| Percent of U.S. Tax Units With No Income Tax Liability, 2009 |

|||||

|---|---|---|---|---|---|

| Income* | Single | Jt. Filers |

Elderly | w/ Chdrn |

All Units |

| <$10K | 99.9 | 100 | 100 | 99.9 | 99.8 |

| $10-20K | 74.3 | 99.9 | 89.5 | 99.8 | 83.6 |

| $20-30K | 36.7 | 90.2 | 76.5 | 98.9 | 61.8 |

| $30-40K | 16 | 79.8 | 61.4 | 89.3 | 47.5 |

| $40-50K | 7.4 | 71.7 | 48.2 | 68.3 | 35.7 |

| $50-75K | 5 | 34.2 | 22.5 | 40.9 | 21.5 |

| $75-100K | 3.6 | 11.3 | 8.1 | 15.1 | 9.2 |

| $100-200K | 4 | 3.4 | 4.9 | 4 | 4.5 |

| $200-500K | 3 | 1.8 | 3.9 | 1.6 | 2 |

| $500K-1M | 2.6 | 1.8 | 1.6 | 2.1 | 2 |

| >$1MM | 2 | 1.5 | 1.1 | 1.3 | 1.5 |

| All | 46.7 | 38.1 | 55.3 | 54.1 | 46.9 |

| *Cash income is Adjusted Gross Income minus taxable state and local tax refunds, plus total deductions from AGI. Source: Urban-Brookings Tax Policy Center, 2009 |

|||||

Archives: Articles

IssueM Articles

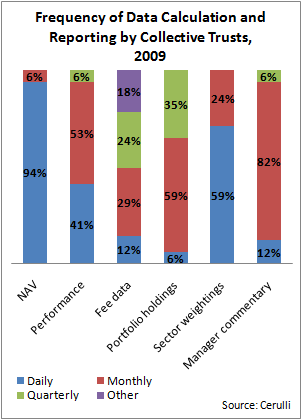

Two Trends in One: CTFs and TDFs

It’s too soon to say if, when or how it will affect the way Americans save for retirement, but the trend is undeniable: asset managers are creating target-date collective trust funds at a rapid rate and pitching them to 401(k) plan sponsors.

“They still have issues, but they’re gaining traction,” said one 401(k) platform provider who asked not to be identified. His firm offers a range of exchange-traded funds, CTFs, and mutual funds to plan sponsors.

Of the 159 collective trust funds (CTFs) that were launched in 2009, 115 (72%) were formed as vehicles for lifecycle or target date investing strategies. From 2007 to 2009, 439 CTFs were formed, of which 241 (55%) were target date CTFs.

Both collective trusts and target date funds—especially TDFs—were handed a ready-made market when they were approved as QDIAs (qualified default investment alternatives) for 401(k) plans by the Pension Protection Act of 2006.

| Top-20 US Collective Trust Fund Managers and Total Assets, 2Q 2009 ($ billions) |

|||

|---|---|---|---|

| Rank | Firm | 2Q 2009 Assets | Q 2009 Marketshare |

| 1 | BlackRock1 | $388.2 | 37.8% |

| 2 | State Street Global Advisors Ltd. | $123.4 | 12.0% |

| 3 | Northern Trust Global Investment Services | $118.9 | 11.6% |

| 4 | BNY Mellon | $110.6 | 10.8% |

| 5 | Fidelity Investments | $65.0 | 6.3% |

| 6 | Invesco National Trust Co. | $40.8 | 4.0% |

| 7 | Old Mutual Asset Management Trust Co. | $26.2 | 2.5% |

| 8 | Galliard Capital Management Inc. | $17.8 | 1.7% |

| 9 | The Vanguard Group, Inc. | $13.1 | 1.3% |

| 10 | UBS Realty Investors LLC | $10.3 | 1.0% |

| 11 | Capital Guardian Trust Company | $10.0 | 1.0% |

| 12 | Ameriprise Trust Company | $9.5 | 0.9% |

| 13 | Wilmington Trust RISC | $6.3 | 0.6% |

| 14 | Schroders Investment Mgt North America | $5.6 | 0.5% |

| 15 | Amalgamated Bank | $4.8 | 0.5% |

| 16 | Fortis Investments USA, Inc. | $4.4 | 0.4% |

| 17 | Genesis Asset Managers, LLP | $4.4 | 0.4% |

| 18 | Morley Financial | $4.0 | 0.4% |

| 19 | Prudential Private Placement Investor, L.P. | $3.5 | 0.3% |

| 20 | AFL-CIO Housing Investment Trust | $3.6 | 0.3% |

| Total CTF market | $1,027.7 | ||

| 1Formerly Barclays Global Investors NA | |||

| Sources: Morningstar Direct, Cerulli Associates | |||

Leading the charge

The largest CTF provider is BlackRock, which has a 38% market share, according to Cerulli Associates. Just four firms, BlackRock (formerly Barclays Global Investors), State Street Global Advisors, Northern Trust, and BNY Mellon, account for 72% of the $1 trillion-plus CTF business in the U.S.

“It’s my understanding that the bigger firms are leading the charge into target-date CTFs,” said Jake Hartnett, senior analyst, Institutional Asset Management, at Cerulli Associates. “Pyramis, Fidelity’s institutional money manager, has come out with them. BlackRock also has a TDF-CTF product.”

“We have cloned a Freedom Fund collective trust,” said Beth McHugh, a Fidelity vice president, referring to Fidelity’s proprietary line of target date funds. “They’re fairly recent and they’re not available to everyone. We also have other multi-fund collective trusts.”

“The trend has been shared among various providers,” said Steve Deutsch, who tracks CTFs for Morningstar, Inc. “BlackRock, Putnam and Nuveen are there, but also smaller firms like Avatar Associates and Manning & Napier. Since CTFs are unregistered, you’ll see a mix of established firms as well as boutiques and smaller firms that can’t afford to go through the cost and time of registration.”

According to Cerulli, CTF assets peaked at $1.43 trillion in 2007 after five years of steady growth. The “flight to quality” in 2008 and 2009 cut their assets to $1.07 trillion in 2008 and $1.03 trillion last year. Of that trillion, about 28% is in DC plans and 72% in DB plans. Morningstar estimates the CTF total at about $1.6 trillion, with about half in DB and half in DC.

That’s still only a fraction of the $13.4 trillion that Americans hold in retirement accounts, in the form of mutual funds, exchange traded funds, variable annuity separate accounts, and individual stocks, as well as CTFs.

Made for each other

Because CTFs are marketed only to institutions, and not to the public as mutual funds are, they do not need to submit a prospectus to the Securities and Exchange Commission for approval and provide one to every potential investor. They are supervised by banking regulators rather than by the SEC.

Advertisement

But TDF-CTFs aren’t merely wholesale, bank-regulated versions of target-date mutual funds.

“We have compared target date mutual funds and TDF-CTFs from same firm,” Deutsch said. “While they may have the same name and the same target date in their objective or strategy, you’ll get completely different money managers running them, different investment decision processes, different allocations and different return streams. They’re not just low-cost clones of mutual funds.”

Cerulli’s Hartnett thinks the CTF structure will actually enhance the target date strategy, because it will make it easier than ever for target date fund managers to hold alternative assets as they seek more sophisticated, institutional-style diversification.

“The target date format and the CTF structure are made for each other,” he said. “Part of the TDF solution, which even in the mutual fund format includes getting exposure to non-correlated assets, is to bring a more institutional level of management to DC plans.”

Presenting the target-date investment strategy in a CTF wrapper will also relieve some of the fiduciary burden from plan sponsors, Hartnett said. By statute, the trustees of CTFs have fiduciary responsibilities that mutual fund managers do not. They can relieve that burden from plan sponsors, or at least share it.

“Because [CTFs] are bank-registered products, you have an external fiduciary joining the plan sponsor,” he added. “Plan sponsors like that. If the asset manager is using a ‘40 Act’ [i.e., Securities Act of 1940] mutual fund format, there’s no co-fiduciary. From what we’ve heard, that makes the CTF an easier sell. We’ve also heard that Taft-Hartley plans [multi- employer union-sponsored DC plans] are more comfortable with CTFs.”

