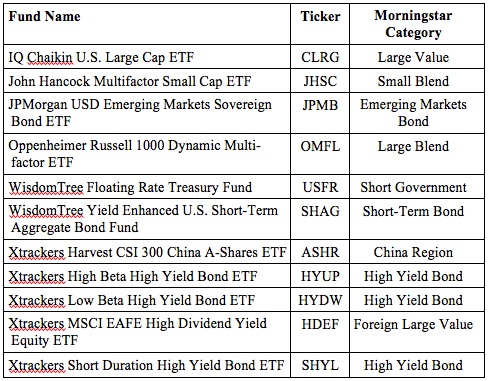

Schwab adds 11 new options to its ETF OneSource marketplace

Charles Schwab’s ETF OneSource platform has added 11 additional ETFs to its offerings, effective July 3. The commission-free online ETF exchange, which has no enrollment requirements or early redemption fees, now offers 265 ETFs from 15 providers across 70 Morningstar Categories.

“Our 2018 ETF Investor Study showed that 64% of investors say that the ability to trade ETFs without commissions is important to them, and 54% of Millennial investors agree,” said Heather Fischer, vice president of ETF and mutual fund platforms at Schwab, in a release.

The 11 new ETFs cover domestic equities, fixed income and international equities. Six of the additions fall into the taxable bond category. The funds added to Schwab ETF OneSource on July 3 include:

Millennials reap benefits of Pension Protection Act: Empower

A new survey from Empower Institute, the thought-leadership arm of Empower Retirement, suggests that the savings levels of Millennials show that they are benefiting from specific innovations in retirement plan design over the last decade.

(The tripling of the value of the stock market since 2009, itself a by-product of Federal Reserve largesse in response to the Great Recession, may also have helped Millennials’ accumulation levels relative to earlier cohorts. Time will tell.)

Americans born after 1981, aka Millennials, are on track to replace 75% of their current income in retirement, according to the survey of 4,000 working Americans ages 18 to 65 who are saving for retirement in any defined contribution workplace plan.

Generation X workers are on track to replace only 61% and Baby Boomers are on track to replace a mere 58%, the survey showed. “Millennials are the first generation to fully benefit from improvements made to retirement plans over the last decade and it shows now in their retirement savings habits and attitudes,” an Empower release said.

Empower attributed the improvements in retirement readiness to innovations made possible by the Pension Protection Act of 2006: Automatic enrollment, automatic escalation of contributions and acknowledgement of the significance of employer matches to employee accounts.

Of Millennials responding to the Empower Institute survey, 41% are automatically enrolled in a DC plan, compared to 38% percent of Gen Xers and 33% percent of Baby Boomers. Additionally, 38% of Millennials are enrolled in a plan with auto escalation features.

The survey results include a Retirement Progress Score (RPS), which is a numeric estimation of the percentage of working income that American households are on track to replace in retirement. The median replacement rate among survey participants is 64%, meaning that half of respondents are on track to replace more than 64% of their current income and half are on track to replace less than 64%.

Some key findings:

- 24% of Millennials who responded to the survey say they have a formal retirement plan, compared with 19% of Gen X respondents and 17% of Baby Boomers.

- Fewer Millennials than Gen Xers and Baby Boomers believe they will have to work at least part time in retirement: 48% of Boomers believe they will need to work at least part time in retirement, compared to 44% of Gen Xers and 40% of Millennials.

- Millennials less confident than older generations about Social Security as a retirement income: 59% of Millennials expect Social Security to be a source of income in retirement, compared to 88% of Boomers and 73% of Gen Xers.

- 61% of Millennials expect defined contribution plans, such as 401(k)s, to be a source of income in retirement, compared to 55% of Gen Xers and 47% of Boomers.

The Empower Institute survey findings are available in a white paper called “Scoring the Progress of Retirement Savers.” The research was conducted by Brightwork Partners LLC for the Empower Institute.

Hueler introduces stable value fund evaluation tool

Hueler Analytics has launched Stable Value Compass, a new online due diligence tool designed for discerning fiduciary advisors. The new tool combines Hueler’s stable value data with technology for analysis and client ready reporting.

Stable Value Compass will allow fiduciaries, advisors, and consultants the capability to compare multiple pooled funds and insurance company sponsored products across key standardized data elements, a Hueler release said.

