Sales of fixed indexed annuities (FIAs) and registered index-linked annuities (RILAs) combined for 45% of near-record U.S. annuity sales in the third quarter of 2024, according to the LIMRA U.S. Individual Annuity Sales Survey.

At $114.7 billion, third-quarter annuity sales were up 30% from the same quarter in 2023, according to the survey, which represents 92% of the total U.S. annuity market. Annuity sales reached $332 billion in the first nine months of 2024, up 23% year-over-year.

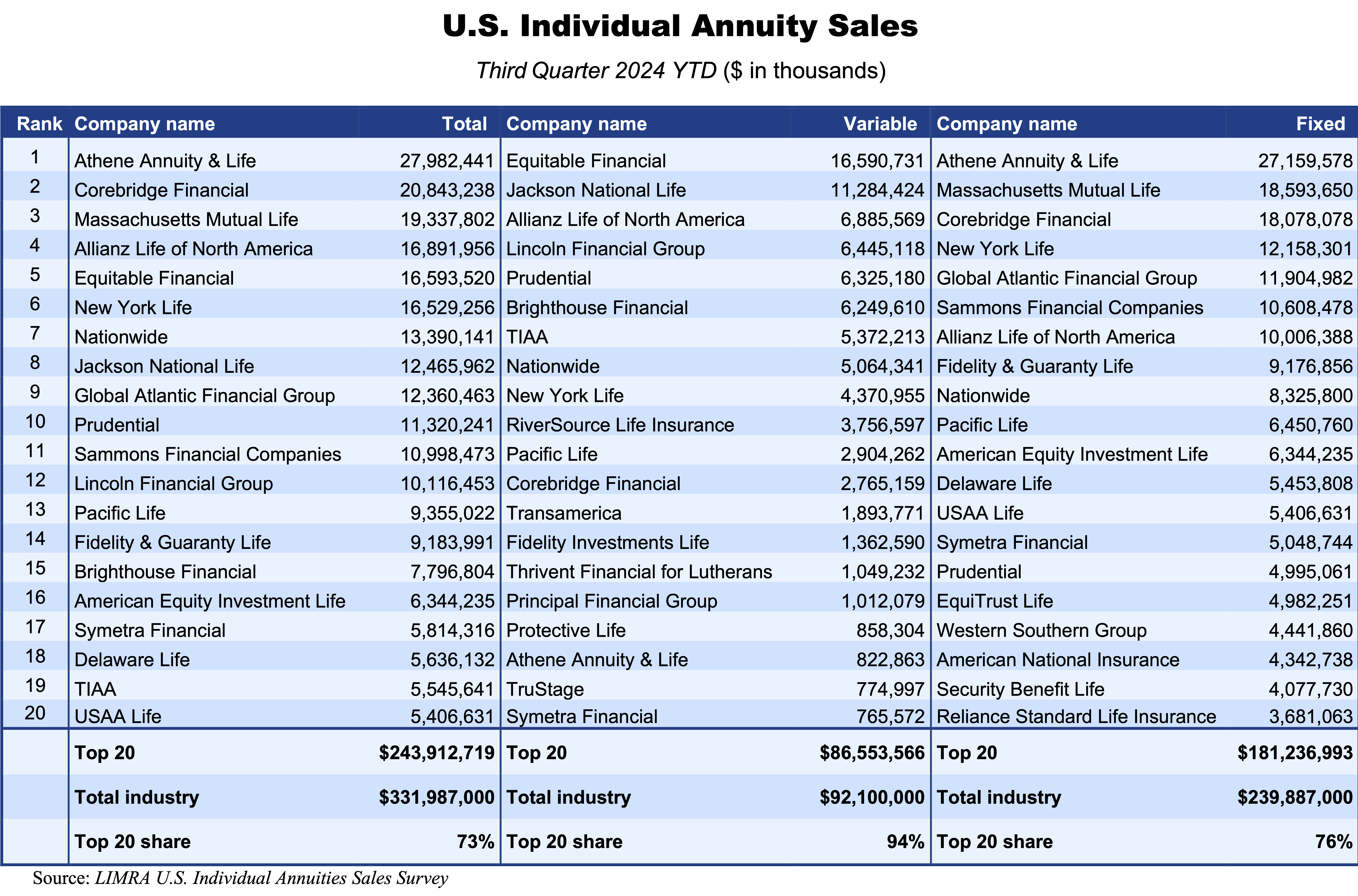

The overall sales leader was Athene Annuity & Life, with sales of $27.98 billion, followed by Corebridge, MassMutual, Allianz Life of U.S. and Equitable. Athene led in fixed annuities (including both fixed indexed and fixed rate contracts) while Equitable led in variable annuities (traditional and RILA).