“Because [CTFs] are bank-registered products, you have an external fiduciary joining the plan sponsor,” he added. “Plan sponsors like that. If the asset manager is using a ‘40 Act’ [i.e., Securities Act of 1940] mutual fund format, there’s no co-fiduciary. From what we’ve heard, that makes the CTF an easier sell. We’ve also heard that Taft-Hartley plans [multi- employer union-sponsored DC plans] are more comfortable with CTFs.”

The percentage of defined contribution plans offering mutual funds declined to 54% from 65% over the six-year period from 2003 to 2008, according to Morningstar. Meanwhile, a higher percentage of plans are using institutional mutual funds (to 80% of plans from 72%), of collective trusts (to 45% from 32%) and separate accounts (to 29% from 24%).

Ironically, CTFs were the investment structure of choice in defined contribution plans during the early days of the 401(k) phenomenon—a holdover from DB practices.

But as the mutual fund business grew, mutual funds supplanted CTFs in DC plans. Mutual funds, which were built for the retail market, have traditionally been more transparent than CTFs in terms of offering prospectuses and daily valuations. But they are more expensive.

Back to the future

Now the pendulum has swung the other way. Precisely because they don’t market to the general public and don’t have to meet a heavy regulatory burden, CTFs operate more cheaply than mutual funds—especially actively managed funds.

In response to consumer and government pressure to cut plan costs, plan sponsors have become increasingly receptive to a variety of low-cost alternatives, including index funds, institutional mutual funds, exchange traded funds, separate accounts, and CTFs.

“Collective trusts, separately managed accounts and institutionally priced mutual funds all have advantages,” said David Wray, president of the Profit Sharing Council of America, an organization of large 401(k) plan sponsors. “There is no single right answer.”

The positioning of target date funds in collective trusts won’t necessarily resolve certain problematic aspects of target-date funds, however. The problems, which were reviewed in Senate hearings last year, include the wide variation in TDF design and the difficulty that investors have in benchmarking TDF performance.

The hearings also revealed that many investors believed that by investing in target date funds, they would reach retirement with adequate savings and that the volatility of their savings would taper off by retirement.

In fact, until they experienced steep losses in 2008, many TDF investors had no idea that so much of their money was at risk. The very fact that TDFs were dated created a false impression that they would protect investors from the market risk associated with an ill-timed retirement.

When packaged inside CTFs, which are less transparent than mutual funds, TDFs are not likely to be any more understandable to the average plan participant than they were before. Whether there’s the seed of a crisis in the wedding of these two strategies remains to be seen.

© 2010 RIJ Publishing. All rights reserved.

My Life as a ‘Dangerous Woman’

When I tell people at parties that I’m a professor of economics who specializes in pension policy, I get a lot of yawns and sidelong glances. I don’t mind—retirement policy is important, but it does tend to be complex.

So imagine my surprise when I saw a Google Alert linking these two word strings: “Teresa Ghilarducci” and “the most dangerous woman in America.” (Not, for instance, Angelina Jolie?)

How did I gain such notoriety? When the banks were bailed out in 2008, I testified before Congress, calling for government to help regular people, not just banks. Absorb the collapsing 401(k) assets on a volunteer basis, I recommended, and replace the assets with safe ones.

Maybe I should have stopped there. But I didn’t. I said 401(k)s were failures and that tax breaks for saving money should go only to the people who need them most, with the government guaranteeing a safe return on savings.

But despite what I thought was a modest proposal, some people heard me—or deliberately misinterpreted me—saying that I wanted the government to take over 401(k)s. And these people weren’t just casual listeners. They were active conservatives, including the Big Enchilada himself—Rush Limbaugh.

Oh, well. No publicity is bad publicity, right?

Wrong. Limbaugh attacked me three times, calling me “communist babe,” among other endearments. Lots of people listen to Rush, it turns out. The exaggerated story soon went viral, to Fox News, the Wall Street Journal editorial page, and to a dizzying array of right-wing bloggers, some of them very angry. You’d be surprised how many there are. I sure was.

Advertisement

The story even reached John McCain, who in the last weeks of the Presidential campaign accused Democrats of wanting to confiscate 401(k)s. If I were a horse, a friend told me, I’d have won the trifecta.

Of course, they shoot horses, don’t they?

Things got pretty scary for a time. My employer, the New School, became alarmed at the screaming voicemail death threats and ominous threatening emails. The university’s security chief gave me his cell phone number. I won’t reveal his last name, but Steve is big and alert. He made me feel secure.

But then support poured in. Justin Fox of Time magazine said the attacks on me were unfair. I wasn’t killing 401(k) plans, he wrote; Wall Street was doing a perfectly good job of that on its own. The New York Times Magazine called my suggestion one of the best ideas of 2008. US News and World report ran a nice article about me. (My glossy photo was soft-focused, with a flower in the background.)

Parade Magazine, which has tens of millions of readers, wrote favorably about my plan in its Intelligence Report section. And the Annenberg Center’s Political Fact Check debunked the false accusations about my alleged “socialist” and “theft” motives. (It’s still on the web if you care to see it.)

So what’s it like to be ‘the most dangerous woman in America?’ I’m working hard on my Rockefeller Foundation grant to promote real pension reform. And I’m still promoting my message—as recently as a few weeks ago, on Larry Kudlow’s CNBC show. Because we still need secure pensions for all Americans.

Citations (Because I’m an academic.)

Ghilarducci, Teresa. “Saving Retirement in the Face of America’s Credit Crises: Short Term and Long Term Solutions,” Committee on Education and Labor, The Impact of the Financial Crisis on Workers’ Retirement Security 1:00, 2181 Rayburn House Office Building. Oral Testimony. Tuesday October 7, 2008.

<http://edlabor.house.gov/testimony/2008-10-07-TeresaGhilarducci.pdf>

Limbaugh, Rush. “Biden: CEO Pensions “Go First” (And Your 401(k) Will Go Next),” Rush 24/7, aired on October 24, 2008.

<http://www.rushlimbaugh.com/home/daily/site_102408/content/01125109.guest.html>

Fox, Justin. “Should the 401k Be Killed?” Time Magazine. Dec. 04, 2008.

<http://www.time.com/time/business/article/0,8599,1864139,00.html>

Mihm, Stephen. “8th Annual Year In Ideas: The Guaranteed Retirement Account,” The New York Times. December 12, 2008.

<http://www.nytimes.com/2008/12/14/magazine/14Ideas-Section2-C-t-001.html>

Brandon, Emily. “Teresa Ghilarducci: The 401(k) Retirement System Has Failed,” U.S. News & World Report. January 30, 2009.

<http://www.usnews.com/money/blogs/planning-to-retire/2009/01/30/teresa-ghilarducci-the-401k-retirement-system-has-failed>

Winik, Lyric Wallwork. “Rethinking Retirement,” Parade Magazine. April 26, 2009.

<http://www.parade.com/news/intelligence-report/archive/rethinking-retirement.html>

FactCheck.Org. November 19, 2008.

<http://www.factcheck.org/askfactcheck/are_congressional_democrats_talking_about

_confiscating_ira.html>

© 2010 RIJ Publishing. All rights reserved.

Turning Home Equity into Lifetime Income

Home equity is destined to become an important source of funds for retirement, and the reverse mortgage is a product designed for this purpose. In this article, I’ll evaluate the reverse mortgage as a product for generating lifetime income, either directly or in combination with an immediate annuity.

The Need to Use Home Equity

For many older Americans, the equity in their home is their largest asset. Data from the Federal Reserve’s Survey of Consumer Finances shows that for individuals over the age of 65, home equity averages about 2 ½ times the amount of financial assets.

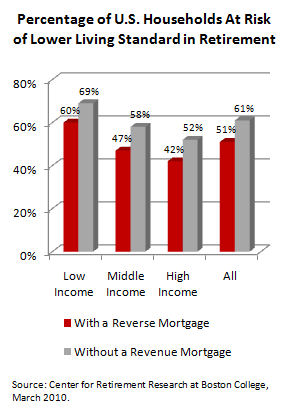

The Center for Retirement Research at Boston College has estimated that without tapping home equity, 61% of Americans are at risk of not being able to maintain their standard of living in retirement, and the trend is worsening. In a recent study they conclude:

“Not tapping home equity may be a luxury that future retirees can ill afford as Social Security replaces a smaller share of pre-retirement incomes and people rely increasingly on meager 401(k) balances rather than on traditional pensions.”

Retirees can generate funds from home equity by downsizing, or by borrowing against their home’s equity value. The reverse mortgage is a product specifically designed for retirees who wish to stay in their home and have access to its equity.

