Ironically, the bankruptcies of multi-billion dollar life insurers owned by publicly-held Baldwin-United (in 1983), First Executive (1991), and First Capital Holding (1991) didn’t scare major mutual life insurance companies away from changing into stock companies. On the contrary.

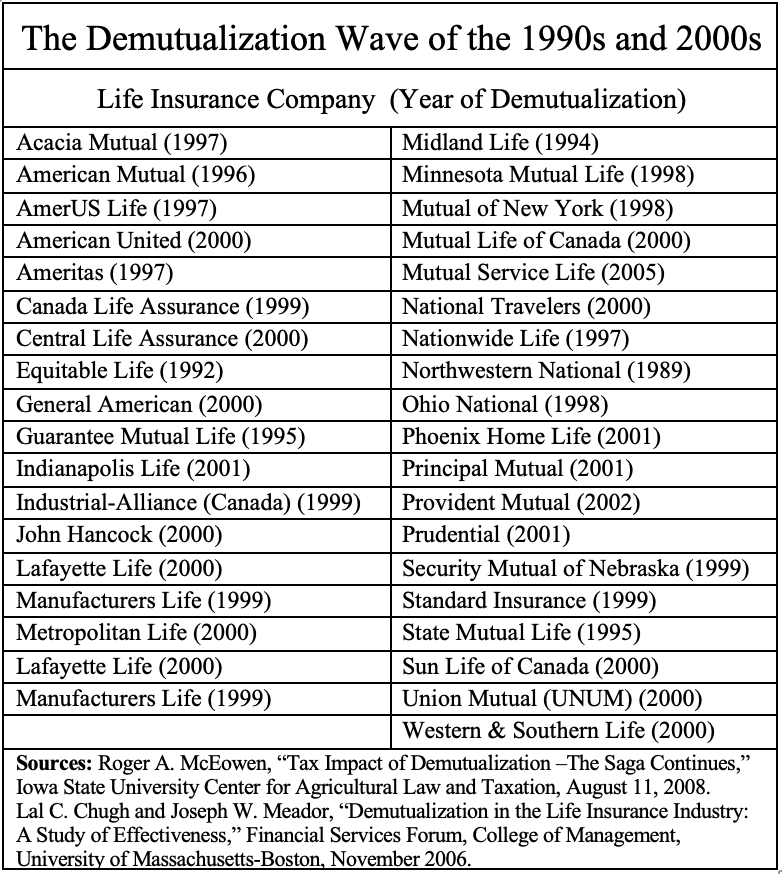

Starting with The Equitable in 1992, a wave of household-name mutuals would “demutualize” in the 1990s and early 2000s. From then on, they would be owned by investors and not, as they had been, by the people who bought their life insurance policies and annuities.

As stock companies, they could do what mutual insurers couldn’t: Hold an initial public offering, sell shares, and raise billions of dollars in fresh capital. In doing so, they hoped to compete in a rapidly consolidating financial services industry where scale would be the price of survival.

The watershed year was 2000 when, after Congress repealed the Glass-Steagall Act, a dozen large mutuals, including Prudential and MetLife, celebrated the end of the old millennium by becoming either stock insurance companies or “mutual holding companies” that owned stock insurance companies.

What few recognized, then or even today, is that stock life insurance companies are fundamentally different from mutual life insurance companies. To varying degrees, and with good as well as regrettable consequences, demutualization changed a company’s priorities, products, profit requirements, relationships with customers, and even their corporate cultures.

What is ‘demutualization’?

There are three types of life insurance companies: stock, mutual, and fraternal. We’re interested in the first two; fraternals tend to be small. Mutual life insurers play two important but narrow roles in the economy. Owned by their customers—the policyholders—they’re tasked with providing those owners (or “members”) with life insurance and annuities at the lowest possible cost.

All life insurers support the overall economy by lending to businesses. That is, they buy mostly corporate bonds and hold them to maturity. The profitability of mutuals depends mainly on the difference (the “spread”) between the yield on their bonds and the benefits they’ve promised to policyholders.

