“Progressive” is not a word typically associated with the annuity industry’s online efforts. The annuity account opening process continues to be arduous and efforts to fully automate and streamline the online process have stalled. Additionally, annuity client and advisor websites lag behind other segments of the financial services industry, such as banking and brokerage, in terms of online account management and client servicing functionalities.

While some of these shortcomings can be attributed to stringent regulatory policies, much of it also has to do with the average age of annuity customers. Annuity contract holders are generally older than most investors, a result of the products’ retirement-focused payout structure. The recommended age to purchase a variable annuity is 55 and recent surveys show the average age of annuity owners is currently 70, up from 66 in 2005.

This brings us to annuity firms’ reluctance to implement social media capabilities on their consumer and advisor websites. A look at the average age of users shows why annuity providers may still be hesitant to get on board: recent surveys conducted by HitWise have found that 59% of the users on social networking sites are between the ages of 18-34 — not exactly the target audience for annuity firms. While the number of users 55 or older has increased by 77% over the last year, this group still accounts for only 5% of the total user base. Moreover, the main draw for many 55+ users surveyed was reconnecting with old friends and staying in touch with family.

Despite the apparent age and lifestyle discrepancies between social media users and annuity investors, a few firms have introduced social media features to clients and prospective investors with varying degrees of success.

Over the last two years, AXA Equitable and TIAA-CREF have both taken a stab at customer-facing social media projects. Among the firms we cover, TIAA-CREF has been the most active and most successful to date. The firm recently launched the final version of myretirement.org, after first making a beta version available to select participants in February 2007.

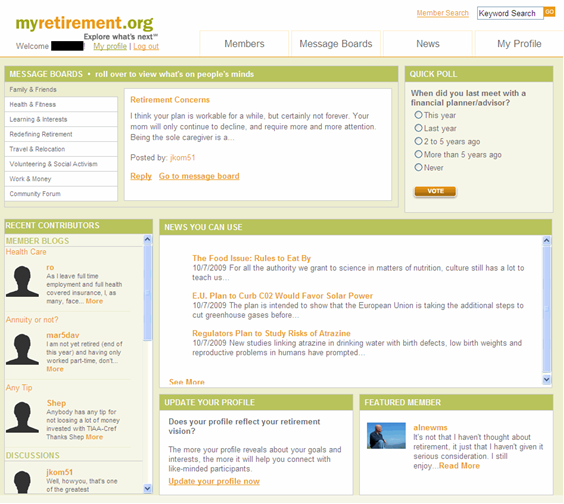

Myretirement.org offers message boards that allow TIAA-CREF clients to discuss a broad range of financial and lifestyle topics, ranging from investment strategies to travel and leisure. Users create custom profiles with personal images and are able to view other member profiles. Myretirement.org also lets members connect directly via friend requests, a popular feature borrowed from larger social networking sites.

MyRetirement.org Homepage

AXA Equitable introduced MyRetirementShop.com in July 2008. The sitelet combined investment education content and lifestyle resources (concierge service for purchasing event tickets, golf reservations, etc.) with open forums promoting discussion among community members on a variety of topics.

With nearly 10,000 members and several hundred posts, TIAA-CREF’s myretirement.org seems to have established a solid footing among TIAA-CREF plan participants. Conversely, while AXA’s MyRetirementShop.com remains publicly available, the open forums (the lone social networking aspect of the site) were removed in October 2008 due to a lack of participation.

The relative success of TIAA-CREF’s social network shows that annuity providers can do well in the social media space. But why did TIAA-CREF succeed while AXA languished?

The answer may lie in the phased roll-out and development of the TIAA site, the firm’s philosophy governing the end-user experience, and the unique nature of the firm’s customer base. With Myretirement.org, TIAA-CREF created an open social networking site that fostered a truly collegial atmosphere. By allowing members to communicate directly and building the site around user-driven message board content, TIAA ultimately allows the end-user to determine their experience. AXA’s MyRetirementShop, on the other hand, highlighted content provided largely by the firm, making the open forums feel secondary. The site also imposed significant barriers to entry, including a separate registration process.

TIAA-CREF had another advantage in that the firm’s clients tend to be drawn from certain professional backgrounds, specifically the academic, medical, research and cultural fields, i.e., those that “serve the greater good.” This shared experience provides a strong foundation for an online community.

TIAA-CREF’s decision to initially release a beta version of myretirement.org for select clients also contributed significantly to its success. During the roughly two plus years of the beta release, the firm was able to use feedback to improve site features and work out the kinks, while at the same time seeding the community with active users. Thus, when the final version went live, the site was already chock-full of user-generated content. AXA, on the other hand, launched MyRetirementShop.com without seeding the community, meaning that when users first accessed the site, they found an online ghost town.

Thus far, annuity firms’ general hesitancy to enter the realm of social media has been justified — the current crop of annuity clients has not taken to social networks in any truly meaningful way. But this will not be the case forever. After all, on networks like Facebook, the fastest growing demographic is users 35 years old and older.

© 2009 Corporate Insight, Inc. All rights reserved.

Industry Views are special reports that are sponsored and independent from RIJ’s editorial content.