Retirees can generate funds from home equity by downsizing, or by borrowing against their home’s equity value. The reverse mortgage is a product specifically designed for retirees who wish to stay in their home and have access to its equity.

So far, reserve mortgages have been used by only about 2% of eligible homeowners. They have generated quite a bit of press coverage—some positive because the product meets a growing need, and some negative because of the high fees.

Product Design

Reverse mortgage lenders offer a number of different ways to utilize home equity. Homeowners may take the loan in any of the following forms: as a lump sum advance, as a credit line account, or as a regular monthly payment that lasts as long as the owners remain in the home.

As a rule, the borrower is not required to make any repayments until he or she vacates the home. Proceeds from the sale of the home may used to pay off the loan balance. Any excess of realized sale value over the value of the loan goes to the homeowners or their heirs. Because the loan is non-recourse, the borrower’s obligation cannot exceed the home value, regardless of how long the homeowners continue to occupy their home.

| Quote from 3/20/10 | |

| Home Value | $300,000 |

| Age of Youngest Owner | 75 |

| Advance or Credit Line Available | $162,915 |

| Monthly Funds Available | $1,120 |

| Variable Loan Interest Rate | 2.73% + .5% mortgage insurance fee = 3.23% |

Here is a sample quote (3/20/10) from Wells Fargo, currently the largest reverse mortgage lender in the United States.

The “Advance or Credit Line Available” is significantly less than the home value because the loan balance grows over time with interest. Amounts available will vary inversely with current interest rates, and directly with the age of the owner.

The “Monthly Funds Available” is the annuity-like payment that owners can choose to receive as long as they remain in their home. The “Variable Loan Interest Rate” in this quote is based on a spread over Libor.

(Note: in examples that follow, I’ve used a projected 6.00% borrowing rate instead of 3.23%. Current rates are at historic lows, so I’ve based the examples on a rate more in line with past averages.)

Fees

Now for the scary news. Here are typical fees based on the above example.

| Typical Fees | ||

| Origination Fee—paid to lender | 2% of first $200,000 of home value, 1% above $200,000 | $5,000 |

| Closing Costs—paid for legal, appraisal, and other services | Similar to a conventional mortgage | $2,500 |

| Mortgage Insurance Premium—Paid to FHA/HUD for guarantees | 2% of home value + .5% of loan balance | $6,000 + .5% of loan balance (included in the 6.00% projected borrowing rate) |

| Servicing Fee-paid to lender for monthly servicing | $35 per month | |

| Total Up Front Fees | $13,500 | |

The total fees are much higher than for conventional mortgages. Fortunately for borrowers, most of these fees can be financed and do not require up-front cash. One way to understand the impact of the fees is to look at the effective loan interest rate as a function of how long the homeowner stays in their home and keeps the reverse mortgage. This calculation is based on the cash the borrower receives and the loan amount paid back at maturity.

| Duration of Reverse Mortgage | Effective Interest Rate—Monthly Pay Mortgage | Effective Interest Rate—Lump Sum Mortgage |

| 5 years | 14.85% | 7.81% |

| 10 Years | 8.76% | 6.98% |

| 15 years | 7.44% | 6.69% |

| 20 years | 6.93% | 6.54% |

| 20 years (example when home value limits loan amount) | 5.61% | 5.56% |

The effective interest rates show the impact of the up-front costs. For example, a homeowner taking out a monthly pay reverse mortgage and keeping the mortgage for five years, would be effectively borrowing at a rate close to 15%.

However, for borrowers who stay in their homes for longer durations, the rates look much more attractive. The rates shown in the last line of the chart are based on an example where home prices increase 2 ½% each year and loan balances eventually bump up against home values, effectively lowering the borrowing cost.

The chart illustrates the point made by many loan counselors: that homeowners should not consider a reverse mortgage unless they expect to remain in their home for a long time.

The Lump-Sum/Annuity Alternative

It is almost never a good idea to borrow money to buy a financial product, but it may be worthwhile to consider taking a lump sum reverse mortgage to purchase an annuity that produces lifetime income. The type of annuity could be either an immediate annuity or a variable annuity with a guaranteed lifetime withdrawal benefit.

Advertisement

In the following example, a hypothetical 75-year-old woman owns a house worth $300,000 (mortgage-free). She would like to generate as much income as possible from the equity in her home. Based on the Wells Fargo quote (above), she could take out a reverse mortgage that would pay her $1,120 per month for as long as she stays in her home. Alternately, she could take the maximum lump sum, $162,915, and buy an immediate annuity (with no refund at death) that, based on Vanguard/AIG rates, would pay $1,281 per month, thus increasing her monthly income by $161.

As another option, she could buy a variable annuity with a guaranteed minimum death benefit. For a 75-year-old, the guaranteed withdrawal percentage would typically be 5%. Unfortunately, 5% would only generate $679 monthly, assuming she purchased the annuity and immediately began taking withdrawals.

Impact on Estate Values

Another important consideration is the impact on amounts left to heirs. The following chart provides a comparison of the three product options in terms of the estate values at different durations.

The estate value is the difference between the home value (assumed to increase 2 ½% annually) and the loan value, for both the immediate annuity and the reverse mortgage strategies. For the variable annuity strategy, the estate value also includes a projection of the growth of the assets in the VA account. The estate value cannot be less than zero.

Not surprisingly, the strategies that produce high monthly incomes produce the low estate values.

The difference between the estate values for the reverse mortgage strategy versus the immediate annuity strategy reflects the lack of a refund feature in the immediate annuity. (An immediate annuity with a refund feature would produce substantially less monthly income.) By contrast, the monthly pay reverse mortgage is like an annuity that pays a refund equal to the home’s net equity value.

The monthly reverse mortgage strategy does better than the immediate annuity strategy up to about age 90 in this example, so it is likely to be the favored strategy if the borrower has legacy interests.

The variable annuity strategy produces the highest estate values, but that’s primarily because monthly income is drastically reduced.

Present Value Measure

It is not straightforward to judge the tradeoff between monthly income and estate value, so the next chart uses present values to combine them into a single measure.

I used the 6.00% borrowing rate to calculate the present values. Based on this measure we can see that attractiveness of the immediate annuity strategy depends on longevity-early deaths are penalized, and long lives are rewarded.

The variable annuity strategy performs the worst under this measure. It is completely dominated by the reverse mortgage. (For variable annuity product charges, I assumed a total of 2.25% annually to cover product fees, investment expenses, and GLWB fees.)

For all three strategies there’s a change in tilt between years 15 and 20, which reflects loan values bumping up against projected home values.

These results will vary depending on choice of assumptions, but, nonetheless, I feel this analysis provides a reasonable comparison of the product alternatives.

Conclusions and Future Analysis

The key conclusions I draw form this analysis are:

- Despite their high fees, reverse mortgages can be attractive for individuals who plan to stay in their home for a long time.

- Effective borrowing costs are exorbitant for shorter-term loans.*

- The monthly pay reverse mortgage provides 10%-15% less income than using an immediate annuity, but provides substantially more value in the event of an early death.

- For maximum income if estate value is not a concern, consider taking a lump sum reverse mortgage and investing the funds in an immediate annuity.

- A strategy of purchasing a variable annuity with a guaranteed withdrawal benefit with a lump sum reverse mortgage does not appear competitive.

* Most reverse mortgages offered currently are under the HUD/FHA Home Equity Conversion Mortgage program, and fees are based on maximum allowances. If the market grows and become more competitive, products may become available with reduced up-front fees that will make them more attractive for shorter durations.

This article offers a start at analyzing the reverse mortgage as a retirement income product, but more research is needed. This analysis was done on a before-tax basis, and a more refined evaluation needs to consider tax effects.

It would also be useful to look at examples where the client has both housing wealth and other savings, and therefore more options in creating retirement income. This analysis can also be improved by developing stochastic forecasts to compare the risks in various strategies.

Such additional research can lay a foundation for incorporating the reverse mortgage product into financial planning software.

© 2010 RIJ Publishing. All rights reserved.

New Public Pension Fund in UK Ponders Investment Strategies

In Britain, the chief investment officer of the Personal Accounts Delivery Authority (PADA) suggested that a proposed national trust fund for private savings accounts should start by investing conservatively, rather than taking excessive risks.

