4.7%, up from 4.6% in the previous quarter and equal to 4.7% in Q1 2019.

- The average contribution to an IRA in Q1 2020 grew to $3,330, up 10% from the average in Q1 2019.

- Contributions to 403(b)/tax exempt account increased to 6.9%, up from 5.6% in Q4 2019 and 5.4% a year ago.

- The number of newly opened IRAs reached a record 407,000 in Q1 2020, up 36% over Q1 2019.

- The number of Millennials contributing to IRAs increased 41% over last year, while the amount contributed by Millennials increased 64%.

- Among female Millennials, the number of IRAs increased 20% from Q1 2019.

- The number of Roth IRAs among Millennials increased 41% over the last year, with the amount of Roth IRA contributions growing 64%.

- Only 7.3% of individuals changed their 401(k) allocation, up from 5.2% in Q4 2019.

- Of savers who made a change, 60% made only one change in the quarter.

- Among Baby Boomers, 9.9% changed their 401(k) allocation, with most moving their savings into a conservative investment option.

- Among those with 403(b)/tax-exempt accounts, 5.2% changed their allocation, up from 4.1% last quarter.

- Only 3% of participants in Fidelity’s 401(k) and 403(b)/tax-exempt platform dropped their allocation to 0% equities.

- Hardship withdrawals increased slightly, but new 401(k) loans dropped. Before the CARES Act passed in late March, only 1.4% of individuals took a hardship withdrawal from their 401(k) in Q1 2020, less than half a percentage point more than the 0.9% in Q1 2019.

- Only 2.3% of 401(k) participants initiated a loan in Q1, down from the 2.6% in Q4 2019 and even with 2.3% in Q1 2019. Individuals did not draw significant funds from their retirement accounts in the first quarter.

Average daily customer calls from Fidelity’s retail and workplace investors increased 20% in Q1 2020 versus Q1 2019, and Fidelity’s new COVID-19 resource centers received nearly one million views through the end of the quarter.

Lincoln Financial waives retirement plan withdrawal, loan fees

Lincoln Financial Group is taking steps to support customers experiencing COVID-19-related financial challenges, including relief for retirement savers, flexibility for policyholders, and support for the community and business.

In support of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), Lincoln Financial is waiving eligible withdrawal and loan initiation fees. Lincoln’s team of retirement consultants are providing one-on-one support by phone or online.

Additionally, Lincoln is sharing educational materials and hosting webinars to help plan participants decide whether a loan or withdrawal is the right option for them and understand how it might affect their long-term goals.

Kevin Kennedy named CMO at Pacific Life Retirement Solutions

Kevin Kennedy has been named senior vice president, sales and chief marketing officer of Pacific Life’s Retirement Solutions Division, which had more than $14 billion in 2019 sales of fixed and variable annuities, structured settlements, and retirement plan annuities.

Kennedy will oversee the division’s sales and marketing organization with oversight for sales execution and analytics, strategic partner and asset manager relationships, structured settlements, and expansion into the registered investment advisor (RIA) market.

Before joining Pacific Life, he was managing director and head of individual retirement at AXA Equitable Holdings, where he was in charge of product design and pricing, business strategy, and distribution of the individual retirement product line.

© 2020 RIJ Publishing LLC. All rights reserved.