Here are two papers on private credit, one on the suitability of target-date funds for low-income workers, one on the money-creating power of the Federal Reserve, and one that blames financial crises not, as Hamlet said, on our stars but on ourselves. Most of the papers can be found through a search by WP number at the National Bureau of Economic Research website.

“Why is Private Lending so Popular?” by David T Robinson and Melanie Wallskog. NBER Working Paper No. 34617.

“Private lending has exploded over the past two decades. To explore its rise, we focus on Business Development Companies (BDCs),” write these Duke University professors. “We show that their growth is intimately connected to growth in private equity. Many BDCs are directly connected to large private equity organizations, and their compensation structures mirror those in private equity.

“Private credit—lending to risky companies—and private equity—ownership of risky startups—appear to be different private markets businesses. But they meet or overlap in the world of Business Development Companies, or BDCs. Publicly-traded, BDCs not only provide debt for PE-sponsored deals, but also make PE-like investments themselves involving deferred interest, preferred equity, and exposure to underlying assets. Their growth is intimately connected to growth in private equity.

“We find that around 70% of the overall growth in the market has been from larger, PE-affiliated BDCs who appear primarily to support PE-sponsored transactions. Thus, providing debt to LBOs likely accounts for a majority of the overall rise in private lending’s popularity. Among non 4PE-affiliated BDCs, we find that the bulk of the recent growth in AUM occurs in BDCs with more complex investment portfolios. In other words, both ‘PE channels’ contribute significantly to the rising popularity of BDCs.”