PADA was set up under the Pensions Act of 2007 to create a national, trust-based pension plan called NEST (National Employment Savings Trust)—a system of personal investment accounts targeted especially for use by low and middle-income workers whose employees may or may not have a workplace savings plan.

Debate has been going on since last year over how the assets in the trust fund should be invested. Mark Fawcett, PADA’s chief investment officer, said that the impact of high volatility in the first five or 10 years of the fund could cause people to give up contributing to personal accounts.

“If we want to build a savings culture, why give them [members] volatility. Keeping them in and keeping them saving is more important than taking a lot of risk in the early years,” Fawcett told delegates at last week’s National Association of Pension Funds meeting in Edinburgh, Scotland, in mid-March.

Under the plan, which is currently scheduled to take full effect in 2012:

- Employers will be required to automatically enroll eligible workers into a workplace pension and make a minimum contribution to their pension.

- The Pensions Act 2008 allows for the introduction of automatic enrollment to be introduced in stages. New duties are expected to fall on large employers first, but the details of how the new duties will be staged are still to be confirmed. This will be specified by secondary legislation.

- A minimum employer contribution of three percent on a band of earnings will be required. However, contributions can be more than this.

- The total minimum contribution for eligible workers should equal eight percent of that band of earnings. This is made up of employer contributions, worker contributions and tax relief.

- Contributions from both employers and employees will be phased in over a transitional period. Minimum employer contributions are likely to initially be one percent on a band of earnings; rising to two percent before reaching the full three percent.

© 2010 RIJ Publishing. All rights reserved.

‘What Do You Want 2Retire?’

Tourists naturally expect to see eye-grabbing electronic billboards in New York’s famous Times Square. One of the newest of the giant ads has been posted by Merrill Lynch above a branch of the Bank of America, Merrill Lynch’s parent, at Broadway and 46th St.

The billboard is the newest component of Merrill Lynch’s “help2retire_____” (read “help2retire blank”) advertising campaign, which invites the investing public to think about what aspects of their daily routines they would like to “retire”—that is, get rid of.

Between March 19 and April 2, the billboard will urge Times Square visitors to send text messages to the billboard, naming the thing they would most like to “retire.” A tally of the responses will be “displayed in real-time.”

The campaign is counter-intuitive in that it focuses investor attention on negative aspects of their pre-retirement lifestyle—such as traffic jams and pinstripe suits-rather than on traditionally positive images of retirement goals, such as sailing, golf, or exotic travel.

Merrill Lynch Wealth Management has also been promoting its “Retirement Income Framework,” which divides a retiree’s investments into short-term, immediate-term and long-term portfolios that satisfy, respectively, immediate consumption expenses, the need for “longevity and income replacement,” and bequests.

Bank of America/Merrill Lynch serves approximately 59 million consumer and small businesses in the U.S. through 6,000 retail banking offices, more than 18,000 ATMs and online.

© 2010 RIJ Publishing. All rights reserved.

New Organization Seeks 401(k) Reform and Much More

Five different groups in Washington, D.C., have created a new public policy organization, Retirement USA, to identify and promote a new kind of national retirement savings plans that would supplement 401(k) plans.

The five organizations include two labor unions, the AFL-CIO and th e Service Employees International Union, and three pension research or advocacy groups, the Economic Policy Institute, the National Committee to Preserve Social Security and Medicare, and the Pension Rights Center.

“So far we’ve been raising awareness of the crisis in retirement income,” said Nancy Hwa, a spokesperson for Retirement USA. “We had a conference last October, we’ve looked at proposals for new kinds of systems, and we’ve looked at what’s happening in the Netherlands and Australia on this issue.

“There are two tracks we’re working on, a short-term and a long-term track. We want to improve the current system, but things like [the Obama Administration’s proposed] Auto-IRA are just short-term fixes. The group’s real focus is long-term. But even in the future, we’re not saying we have to scrap what we have now and go for something entirely different.”

The group solicited proposals for a new kind of retirement system last fall and has selected five of those proposals for further consideration. The proposals and their authors, in parentheses, are:

Guaranteed Retirement Account Plan (Teresa Ghilarducci). The GRA proposal mandates a contribution of 5% of earnings (up to the Social Security wage base) for all workers, evenly divided between employer and employee.

The employee’s share of the contribution would be offset by a $600 refundable tax credit, which offset contributions by those with incomes below $24,000. The contributions of husbands and wives would be combined and divided equally between their individual accounts.

The plan would guarantee a real 3% annual rate of return. Surpluses would be distributed to participants. A balancing fund would be maintained to ride out periods of low investment returns.

Account balances would be converted to inflation‐adjusted annuities upon retirement, with a partial (10%) lump sum available. A full‐time worker who contributes into the plan for 40 years and retires at age 65 can be expected to receive income equal to roughly 25% of pre‐retirement income.

The plan would also provide a death benefit of one‐half the account balance for participants who die before retiring. Those who die after retirement could bequeath to their heirs half their final account balance less the total of benefits received.

Guaranteed Benefit Plan (Mark Ugoretz). The proposal is based on the ERISA Industry Committee’s Guaranteed Benefit Plan, which is part of a larger proposal titled the New Benefit Platform for Life Security.

One of the benefits proposed for the new Lifetime Security Plan is a Guaranteed Benefit Plan (GBP), which would provide a single source of retirement income. The GBP is a hybrid arrangement, similar to a cash balance plan.

The GBP would, at a minimum, guarantee the principal that employers and employees contribute to the plan, so that employees would be protected from a net loss. In addition the GBP would establish a minimum investment credit that would apply to the balance of each individual account.

Distributions from the GBP would be paid out at retirement only as a stream of payments or in annuity form. Because each benefit administrator is expected to enroll very large numbers of employees, this large pool should help bring down the cost of annuities, making them significantly more affordable to retirees. Further, the GBP would be guaranteed by the Pension Benefit Guaranty Corporation (PBGC).

These programs would be voluntary for the employer, although the program could be combined with a requirement that individuals whose employer does not offer a plan make minimum contributions to either a pension or retirement savings plan.

The New Benefit Platform calls for competitive independent benefit administrators to administer health and retirement plans. Benefit administrators would be liable for contractual and other common‐law obligations (similar to existing ERISA fiduciary responsibilities).

Guaranteed Pension and Community Investment Plan (Glenn Beamer).

Workers would contribute 5% of their wages to locally‐based funds and receive fully guaranteed lifetime annuities at retirement.

Workers, employers, unions and governments would be encouraged to contribute an additional 5% to 10% of wages. An 80% refundable tax credit would offset $560 of workers’ first $700 in contributions and replace the current deduction allowed for 401(k) plan contributions.

This tax credit would be deficit neutral or would decrease the deficit. The contribution structure would be progressive, and accounts would be fully portable. Full benefits would be payable when the participant’s age and service equals 100.

A locally elected board of trustees would administer the plan and would invest 70% of a worker’s account in a balance‐guaranteed account and 30% in community development. CPCI Community Investment programs would be determined and adopted locally. A federal agency similar to the Pension Benefit Guaranty Corporation will regulate CPCI plans.

Retirement-USA Plus Plan (Nancy Altman). The proposal would establish a defined benefit plan sponsored and administered by the federal government.

Plan participants would consist of all workers in employment covered by Social Security. Benefits would equal 20% of currently scheduled Social Security benefits. Retirement benefits would be paid automatically in the form of 100% Joint and Survivor Annuities.

Additional benefits would be paid directly to divorced spouses who were divorced after at least 10 years of marriage, dependent spouses, parents, children, and grandchildren. The Plan would provide group life and disability insurance, as well.

All benefits would be fully protected against inflation. In addition, all participants would have the option to convert tax‐favored and other savings into a supplemental annuity purchased through the Social Security Administration.

On the date of adoption, plan benefits would immediately vest in all workers who were insured for purposes of receiving Social Security benefits and would be immediately payable to all Social Security beneficiaries. Workers not then vested would become so when they became insured for purposes of receipt of Social Security benefits.

The plan includes two alternative financing mechanisms. The second would leave the plan in long‐range actuarial balance; the first, in long‐range surplus. The first alternative consists of (1) employer and employee contributions on earnings in excess of Social Security’s maximum, (2) revenue from requiring consistent tax treatment of employee contributions to salary reduction plans, (3) revenue from a dedicated federal estate tax, and (4) investment income on Plan reserves.