Hueler Analytics provides broad market coverage of stable value alternatives including stable value pooled funds, insurance company separate accounts, and general account products.

MassMutual to offer T. Rowe Price target date funds

MassMutual will offer a series of Select T. Rowe Price Target Date Funds target date to its retirement plan customers, according to a release from the mutual insurer. The TDF series features active management and dynamic tactical asset allocation. The funds are available only in plans where MassMutual is the recordkeeper.

The “MassMutual Select T. Rowe Price Retirement Funds” are designed to address certain risks, including inflation, longevity, and market risks, which retirement savers face during their accumulation years and through retirement, a MassMutual release said.

Recent research by MassMutual indicates that many retirees and pre-retirees continue to favor active management as an investment strategy. Nearly half (47% of pre-retirees; 49% of retirees) say they have assets invested in actively managed mutual funds, according to the MassMutual Retirement Savings Risk Study. In addition, 80% of pre-retirees and 71% of retirees find active management appealing as an investment strategy.

However, some retirees and pre-retirees may be taking too much risk with their retirement savings. Eighty-eight percent of retirees and 73% of pre-retirees who rely on a financial advisor report that their advisor has recommended they invest more or somewhat more conservatively than they currently do, the MassMutual study reports.

Many expect to work in retirement: Prudential

Uncertain about Social Security and their own financial preparedness, more than half of future retirees expect to work during retirement, according to a new study from PGIM Investments, which manufactures and distributes funds for PGIM, Inc., Prudential Financial’s global investment management business.

The study, the 2018 Retirement Preparedness Study: A Generational Challenge, conducted by The Harris Poll for PGIM Investments, found that while only 6% of today’s retirees work, 52% of pre-retiree Baby Boomers, 58% of pre-retiree Gen Xers, and 43% of pre-retiree Millennials expect to work full- or part-time in retirement.

These expectations may be linked to pre-retirees’ decreased confidence about Social Security. Only 51% of Millennials expect to receive these benefits at all.

According to the study:

- Pre-retirees are more likely to base their decision about when to retire on their wealth rather than their age. Half of Gen Xers and 62% of Millennials say they will retire when they have saved enough money. Current retirees decided when to retire largely based on their age and eligibility for Social Security and pensions.

- Millennials are more likely to plan to start a business in retirement (20%) than Gen Xers (9%) or Boomers (4%). Nearly four in 10 pre-retirees (39%) say they want to volunteer after they retire.

- More than half (51%) of current retirees say they’re “living the dream.” On average, these individuals started saving six years earlier than other retirees. Compared with those who aren’t living their dream retirement, these individuals are more likely to have pensions and diversified sources of income. They also are more likely to have been able to retire at their planned retirement age.

- More than half (53%) of pre-retirees are unsure how much they need for retirement. Gen Xers have the highest estimates of the savings they need, but almost 20% aren’t saving for retirement at all.

- Fifty-one percent of retirees say they retired earlier than expected. Of that group, half say they retired more than five years earlier than planned because of health problems (29% of the early retirees), layoffs or restructurings (14%), the need to care for a loved one (13%), or the inability to find a new job (10%).

To address growing consumer need for retirement income planning, Prudential Financial, along with 23 other leading financial services organizations, established the Alliance for Lifetime Income to help educate Americans about the value of having protected income in retirement.

Asians spend 11 fewer years saving for retirement: LIMRA

In the U.S., the average age for consumers to start saving for retirement is 35 and Americans on average expect to retire at 66. But in Asia, saving starts at age 40 on average and the expected retirement age is 60, according to a new report from the LIMRA Secure Retirement Institute.

Despite the shortened time to save for retirement, more consumers in Asia are confident they will be able to live the retirement lifestyle they want.

Consumers in Asia are more likely to be confident about maintaining their desired lifestyle in retirement than consumers in the US, according to the report. While only half of Americans expressed confidence about retirement, 69% of Asians did.

Similarly, 31% of consumers in Asia are not concerned about outliving their retirement assets, compared to 24% of US consumers, according to LIMRA SRI. But a larger fraction of US consumers has determined their expected health care costs in retirement (40% vs. 34%).

According to the study, 47% of consumers in Asia and 43% in the US have calculated the assets they will have in retirement, and 39% of Asian consumers have estimated how long those assets will last, versus 34% of Asian. More than half of consumers in both regions have not done basic retirement planning.

© 2018 RIJ Publishing LLC. All rights reserved.