If a mutual earns more on its investments than it needs, it pays dividends to its policyholders, thus lowering their cost of insurance even more. Since mutuals are akin to non-profits, and provide a public good, all life insurers in the U.S. enjoy favorable tax treatment of their products and relatively light regulation by state insurance commissions.

The strength of mutuals is also their weakness. Gibraltar is impossible to move; for the same reason, it’s not very nimble. A mutual insurer can’t raise large amounts of fresh capital overnight or seize new opportunities in fast-changing times. But since they don’t have investors to cheer on that kind of behavior, they have no incentive to do so—unless or until their survival is at stake.

Stock companies are fundamentally different creatures. They are owned by their shareholders, who include individuals and institutions like pension funds and endowments, not by their customers. Unlike policyholders, who seek relief from risk, investor-shareholders seek risk and its ability to deliver wealth. Where mutuals rely on the spread for their profits, stock life insurers prefer to rely on asset management fees.

From the Panic of 1837 to the turn of the 20th century, most U.S. life insurers had been stock companies. After the Armstrong Committee’s exposure of stock insurance company mischief in 1905, many became mutuals. But the 1970s would change the financial game. The abandonment of the gold standard and unprecedented inflation in 1971, which led to the soaring interest rates of the early 1980s, disrupted the entire U.S. financial services industry.

To compete in a rapidly diversifying and consolidating financial service industry, many mutual life insurers felt they needed more resources and flexibility. Conversion to the stock company model, in a legal process opaquely called “demutualization,” presented a path to growth, independence, and higher profits. Once a few large mutuals showed the way, the herd followed.

Between 1997 and 2001, five of the 15 largest U.S. life insurers demutualized. Ten other major life insurance companies, with total assets in 2003 of $775 billion, demutualized over the same time period [Meader and Chugh]. Of the 1,470 life insurance companies that were in business in the United States at the end of 1999, only 106 were still mutual companies, or 7% of the total. But they included giants like MassMutual, New York Life, and Northwestern Mutual Life. Mutuals accounted for 21% of the total industry assets, 17% of premium income, and 36% of life insurance in force. [Smallenberger].

Drivers of Demutualization

Many factors drove demutualization. As a business strategy, demutualization was seen as a company’s route to increase competitiveness and profits as a one-stop shop for all kinds financial services. But macroeconomic forces, like globalization, government spending, and the aging of the Boomer generation also contributed to the trend. Pressure to demutualize or not varied, of course, by company.

Insurers needed capital to compete

In the freewheeling financial industry of the late 1990s and early 2000s, before the reality check of 2008, mutual insurers looked over-specialized and under-financed relative to the competition. The industry landscape and outlook was described in 2000 by executive James Smallenberger of AmerUs Group (acquired by British insurer Aviva plc in 2006) in a 2000 Drake Law Review article.

Smallenberger predicted “continued consolidation within the life insurance industry and convergence of the life insurance industry with… banks, securities firms, and mutual fund companies. Many life insurance companies will need to gain significant economies of scale through acquisition or internal growth in order to cost-effectively invest in new products and technologies to meet changing insurance and investment needs and customer service expectations…”

“Mutual insurers do not have sufficient organizational flexibility to participate in the emerging integrated financial services market” [Butler, et al]. Smallenberger believed that “companies unable to achieve the necessary economies of scale will be gobbled up by larger competitors.” [Smallenberger].

Managerial self-interest

Consumer advocates, especially in New York, charged that executives at mutual insurers might use demutualization as an opportunity to appropriate the general account surplus—the owners’ equity—for themselves. This was a murky area, and, in the patchwork system of insurance regulation in the U.S., the rules varied by state.

In a mutual insurer, the surplus belongs to the policyholders. In a stock company, it belongs to the shareholders. To the extent that executives could choose to reward shareholders—of whom executives were likely to be among the largest—the path to self-enrichment was certainly there. In the collapse of First Executive Corp., parent of Executive Life, insiders did in fact engineer control of a large share of the failed company’s assets.