The alternative method is to require contributions by employers and employees of 1.5% each on wages insured by Social Security and to expand the Earned Income Tax Credit, in order to offset the cost for lower‐income workers.

Insured Retirement Accounts (Regina Jefferson). The proposal would provide insured retirement accounts for individuals not covered by individual employer‐sponsored plans.

Employer and employee would each contribute 3% of wages up to the Social Security wage base to the accounts. The contributions of low and moderate income wage earners would receive a public subsidy, which would be gradually phased out.

Contributions would be made to either a clearinghouse established by the Social Security Administration (or to another entity such as the Pension Benefit Guaranty Corporation). Investment assets would be pooled by the entity receiving them, and the investment function could be contracted out to investment professionals.

As described below, the pooled investment portfolios would be subject to some portfolio design parameters, which would reduce the risk of investment loss. Benefits would be paid as life annuities commencing at retirement age; disability benefits would also be available.

The insurance program and portfolio parameters are the innovative aspect of this proposal and are based on previous work suggesting an optional defined contribution insurance program for private sector plans. The primary idea of the insurance proposal is to protect participants from severe losses that occur close to their retirement.

The insurance would do this by providing that each year’s contribution would earn over an employee’s career no less than the average annual rate of return on a model portfolio that conformed to the investment parameters.

Variable Defined Benefit Plan (Gene Kalwarski). This proposal, developed by the United Food and Commercial Workers International Union, creates a new type of defined benefit plan, removes significant levels of risk inherent in today’s traditional defined benefit plan.

The VDB plan might be described as a floor‐elevator plan. Each participant would receive an annual floor benefit, which would be stated in the form of a uniform retirement annuity. (The benefit could be either a flat benefit or a percentage of pay, in which case the floor benefit would look like a career average defined benefit.)

The floor benefit would be actuarially determined from the plan’s contribution base for all participants in the plan as a uniform benefit, but using a very conservative interest assumption. The floor benefit would also be converted into investment units in the plan’s collective assets, which would be professionally managed. For example, a $100 floor benefit would purchase $100 of investment units.

These investment units would fluctuate in value annually, increasing in value in a year in which the plan’s investment return exceeded the conservative interest assumption (plus a reserve factor) and declining in value in a year in which the plan’s investment return fell below the assumption.

At retirement, employees would receive the greater of the sum of their floor benefits or the sum of their investment units. Benefits would be paid only in annuity form, although a plan could be structured to provide for death, disability, post‐retirement inflation protection, and/or early retirement.

© 2010 RIJ Publishing. All rights reserved.

From Genworth, a Less Painful Way to Buy LTC Insurance

Genworth Financial, Inc. has issued a long-term care/annuity hybrid product, joining the handful of companies who have take advantage of a provision in the Pension Protection Act of 2006, effective January 1 of this year, that resolves a tax technicality that barred such products in the past.

The Richmond, Va.-based insurers, new product, Total Living Coverage Annuity (TLCA) combines a single-premium fixed deferred annuity with long-term care coverage. It is underwritten by Genworth Life Insurance Company.

Like products announced last year by several companies (see RIJ, July 8, 2009, “A Short-Cut to Long-Term Care Insurance”), the product in effect allows owners of fixed annuities to withdraw the assets tax-free when applying them to long-term care costs. The cost of long-term care insurance is greatly reduced because the fixed annuity assets serve as a very large deductible. Genworth introduced a universal life insurance/LTC hybrid a few years ago.

The product, whose market consists of the estimated $96 billion in out-of-surrender-period fixed annuity assets in the U.S., will mainly save money for people with significant unused capital who would otherwise self-insure against the risk of incurring long-term nursing home or home health care costs.

Katie Liebel, vice president of fixed annuity products, described how the new hybrid works. If an investor put $100,000 into the new product, for instance, he or she could choose $200,000 or $300,000 worth of long-term care coverage, spread over a period of four or six years, she said. Inflation-adjustment is available as an option.

“Only seven percent of the people who are looking for long-term care insurance actually purchase it, and the other 93% are self-insuring,” Liebel said. “This allows them to self-insure more effectively.”

The product, which can be funded with assets from another annuity or life insurance policy, has a minimum premium of $35,000. Once invested, the money earns 3.25% (with a minimum guarantee of 3%) or as much as 3.65% if the premium is $150,000 or more.

As the assets grow, the issuer assesses an insurance charge of between 0.40% and 1.5% on the insurer’s exposure. The expense ratio depends on the amount of coverage purchased as well as the age and health of the purchaser. Liebel described the underwriting as “simplified, with no lab tests or review of doctors’ records.”

Over time, the annuity would grow and the insurer’s exposure would shrink, resulting in a steady decline in fees. The annuity owner could withdraw money from the contract, but doing so would cause a proportionate reduction in the amount of LTC coverage.

Many existing annuity contracts allow accelerated payouts for nursing home costs, but the distributions are not tax-free, as they are when combined with long-term care insurance.

© 2010 RIJ Publishing. All rights reserved.

Fund Fees Can Devastate 401(k) Savings: Towers Watson

Fund expenses can shave up to 30% from the value of a retirement account over a lifetime of savings and shorten the life of the account by as much as 15 years, according to a new analysis of target-date fund fees by the consulting firm Towers Watson. TDFs are widely used in 401(k) plans.

Differences in TDF fees, which can range from less than 20 basis points per year for passively managed TDFs to more than 180 basis points for actively managed TDFs, have a much bigger impact on variation in cumulative returns than the amount of equities in the fund or the fund’s design, the analysis showed.

“Most employees are losing a very material amount of their retirement assets due to fee-related erosion,” Towers Watson said. “While 20 basis point fees reduced retirement income by one to three years, fees of 50-100 basis points eliminated 7-12 years of retirement income for most participants.

“For savings rates of 8% or more, a 100 basis point fee reduced the age of savings depletion by 9-15 years for all salary levels. The analysis included the effect of Social Security payments, which helped lower-salary employees improve their years of retirement income but also meant they lost more security due to fees compared with high-salary employees at an 8% savings level.”

The study considered four salary levels ranging from $25,000 to $125,000, three savings rates (4%, 8% and 12% of salary), and three fee levels (20, 50, and 100 basis points).

Towers Watson assumed that the participant worked and saved from age 25 to age 62 and drew a retirement income from Social Security and 401(k) savings equal to 70% of their salary. Generally, the higher the salary, the higher the fees, and the greater the savings rate, the greater the impact of fees on the life of the portfolio.

The analysts suggested that some sponsors might persist in offering high-fee funds because they lack economies of scale, they are limited to their record keeper’s fund options, or because they use actively managed TDFs.

Plan advisors and plan sponsors may not like the idea of reducing fund fees in 401(k) plans, if statements made in a March 28 Investment News article are any indication.

The article quoted several advisors and officials expressing disagreement with a recent Department of Labor initiative suggesting that fees and expenses should play a bigger role than historical performance in the evaluation and choice of funds as 401(k) options.

Several advisors appeared to be outraged at the suggestion, implicit in DoL’s latest proposal on regulations governing investment advice for plan participants, that low-cost index funds are better for investors than actively managed funds. They were also evidently out raged that a shift to index funds might lower their revenues.

The article said in part:

“If the agency does set a bias toward passively managed funds, it could mean less business for financial advisers, experts said. If a plan sponsor decides to include only index funds in its plan, the client might not feel that it needs an adviser to help choose funds, said Thomas Clark Jr., vice president of retirement plan services at Lockton Financial Advisors LLC.

“It could also mean increased costs to plan sponsors because index funds offer less in revenue-sharing dollars than actively managed funds, and thus there is less money to cover record-keeping expenses, he said.

“Most advisers oppose the [DoL’s] questions mainly on principle. ‘This makes no sense to me,’ said Manny G. Erlich, managing director at The Geller Group. ‘They need educating.’ Any advice that doesn’t take into consideration the past performance of funds isn’t good advice, Mr. Francis said.

“A bias toward passively managed funds, leading to more 401(k) plan sponsors adding index funds to their lineups, would also have a negative impact on employee engagement in saving for retirement, said Paul R. D’Aiutolo, vice president of investments, advisory and brokerage services at UBS Institutional Consulting.

“‘The purpose is to keep people engaged in their plans,’ he said. While index funds may perform well over the long term, it’s often the ups and downs of actively managed funds that keep plan participants paying attention,’ Mr. D’Aiutolo said.”