New York Life was the leader in sales of payout annuities (single premium immediate annuities and deferred income annuities). With combined FIA and RILA sales of about $16.9 billion, Allianz Life was the overall leader in index-linked annuities.

“All product lines posted double-digit increases, and overall sales were less than 1% lower than the record-high sales set in fourth quarter 2023,” said Bryan Hodgens, senior vice president and head of LIMRA research, in a release.

“While interest rates have declined, heightened market uncertainty will likely continue to draw investors seeking principal protection and guaranteed growth. LIMRA expects annuity sales to set a new record in 2024.”

Different types of life/annuity dominate different segments of the annuity market, depending on their business models. Mutual life insurance companies are supreme in payout annuities. The former sellers of traditional VAs now rule the roost in RILAs. Private equity-led (PE) annuity issuers reign in the FIA space. This rule has exceptions, however. Mutuals and PE companies both are leaders in fixed rate deferred annuity sales. MassMutual, a mutual life insurer, has had strong FIA sales since acquiring Great American in 2021.

Fixed indexed annuities

At $35.2 billion, FIA sales set a new record the third consecutive quarter, up 56% from 3Q2023. Year-to-date (YTD) FIA sales increased 34% to $95.1 billion. “Strong equity market performance and a desire for principal protection continue to attract investor interest in FIA products,” said Hodgens. “To remain competitive, carriers are refining their indices and introducing more lucrative crediting options.”

The top-five issuers were Athene, Allianz Life, Sammons Financial Companies (including Midland National Life and North American Company for Life and Health Insurance), Corebridge Financial and American Equity Investment Life. [Note: High sales commissions are a perennial driver of FIA sales. Long-dated FIA liabilities are also the primary raw material of the “Bermuda Triangle” strategy, as described in RIJ reporting since 2020.]

Registered index-linked annuities

At $17 billion, RILAs enjoyed record sales for the sixth consecutive quarter, up 35% from the prior year. In the first nine months of 2024, RILA sales were $47.9 billion, up 39% from 2023.

“In the first nine months of 2024, RILA sales surpassed the total RILA sales collected in 2023 ($47.9 billion vs. $47.4 billion), Hodgens said. “LIMRA expects RILA sales to remain strong through 2025.” The top-five RILA issuers were Equitable, Allianz Life, Prudential, Brighthouse Financial and Jackson National Life.

Fixed-rate deferred annuities

Fixed-rate deferred (FRD) annuity sales were $40.3 billion in the third quarter, up 17% from 3Q2023. In the first nine months of 2024, FRD sales totaled $124 billion, up 17% from the prior year. The top-five issuers were Athene, MassMutual, Corebridge Financial, New York Life and Global Atlantic Financial.

“Our October preliminary figures suggest sales are beginning to soften in the face of repeated interest rate cuts (in September and November),” the release said. “That said, FRD contracts still offer higher yields when compared with other short-term investments. If market volatility increases, LIMRA expects increased demand for FRDs with clients seeking principal protection.”

Payout annuities

Single premium immediate annuity (SPIA) sales were $3.5 billion in the third quarter, up 20% from the prior year. In the first nine months of 2024, SPIA sales rose 8% to $10.5 billion.

Third-quarter deferred income annuity (DIA) sales were $1.3 billion, up 41% jump from 3Q2023. In the first nine months of the year, DIA sales grew 33% to $3.8 billion.

The top-five issuers of payout annuities were New York Life, MetLife, USAA Life, Pacific Life, and MassMutual.

Traditional variable annuities

Traditional VA sales were $15.1 billion in 3Q2024, up 16% from 3Q2023. It was the third consecutive quarter of year-over-year growth for VAs. For the first nine months of 2024, traditional VA sales totaled $44.2 billion, up 13% gain YoY. The top five issuers were Jackson National Life, Equitable, TIAA (group annuities), Nationwide, and Lincoln Financial.

For more details on the sales results, go to Annuity Estimates (2024 Third Quarter) in LIMRA’s Fact Tank.

- To view the top 20 rankings of total, variable and fixed annuity writers in the third quarter of 2024, see U.S. Individual Annuity Sales (2024 Third Quarter Results).

- To view the top 20 rankings of traditional VA and RILA sales leaders in the third quarter of 2024, visit U.S. Individual Variable Annuity Sales (2024 Third Quarter VA Breakout Results).

- For the top 20 rankings of fixed-rate deferred, fixed indexed and payout annuity writers in the third quarter of 2024, visit U.S. Individual Fixed Annuity Sales (2024 Third Quarter Fixed Breakout Results).

- © 2024 RIJ Publishing LLC.