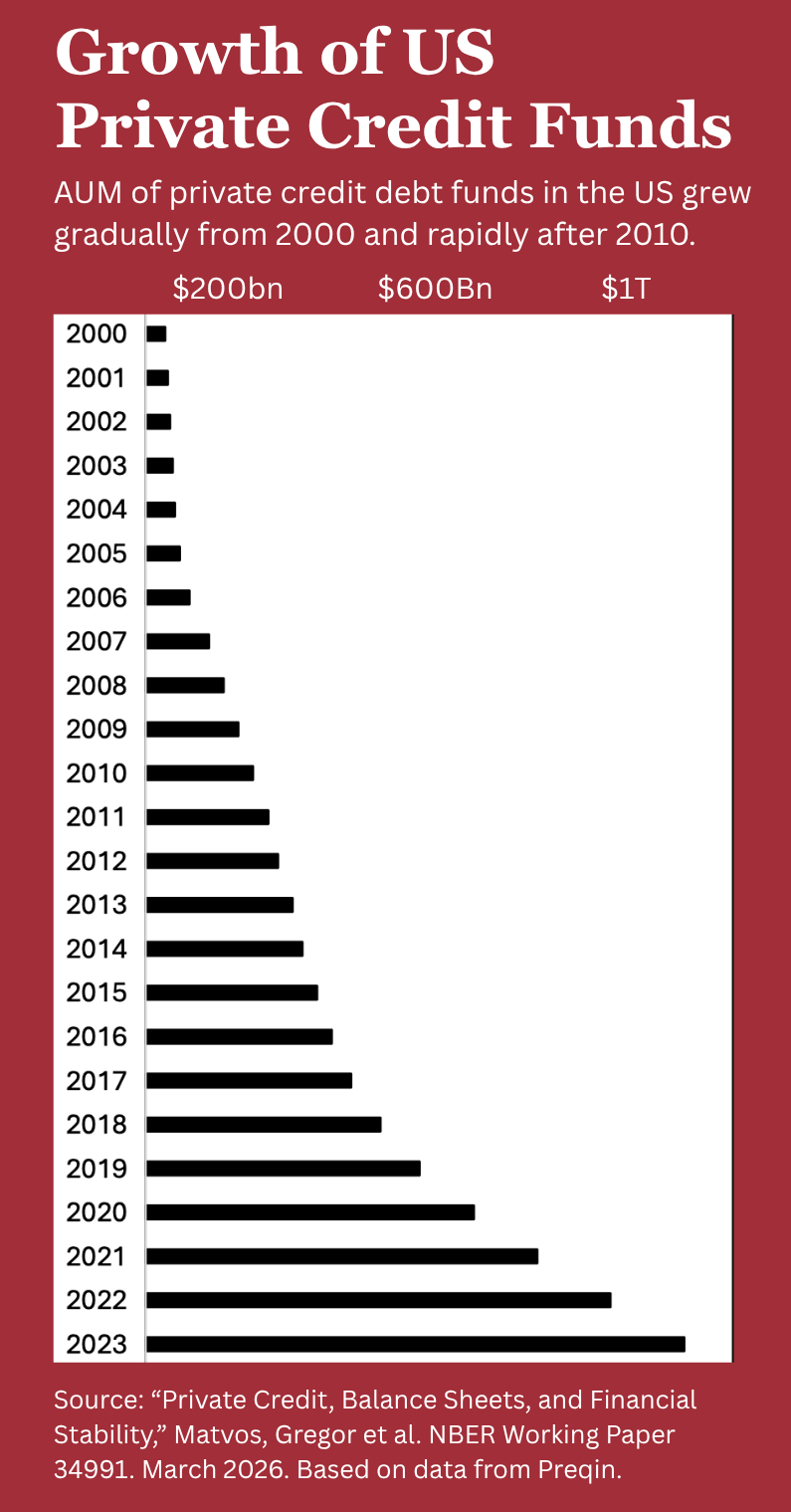

“Private Credit, Balance Sheets and Financial Stability,” by Gregor Matvos, Tomasz Piskorski, and Amit Seru. NBER Working Paper No. 34991.

In this industry-supported research paper, authors Gregor Matvos and Amit Seru of Stanford and Tomasz Piskorski of Columbia argue that “private credit funds appear conservatively structured and unlikely to pose systemic risks comparable to traditional banks under their current balance-sheet configurations.”

Using comprehensive fund- and asset-level data covering most of the industry, the authors show that “private credit funds are highly capitalized, with equity typically accounting for 65–80% of total assets—more than six times the capitalization of U.S. banks, where equity represents about 10%.

According to the paper, “Performance data show positive average net annualized returns with limited downside risk to creditors, as losses are largely borne by equity investors. Overall, private credit funds appear conservatively structured and unlikely to pose systemic risks comparable to traditional banks under their current balance-sheet configurations.

“Debt usage is moderate and largely reflects bank credit lines used for liquidity management. Fund lives average 10–12 years, while underlying loan maturities are generally shorter, implying little or no maturity mismatch—unlike banks, which fund long-term assets with short-term callable deposits. Private credit portfolios are diversified across industries, geographies, and credit strategies, reducing exposure to correlated shocks.”

The authors warn however that “potential vulnerabilities… could emerge as the sector grows, including governance and disclosure frictions, stress-period dynamics, bank–nonbank linkages, and the transmission of losses through limited partner balance sheets and retail investment vehicles.”

“Life Cycle Portfolio Choice with Human Capital and Social Security,” by Jason Scott, John B. Shoven, Sita Slavov, and John G. Watson. NBER Working Paper No. 34966.

“Target date funds – which initially invest a large share of retirement savings in stocks and shift gradually towards bonds over the life cycle – are designed to provide a ‘one-stop shop’ for retirement investing. The rationale for this pattern is that human capital, which is highest at the start of a worker’s career, is ‘bond-like,’” write these authors in the abstract of their research.

“Thus, utility is maximized when financial wealth is initially invested primarily in stocks, with the investment mix shifting towards bonds as the present value of future labor income declines. We revisit this logic in a dynamic model in which shocks to labor income are correlated with the stock market, and in which Social Security replaces a higher share of income for lower-income individuals.

“In line with empirical evidence, lower-income individuals in the model experience a higher degree of correlation between labor earnings growth and stock returns. We find that utility-maximizing retirement portfolios can vary greatly across individuals, deviating substantially from the pattern of a target date fund for lower-income individuals.”