© 2010 RIJ Publishing. All rights reserved.

Insult to Injury: Disability’s Impact on a Retirement Plan

Picture this: You have a client who is ten years away from retirement. He comes to you for retirement advice. You spend several hours, maybe even a full day with him. You consider many different retirement scenarios.

At the end of this exercise, you prepare a plan that’s as thick as a phone book. In your next meeting, you review the plan with your client.

One of your suggestions is that he buy disability (a.k.a. income replacement) insurance, in case he can’t work and earn income. But your client says that his employer already gives him similar insurance. He has no interest in purchasing his own disability insurance. After some intense discussions, you fail to convince him.

“Oh well,” you think, “maybe he’ll come around soon.” After your meeting, you decide to hand over the plan to your client.

Perhaps the client was just being stubborn. Perhaps he thinks you’re only angling for a big, undeserved commission. Perhaps he genuinely believes that his company hired him for life and their plan is all he needs.

The bottom line is, you weren’t able to demonstrate clearly why he needed disability insurance in his overall retirement plan. But you might have been more persuasive if you had been able to show him the precise impact of a loss of income on his retirement accounts.

Advertisement

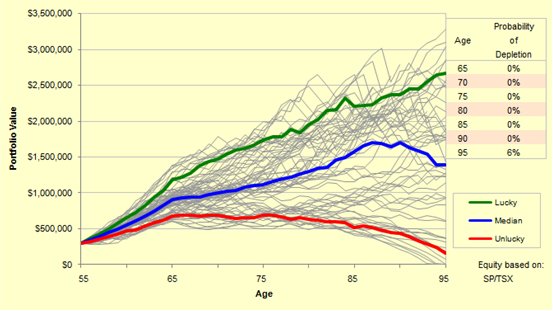

If you haven’t done that before, here’s an example: A couple, Bob and Sue, both 55, have about $300,000 in their retirement accounts. Their asset allocation is 40% equities and 60% fixed income. They intend to save a combined $25,000 each year until they retire at age 65. After retirement, they expect to need $50,000 a year, indexed to inflation. They anticipate $25,000 in combined Social Security benefits. They want their income to last until age 95.

In my case, I run this information through my retirement calculator, which is based on actual market history, and discover that they have a good plan (Figure 1). If they are lucky (top decile of all historical outcomes) and catch a good, long-term uptrend in the market, their portfolio will be worth about $2.7 million in 40 years. Even if they are unlucky (bottom decile of all historical outcomes), they’ll have about $165,000 at age 95.

Figure 1: Bob and Sue’s Retirement Assets over time

Well, not so fast. What if Bob loses his job? In that case, he also loses his disability insurance. Now he’s on his own. If he experiences a health problem or an accident and can’t earn income for awhile, he and Sue won’t be able to save $25,000 every year. Worse, they may have to spend some of their retirement savings to make ends meet. Their meticulous retirement income plan would go down the drain.

Figure 2 depicts the impact of a disability that lasts two years. The blue line on the graph in Figure 2 indicates the portfolio value if Bob has no disability insurance and he suffers no disability. Bob earns income continuously until age 65. Everything looks great; the portfolio lasts at least until age 95.

The red line depicts the portfolio value if Bob has no disability coverage and he becomes disabled during ages 55 and 56. Note that the portfolio life is shortened by 7 years. If Bob were single that might be acceptable, because a disability lasting two years might also reduce his life expectancy. But he needs to consider Sue. There is a 36% chance that she will be alive when their money runs out at age 88. This is not an acceptable retirement plan.

The red line depicts the portfolio value if Bob has no disability coverage and he becomes disabled during ages 55 and 56. Note that the portfolio life is shortened by 7 years. If Bob were single that might be acceptable, because a disability lasting two years might also reduce his life expectancy. But he needs to consider Sue. There is a 36% chance that she will be alive when their money runs out at age 88. This is not an acceptable retirement plan.

Finally, the green line on the chart indicates the portfolio value if Bob does have disability insurance. Even though he earns no income at ages 55 and 56, the portfolio value is only slightly lower than the blue line, because of the cost of the disability insurance. In this scenario, Bob and Sue still have income until age 95. This is a good retirement plan.

| Duration of total loss of income: | Portfolio life is reduced by: |

|---|---|

| 1 year | 1 to 7 years |

| 2 years | 5 to 11 years |

| 3 years | 8 to 14 years |

| 4 years | 12 to 17 years |

This table shows the impact of loss of income to portfolio life.

Remember that these numbers are only approximate. In this example, the assets were just barely adequate to cover the retirement income. If the client had already in been in what I call the “Red Zone,” the impact would be more severe.

Many factors can reduce the number of years in a portfolio’s life. These include the amount of excess assets already in the portfolio, the amount each spouse earns, when the disability occurs relative to retirement age, the amount of additional expenses the disability makes ne cessary, and whether or not one can collect government disability benefits.

However, the numbers in the table above might help you convince your client that, during the accumulation stage, disability insurance is not a luxury but a necessity for proper retirement planning. A retirement plan isn’t complete or comprehensive until you have carefully examined and covered the risk of disability.

Jim Otar, CMT, CFP, is a financial planner, a professional engineer, a market technician, a financial writer and the founder of retirementoptimizer.com. His articles on retirement planning won the CFP Board Article Awards in 2001 and 2002. He is the author of “Unveiling the Retirement Myth – Advanced Retirement Planning based on Market History” and “High Expectation and False Dreams” Your comments are welcome: [email protected].

© Copyright Jim Otar 2010

ING Offers a Simpler, Cheaper Variable Annuity

During the variable annuity “arms race,” ING was a full-fledged nuclear power. Just two years ago, sales of its LifePay Plus product, with its lavish 7% roll-up, were running over $1 billion a month.

Then the financial crisis hit, ending the arms race almost overnight. ING de-risked its product and pulled in its horns. VA sales in 2009, at $6.7 billion, were down almost 40% from $10.87 billion in 2007.

Now the Dutch-owned firm has undergone a reorganization, combining its annuity and rollover businesses into ING Financial Solutions, and it has revealed its first new variable annuity product design since the crisis.

The new variable annuity contract is Select Opportunities. The 7% roll-up has been stripped away, replaced by a simple ratchet. The price is over 100 basis points lower. It is part of a suite of products that ING introduced this spring under a new strategy that’s intended to offer advisors a variety of simplified products rather than multiple versions of a complicated one.

“We closed our other variable annuities as part of a broader strategy to take solutions to the market, as opposed to a single product,” said Bill Lowe, president and head of distribution for ING Financial Solutions.

“Before the financial crisis, every company was going after the same advisors with the same product—the variable annuity with a big benefit guarantee,” he told RIJ. “Now companies are going after different parts of the market.

Advertisement

“We’ve decided to go with a multi-product strategy—the fixed, indexed, and variable annuities and a mutual fund custodial IRA-based product. From a risk/reward perspective, we’re targeting the adviser with a whole spectrum of solutions,” he added.

Select Opportunities is a bundled product, with one death benefit and one living benefit, both standard. It has three age bands and a shortened five-year surrender period that puts it “between a B-share and an L-share.” It is offered in a single life version only, with no joint-and-survivor options.

The all-in cost is about 2.25% a year, including 100 basis points for the living benefit rider, 75 basis points for the mortality and expense risk fee, and 50 basis points for the investment management.

“We’re going after any advisers who were turned off by variable annuities because of the price,” Lowe said. “There’s an inflection point where they just wont buy the product.”

The client’s annual payout rate—4% at age 65, 4.5% at age 70, and 5% at age 75—kicks in when the client enters each age band, regardless of when payments began. “It automatically steps you up, so there’s inflation protection,” Lowe said.

The contract offers 11 investment options, including three large-cap index funds, a midcap and a small cap index fund, two international equity index funds, a Treasury Inflation-Protected Securities fund, and a money market fund. The equity allocation is limited to 70% of the insured portfolio.

“We tried to keep it as simple as we possibly could,” Lowe said. “We’re trying to draw in the individual who says ‘there’s just too much optionality, it’s too confusing.’ The price is back to where annuities were in the early 1990s.”

© 2010 RIJ Publishing. All rights reserved.