Few policyholders knew they had rights to a portion of the equity. Rules for securing, quantifying and transferring those rights varied by state, if they existed at all. Prudential’s demutualization in 2001 showed one way in which the pie could be sliced among its then-approximately 11,000,000 policyholders. [IRS, Demutualization-Revised]

“Management gave 454.6 million shares to the policyholders directly and in addition sold 110 million shares to the public at $27.50 per share. Part of the $3 billion in proceeds was paid to cash-out small policyholders and to other policyholders who chose not to receive shares of stock in the new company.” [Meador & Chugh]

Foreign firms’ interest the U.S. life/annuity market

Large European insurers were naturally eager to enter U.S. market. According to a May 1999 Bloomberg News report, the U.S. “accounts for more than half the world’s retirement savings market,” which Intersec Research of Stamford, Conn., predicted would grow 39% to $15.4 trillion by 2003. (That number reached $40 trillion in 2024, according to the Investment Company Institute.) To accept foreign investment, however insurers needed to be stock companies. The Equitable’s demutualization in 1991 was driven by the prospect of a $1 billion capital infusion from French insurance giant AXA [International Herald Tribune].

Banks’ desire to access insurance assets

Mutual insurers could see that financial conglomerates were encroaching on their turf. Banks, which sell fixed-rate annuities today, were as interested in diversifying into insurance as insurers were to diversify out of it. [Stephen Friedman, “The Next Five Years.”] “On the demutualization debate, the proposal for demutualization comes not from the life insurance companies, which are very happy being mutual companies, but from the banks, because the banks want to demutualize the life insurance companies and then buy them. That is more than a sidelight on this discussion, I think, because it reflects a worldwide trend. If I can coin a double cliche, I would call that trend the ‘globalization of the homogenization of financial institutions.’”

Financial Megatrends

The growth of the U.S. financial sector in the 1990s could not have occurred without a growing money supply. An increase in deficit spending by the U.S. government after 1980 provided that supply.

The national debt is the difference between what the federal government has spent into the economy since the founding of the country and what it has taxed out of the economy. In 1980, the accumulated difference was $908 billion.

The Reagan Administration criticized the debt as a drag on the economy. But rather than reduce it by cutting spending and raising taxes, the administration cut taxes and increased military spending. Over the next decade, the debt rose to $3.23 trillion. Those new trillions cascaded through government contractors, banks, businesses, employers, the financial markets, and American households.

The national debt reached $5.67 trillion in 2000 and then more than doubled, to $13.56 trillion by 2010 as a result of the bailout of the financial system after 2008. Today, the debt stands at more than $33 trillion. The national debt troubles many people. They believe that U.S. taxpayers will have to pay down the debt someday, impoverishing themselves in the process. Reasonable economists disagree [Fiscaldata.treasury].

Evolution of life insurers into investment companies

Even before they converted to stock companies, mutuals were already creating “variable” or “indexed” life insurance and annuity products that offered potential for investment growth along with their usual insurance-related benefits. “The spike in interest rates at the beginning of the 1980s “caused the development of a series of investment products lodged within life insurance companies’ variable life and annuity products. These products pass on to the customer the risks and the benefits of the investment management process.” Also, “many large life insurance companies have bought large investment management firms. Alliance Capital, for example, with more than $40 billion under management, is a subsidiary of the Equitable… The life insurance business itself has become an investment management business.” [Friedman]

An unprecedented bull market

By demutualizing, life insurers were following the flow of the 1990s. The flow was into stocks. The deregulation of telecom industry, the mass ownership of personal computers, the Internet, and the dot-com boom gave investors plenty of opportunity to invest. It was the period of index funds and discount brokerages, when “Main Street met Wall Street.”

The technology-heavy NASDAQ was 458 at the start of 1990, and 4,798 in March 2000, before the inevitable shake-out of 2001. The S&P 500 was 813 in 1990 and 2,756 in March 2000. The DJIA was 2,560 at the beginning of 1990 and 11,390 at the beginning of 2000. If life insurers wanted to join this party, and hold onto customers, they would have to become part of the securities world.