“The Effect of Annuities on Longevity,” by Borja Larrain, Alessandro Previtero, and Felipe Severino. NBER Working Paper No. 35082.

This survey of the lives of 600,000 Chilean retirees from 2004 to 2022 shows that “the decision to annuitize—instrumented by recent market returns—substantially reduces mortality at five- and ten-year horizons. Further analyses indicate that annuities reduce mortality by shielding retirees from income volatility and investment-related stress. Complementary survey evidence suggests that annuitants invest more in health and report lower disability rates.

“Annuities can affect longevity through several interconnected channels. Annuities provide a stable source of lifetime income, reducing the likelihood that retirees face liquidity constraints. They also shield retirees from income uncertainty and anxiety associated with adverse financial market movements. Higher earnings and lower earnings volatility can increase both immediate and long-term longevity, consistent with evidence on job displacements in Sullivan and von Wachter (2009a,b).

“Similarly, stock market fluctuations can lead to stress, diminished mental health, and ultimately higher short-term mortality (Engelberg and Parsons 2016, Schwandt 2018). Finally, life-contingent payments from annuities can promote health investments (Philipson and Becker 1998), thereby improving health later in life and reducing mortality.”

“Democratic Sovereignty and the Prerogative to Make Money: The Case of the Federal Reserve,” by Christine Desan, Harvard Law School.

Desan is a Harvard Law School professor who has written about money’s role in society. In a new monograph, she examines, through her specialized lens, the ongoing power struggle between advocates of an all-powerful “unitary presidency” and those who believe that the Constitution dictates a “separation of powers” where the executive, legislative and judicial branches “check” each other’s over-reach.

The author of “Making Money: Coin, Currency, and the Coming of Capitalism” (Oxford, 2015), Desan sides with the latter. She argues that, while the Fed isn’t a branch of government, independence from the president was part of its founding purpose.

The constitutional conclusion follows: Congress’s prerogative over money-making clearly secures the Fed’s independence from presidential interference. That conclusion is lost in current scholarship that treats the Fed as fundamentally like other independent agencies. The Court has assumed, similarly, that the unitary executive presides over a relatively homogeneous regulatory field.

“Congress established the Federal Reserve System to carry out a critical legislative prerogative—making the sovereign money supply,” she writes. “Congress used an institutional form—national banking—innovated precisely to secure sovereign money-making from executive (originally monarchical) interference. Congress in turn assigned a vital responsibility—the capacity to make money out of debt in the people’s name—to the Fed.”

Those words suggest that Desan is a chartalist, or, like adherents to Modern Monetary Theory, on the chartalist spectrum. A chartalist regards money as a “creature of the law, created and regulated by the state to organize economic activity. The more traditional view is that money arose as an efficient substitute for barter and has no value unless tied to a valuable commodity, such as gold or silver.

“The Political Economy of Financial Crises,” by Charles W. Calomiris and Matthew S. Jaremski. NBER Working Paper No. 35101.

“The common narrative… that we are inherently vulnerable to external shocks is wrong. Instability is not a fact of nature,” according to this paper by Charles W. Caloramis of Columbia University and Matthew S. Jaremski of Utah State University

“Financial crises are better seen as a mirror of who we are as a society, reflecting our political structures, vying constituencies, cultural preferences, and blind spots. A proper understanding of financial crises thus forces us to face the awkward truth that the costs that attend financial crises are often self-inflicted.”

The authors show “how policymakers shape financial rules in ways that favor politically-influential groups but result in financial vulnerability. Key mechanisms include restricted bank chartering, safety nets, credit subsidies, and sovereign borrowing. Political forces also shape crisis management. Delayed interventions, selective support, and constrained policy responses can deepen and prolong crises.

“Instead of seeing financial crises as arising from an unavoidable vulnerability to external shocks they are better seen as a mirror of the societies in which they occur, reflecting their political structures, vying constituencies, cultural preferences, and blind spots.”

© 2026 RIJ Publishing LLC.