Percentage of U.S. Households At Risk of Lower Living Standard in Retirement

Eating the Competition’s Lunch

In a conference room in the old American Lithograph Building on Park Avenue in Manhattan recently, 15 female New Yorkers listened intently to a fellow New Yorker talk to them in New York-ese about how to manage their 401(k) accounts better.

The women, all employees of Landor Associates, a creative firm that manages brands for firms like Citigroup, Federal Express and Pepsico, ranged in age from 25 to 60. The instructor was Tony Truino, an energetic, nattily dressed MetLife advisor with a fast, in-your-face-but-in-a-nice-way Brooklyn patter that suited this audience to a tee.

“The rule of 25… has anybody heard of it?” Truino asked. “It’s a quick way to calculate how big of a nest egg you’ll need to retire on.” If you spend one twenty-fifth of your savings, or 4% per year, he explained, “Statistically, you won’t run out of money. But what if you spend $100,000 on health care on the first two years? I wouldn’t use the rule of 25. It’s close, but it’s not absolute.”

The concepts rained down in bunches, and weren’t easy to absorb. “My head hurts already,” remarked one of the participants. “Where’s the roulette table?” joked another, perhaps imagining a simpler way to gamble.

And so it went for almost two hours, as Truino and accountant George Gerhard, his MetLife tag-team partner, clicked through PowerPoint slides on topics like the differences between stocks and bonds (“ownership versus loaner-ship”), the security of T-bonds (“the government will always print enough money to pay you back”) and so forth.

Advertisement

The women remained silent, but focused. This was serious stuff.

The seminar at Landor Associates in February was just one of dozens of similar brown-baggers conducted by MetLife advisors under the insurer’s Retirewise investment education program for 401(k) participants.

The programs, which generally consist of four two-hour mid-day sessions, have been conducted at companies all over the U.S. The subject matter ranges from the basics of investing to the complexities of retirement income planning. MetLife charges neither the participants nor the plan sponsors a fee.

Post-Crisis, people are waking up to Americans’ their overall lack of preparedness for retirement and the shortage of unbiased information for 401(k) participants about converting savings to income. Retirewise helps answers that need.

What’s noteworthy about the program is that MetLife conducts the seminars at companies where another company—like Fidelity Investments, for instance—is the 401(k) plan provider. MetLife will typically also have a relationship with the plan sponsor, perhaps the dental insurance provider.

Retirewise is therefore something of a Trojan Horse. It gives MetLife a chance to promote its brand on its competitors’ turf. Indeed, its advisors aren’t shy about offering one-on-one consultations to seminar participants when the program ends. The consultations frequently lead to rollovers to MetLife when the employees change jobs or retire.

The campaign is also noteworthy in light of the recent announcement of the formation of the Defined Contribution Institutional Investment Association, one of whose stated goals is to foster the retention of participant assets in their plans (or in “deemed IRAs” in the plan) even after they retire. If anything, the battle for participant assets is accelerating.

The program’s genesis

The program’s genesis

MetLife advisors have been conducting onsite education sessions for several years. But the roots of Retirewise in its current form go back to 2006, said Jeff Tulloch, a MetLife national sales director and manager of the insurer’s Individual Business Liaison Group, which includes Retirewise.

“It started with our CEO, Rob Henrikson, who comes out of the retirement business,” Tulloch said. “He knows we are facing a situation in America where it’s tough for a lot of people, where they’re responsible for their own retirement. So he asked us, ‘How do we leverage what we already do and apply it to what’s going in the market.’

“We looked at two of our U.S. businesses, the institutional business, which has 60,000 corporate customers, including 90 of the Fortune 100 companies, and our retail side, where we have 8,000 to 10,000 financial advisors. We started to think about leveraging those two—the customer relationships and the retail space.”

The Retirewise instructors or “specialists” include some of MetLife’s top producers. “We took a small subset of advisors who concentrate on retirement and are part of the retail field force, and we trained them as Retirewise specialists. It’s about 250 people, a small elite group whose members meet certain high-level criteria.”

A curriculum has gradually evolved over time. “We saw the lack of a comprehensive financial education program. We said, let’s incorporate things like investment principles and risk and get people thinking about their governmental benefits. There was no specific direction in terms of product or approach,” Tulloch said. MetLife does try to match the instructors with the audience, so it was no coincidence that at Landor, both the instructors and the audience were New Yorkers.

The program consists of four seminars. The first is devoted to the most basic issues: the importance of starting early to save for retirement, the principle of compounding and the Rule of 72, the impact of inflation, taxes, and fees on accumulation, the differences between various tax-deferred accounts, and so forth.

In the second seminar, the advisors describe the building blocks of a portfolio, including stocks, bonds, mutual funds and annuities. (MetLife is a leading seller of variable annuities with living benefits.) Concepts like asset allocation, diversification, and dollar cost averaging are also covered.

The third part of the program delves specifically into the transition from work to retirement. It covers payout options from defined benefit and defined contribution plans, the merits of income annuities, and the maximization of Social Security benefits. The fourth and final seminar involves aging, estate planning and insurance questions.

“We settled on a four-part program, with two hours in each part,” Tulloch told RIJ. “At the beginning, we wondered, will employees go for that? Eight hours is a long time, and you have prep work and homework on top of that. Our conclusion was, this is a lot of information to cover and even eight hours isn’t enough to do it right. So part of the message of the program is, this is just a launching pad for your financial education.”

Post-seminar consultations

So far, MetLife has conducted about a thousand Retirewise programs at about 500 different companies, reaching about 25,000 participants. People of all ages and income levels attend the voluntary sessions. The average age is about 45. An estimated 40% of the participants, MetLife has found, regard their employer-sponsored plans as the foundation of their retirement security.

Northeast Utilities, a power company in southern New England, has been the site of 25 to 30 different MetLife 401(k) education seminars over the past four or five years. The company employs 6,000 workers at four electric utilities in Connecticut, Massachusetts and New Hampshire.

Keith Coakley, the firm’s Director of Compensation and Benefits, said that NU first hosted a MetLife education program in 2004, when it invited advisors from Barnum Financial Group, an arm of MetLife, to counsel employees during NU’s transition from a defined benefit to a defined contribution pension plan. MetLife was (and is) a provider of home and auto insurance to NU employees.

Fidelity Investments is NU’s 401(k) provider. The Boston-based fund giant has offered to send its own investment counselors to NU, along with the printed education materials that it regularly sends out to its plan sponsors and participants. But NU was happy with MetLife and wanted to keep things simple.

“We don’t bring them both in,” Coakley told RIJ. “We once had a situation where we had two entities offering advice here. We found that it was a little confusing and even a little overwhelming for employees. So we decided to have one onsite presence. Employees can go to the nearby Fidelity office for advice if they want to, and Fidelity is always good over the phone.

“Prior to MetLife we had three different firms who were provided training, and it took a lot of effort to select the ones who didn’t sell so vigorously that the employees felt they were getting a sales pitch,” he added. The employees didn’t feel pressured by MetLife, and NU lost no staff time. “MetLife does all the meeting planning. We do almost nothing.”

Sober assessment

MetLife may use the soft-sell approach, but it does sell. Tulloch estimates that as many as half of the seminar attendees ask for a one-on-one consultation with an advisor after the program ends. Those meetings may or may not lead to ongoing professional relationships. But MetLife has found that the program also helps the plan provider.

“We wondered, how will this play with 401(k) providers? Would employers see how our program and the providers could work together? We found that the 401(k) providers benefit from what we’re doing,” he said.

“I was at a debriefing with an employer in California a year ago, and the human resource manager commented that after the seminar they’d seen an uptick in the contributions,” he added. “The specialists talk about increasing participant savings rates by one percent or so.”

While they’re heartened by the success of Retirewise, the program has brought MetLife officials to a sobering assessment of Americans as retirement savers.

“There’s been a verification in my own mind that we are a nation of procrastinators and spenders, who are concerned about retirement but don’t know where to start,” Tulloch added. “Employees tell us, ‘I know the basics of investing, but I don’t know how to pull it all together.’”

As MetLife spokesman Pat Connor put it, “We’ve learned that people don’t think about the retirement issue very much.”

© 2010 RIJ Publishing. All rights reserved.

Social Security Cash-Flow Turns Negative

The Congressional Budget Office says the Social Security system will pay out more in benefits this year than it receives in payroll taxes, an event not expected until at least 2016, The New York Times reported.