Changing regulations

Changes in federal tax law helped shape the evolution of the life/annuity business in the 1980s and 1990s. The Tax Equity and Fiscal Responsibility Act of 1982 (TEFRA) eliminated a loophole in the use of variable annuities, along with many other tax breaks. But despite TEFRA, the variable annuity allowed wealthy investors to delay taxes on the growth of their investments until they retired.

In 1984, the passage of the Deficit Reduction Act (DEFRA) limited the deductibility of policyholder dividends paid by mutuals as a way to “allocate taxes more equitably between mutual and stock life insurers” [McNamara and Rhee]. In 1988, a New York law ended a 66-year prohibition against demutualization and “served as a model for demutualization statutes in other states” [Battilani and Schröter].

The demutualization trend, already well under way, was eventually codified and sanctified by legislation at the end of the Clinton administration. “With the passage of the Gramm-Leach-Bliley Financial Services Modernization Act in 1999, the Depression-era barriers that blocked cross-industry mergers and product sales among banks, securities firms, and insurance companies have been removed. This reform will clear the way for these firms to move increasingly into each other’s businesses, thereby forcing each firm to become more efficient, more creative, and more customer-focused than ever” [Smallenberger].

During the 1990s and early 2000s, 37 major life insurers demutualized. Of those, the estimated number of policyholders was reported for only 15 companies was available. They had an estimated 29,713,000. Of that total, Prudential and MetLife had combined 22,200,000 policyholders.

Boomer saving in tax-deferred 401(k) plans

The macro-trend arguably driving all of the financial micro-trends of our recent history is the maturation of the Baby Boomer Generation. By 1990, the entire Boomer generation (born 1946 to 1964) was old enough to be in the workforce. They had married, created families, set up households. They were beginning to save in large numbers in hundreds of thousands of relatively new 401(k) plans.

U.S. savings in tax-deferred defined contribution savings plans (e.g., 401(k)s and 403(b)s) was only $874 billion in 1990. By 2000, it was $2.958 trillion, According to the Investment Company Institute. In 1990, $636 billion was in individual IRAs.

By 2000, that figure was $2.629 trillion (reflecting the growth of “rollover IRAs,” which contain money saved in defined contribution plans but later “rolled over” to individual IRAs). In 1997, when I went to work at The Vanguard Group (now “Vanguard”), a kind of cooperative, it managed about $250 billion worth of mutual funds. In 2024, Vanguard managed $7.2 trillion.

This is the first part of a two-part article on demutualization. The second and final part, covering the opposition to, the impact of, and the long-term implications of demutualization, will appear in the November issue of Retirement Income Journal.

Sources

Battilani, Patrizia, and Harm G. Schröter. “Decumulation and Its Problems,” Quaderni – Working Paper DSE N° 762.

Butler, Richard J., Yijing Cui, and Andrew Whitman, “Insurers’ Demutualization Decisions,” Risk Management and Insurance Review, 2000, Vol. 3, No. 2, pages 135-154.

Friedman, Stephen J. “The U.S. Life Insurance Industry: The Next Five Years” (1990) Pace Law Faculty Publications. https://digitalcommons.pace.edu/lawfaculty/115

“Historical Debt Outstanding,” FiscalData.treasury.gov https://fiscaldata.treasury.gov/datasets/historical-debt-outstanding/historical-debt-outstanding

Malkin, Lawrence, and Jacques Neher. “French Insurer to Put $1 billion into Equitable: AXA Buys Stake in U.S. firm,” International Herald Tribune, July 19, 1991.

McNamara, Michael J., and S. Ghon Rhee. “Ownership Structure and Performance: The Demutualization of Life Insurers.” The Journal of Risk and Insurance, Jun., 1992, Vol. 59, No. 2 (June, 1992).

Smallenberger, James A. “Restructuring Mutual Insurance Companies: A Practical Guide Through the Process,” Drake Law Review, Vol. 49, 2001.

© 2024 RIJ Publishing LLC. All rights reserved.