I staked out a position on yield curve control in Bloomberg Opinion:

The Federal Reserve might not be ready to explicitly target yields on U.S. Treasury securities to keep them from rising and hindering the economic recovery, but that doesn’t mean it won’t happen. If you believe the Fed will be under continued pressure to do more to support the economy, it’s tough to bet against the eventual adoption of so-called yield-curve control.

Recall that last week, the Fed signaled doubts about yield curve control. My expectation is that those doubts will eventually fade.

How do I arrive at such a conclusion despite the Fed’s reticence? My position assumes continued economic weakness, inflation persistently below target, and an eventual unwillingness on the part of the Fed to continuously ramp up the scale of asset purchases.

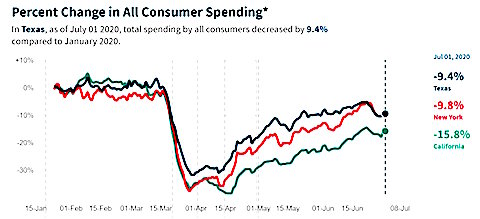

With a new wave of Covid-19 cases sweeping some states, particularly in the South and West, it is becoming increasingly evident that we will not experience anything like a V-shaped recovery. We are in this for the long haul; consumers are already starting to step back:

From a July 8, 2020 Tweet by Julie Coronado, Ph.D.

We have to assume that even in the case of a miracle vaccine, full recovery remains years away. If the last recovery is any example, inflation will remain persistently below the Fed’s 2% target. With that being the case, the Fed will be under constant pressure to DO MORE.

What does “doing more” entail? First up will be enhanced forward guidance. They will tie policy to economic conditions, likely weighted more toward realized inflation. Beyond that, they will want to move onto a tool they can escalate. They could escalate quantitative easing, but that commits them to a path of expanding the balance sheet at an increasing pace. Doing more with quantitative easing means $45 billion becomes $60 billion becomes $75 billion, etc. You get the idea. I think the Fed would eventually become concerned about the optics.

Alternatively, you could instead move toward yield curve control. The Australian experience is that once you establish credibility on the policy, you don’t need to actually buy any bonds. Plus, you don’t have to jump straight to three years out. You start at one year, then two years, then three years. That’s like a full year of “doing more” without escalating the pace of asset purchases.

You can argue whether this actually accomplishes anything. That’s fine, you don’t think the signaling alone has much value. Others think it does. Either way, you have an investment position. Note also that a turn toward yield curve control doesn’t necessarily preclude the Fed from doing more quantitative easing. I expect they would use the tools in tandem, yield curve control to lock down the front end and enhance forward guidance and asset purchases to reduce term premiums and force investors into less safe assets.

Of course, a surprisingly quick recovery or an outbreak of inflation would eliminate the need for additional policy. For example, Congress could in theory pump enough money into the economy to accelerate the return to full employment. It’s not my expectation, but it could happen and shift the path of Fed policy.

Bottom Line: Yield curve curve control seems too obvious a choice to easily dismiss.

© 2020 Tim Duy. Used by permission. This column first appeared on his blog.