Unemployment has forced many people to apply for benefits sooner than planned while also reducing payroll tax revenue. But Stephen C. Goss, chief actuary of the Social Security Administration, said that the change would not affect benefits in 2010.

The $29 billion shortfall projected for this year is small, relative to the roughly $700 billion that should flow in and out of the system, Goss said. The system, he added, has a balance of about $2.5 trillion that will take decades to deplete. The cushion is expected to grow again if the economy recovers.

Indeed, the Congressional Budget Office’s projection shows the recession easing in the next few years, with small Social Security surpluses reappearing briefly in 2014 and 2015.

After that, demographic forces are expected to overtake the fund, as more and more baby boomers leave the work force, stop paying into the program and start collecting their benefits. At that point, outlays will exceed revenue every year, no matter how well the economy performs.

Although Social Security is often said to have a “trust fund,” the term really serves as an accounting device, to track the pay-as-you-go program’s revenue and outlays over time. Its so-called balance is, in fact, a history of its vast cash flows: the sum of all of its revenue in the past, minus all of its outlays. The balance is currently about $2.5 trillion because after the early 1980s the program ran surpluses, year after year.

Now the balance will slowly start to shrink, as outlays start to exceed revenue. By law, Social Security cannot pay out more than its balance in any given year.

For accounting purposes, the system’s accumulated revenue is placed in Treasury securities. In a year like this, the paper gains from the interest earned on the securities will more than cover the difference between what it takes in and pays out.

© 2010 RIJ Publishing. All rights reserved.

Vandalism Follows Obama Health Bill Signing

On Tuesday, President Obama signed H.R. 3590, the Patient Protection and Affordable Care Act bill, saying it will lead to “reforms that generations of Americans have fought for and marched for.”

On Wednesday, law enforcement officials reported that Democratic legislators had received death threats and been the victims of vandalism because of their votes in favor of the health care bill, according to The New York Times.

Meanwhile, the Senate parliamentarian has ruled informally that the “Cadillac health plan excise tax” provision in a second major health bill, the Reconciliation Act of 2010, complies with the rules governing budget reconciliation bills.

The House passed the Reconciliation Act, H.R. 4872, Sunday, but the Senate still must pass it before Obama can sign it into law. Several Democratic officials and lobbyists are predicting that Democrats can count on getting 52 votes for H.R. 4872. They are expecting the final vote to occur before the Senate leaves Friday for the two-week Easter recess.

Obama, who has often talked about the insurance struggles his own mother faced as she was dying of cancer, noted that some of the provisions in PPACA, particularly provisions affecting insurers, will take effect this year.

Republicans reacted angrily to the signing.

House Minority Leader John Boehner, R-Ohio called the event something that “looked and sounded like a liberal Democratic pep rally” for “a massive government takeover of health care.”

Sen. John McCain, R-Ariz., told an Arizona radio station that Democrats should not expect any cooperation from Republicans in the Senate for the rest of the year, according to The Hill, a Washington newspaper.

Officials in Florida, Pennsylvania, Texas and 11 other states have filed a suit to block implementation of PPACA is the U.S. District Court for the Northern District of Florida. The states are objecting to provisions that require individuals to have health coverage and provisions that would require states to pay to expand Medicaid programs.

Tom Currey, president of the National Association of Insurance and Financial Advisors, Falls Church, Va., said NAIFA members “are pleased that Congress has recognized the positive role that health insurance agents can play in helping small businesses and individuals acquire appropriate health insurance plans.”

If PPACA takes effect as written, agents should still to be able to perform their traditional role, Currey said, adding that he likes a provision that would increase penalties for individuals who fail to have health coverage.

© 2010 RIJ Publishing. All rights reserved.

Hartford Financial Prepares to Repay U.S. Treasury

Hartford Financial Services Group Inc. has completed the previously announced stock and debt offerings it is using to get out of the U.S. Treasury’s Capital Purchase Program, National Underwriter reported.

Hartford Financial borrowed $3.4 billion in 2009 from the CPP, which is part of the Troubled Asset Relief Program. To pay back the CPP obligations, Hartford has sold:

- About 60 million shares of common stock.

- 23 million “depositary shares,” which each represent a 1/40th interest in a share of Hartford’s 7.25% Mandatory Convertible Preferred Stock, Series F.

- $1.1 billion of senior notes, including $300 million in 4.00% senior notes due 2015, $500 million in 5.50% senior notes due 2020, and $300 million in 6.625% senior notes due 2040.

The underwriters exercised options to buy 7.3 million shares of the common stock and 3 million depositary shares. Hartford is seeking approval to use $425 million in debt offering proceeds and the proceeds of the stock and depositary share offerings to pay the Treasury back by repurchasing preferred shares it issued through the CPP program.

Hartford will use the rest of the senior-note offering proceeds to prepare to re-pay debt that will mature this year and next year.

“We were pleased with the execution of the capital raise,” Hartford Chairman Liam McGee says in a statement. “There was a high level of investor interest in our offerings and pricing was favorable, reflecting confidence in the Hartford’s future.” The Treasury Department will still have warrants to buy Hartford common stock. Hartford has not announced plans to buy the warrants back.

© 2010 RIJ Publishing. All rights reserved.

More Assets Moving From 401(k)s to IRAs

More people are rolling over their 401(k) savings into IRAs when they leave their jobs or retire, according to research published today by Charles Schwab, Pensions & Investments reported.

The research found 69% of assets held by 401(k) participants were distributed from former employers’ plans within 12 months of leaving a job, confirmed Eric Hazard, a spokesman for Schwab. Thirty-one percent kept their money in their former employer’s 401(k) plan.

Of the assets that were moved, 80% were rolled over into IRAs, 10% were taken in cash distributions, 8% were moved into new employer plans and 2% were taken in other forms of distributions, according to a Schwab news release on the report.

The research was based on records of 12,198 employees who left jobs in the fourth quarter of 2008; Schwab then checked where the employees had distributed their 401(k) assets by the end of 2009. The data were obtained from a database of 1.5 million participants in Schwab-administered 401(k) plans, Mr. Hazard said.

“We are definitely seeing an uptick in the number of 401(k) plan participants who choose to roll over plan assets instead of cashing out or leaving savings with a previous employer,” Catherine Golladay, vice president of 401(k) advice and education at Schwab, said in the release.

In an earlier study, Schwab found that among participants who left an employer in the first quarter of 2008, 57% of assets were moved out a former employer’s plan by the first quarter of 2009, while 43% of assets remained in the plan, the news release said.

Of those distributed assets, 75% were rolled over into IRAs, 14% were taken as cash distributions, 7% were transferred to new employer’s plans and 4% were taken in other forms of distributions, Mr. Hazard said.

© 2010 RIJ Publishing. All rights reserved.

Australians Want More Workplace Savings

Sixty-one percent of Australians support a rise in the Superannuation Guarantee to 12% and are prepared to pay for it with a direct contribution from their wages, according to a survey released March 15 by the Australian Institute of Superannuation Trustees.

Superannuation Guarantee is the official term for compulsory contributions to retirement funds made by employers in Australia on behalf of their employees. An employer must contribute the equivalent of 9 per cent of an employee’s salary.

There’s more to the situation than the contribution rate, however. The Australia system of private retirement accounts funded by employer contributions, which supplements a state old-age pension and private savings, is complicated by the way contributions are taxed, by the still-meager savings of older workers for whom the program arrived late in life, and controversies over the fees and commissions paid to the managers of the retirement funds.

The AIST-commissioned consumer survey, conducted March 3-11, was released at the Conference of Major Super Funds in Brisbane, according to Investment magazine in Sydney. It suggests many Australians are concerned that their current level of super contributions won’t provide them with enough retirement income.

AIST CEO Fiona Reynolds said it appeared that the community was ahead of the views of most politicians on the need to lift the level of super contributions.

“It seems that both the super industry and the public understand that 9% … is not going to deliver a comfortable retirement. We hope this message is received by the government and … that steps are taken to improve adequacy within our retirement incomes system,” Ms. Reynolds said.

The Superannuation Guarantee contribution was originally set at 3% of the employees’ income, and has been incrementally increased by the Australian government.

Since July 2002, the minimum contribution has been set at 9% of an employee’s ordinary time earnings. The 9% doesn’t apply to overtime rates but is payable on bonuses and commissions.

Although compulsory superannuation is now popular, small business groups resisted it at first, fearing the burden associated with its implementation and its ongoing costs.