Starting more than two decades ago, many of the major life insurance companies switched to distributing their products through independent intermediaries instead of through captive sales forces. The change forced insurers to compete against each other for advisors’ loyalty—by paying attractive commissions and/or issuing appealing products.

More recently, many investment advisors’ revenue models evolved from selling products for a commission to selling advice for a fee. As a result, the power of manufacturer-paid commissions to drive annuity sales has been diluted. For future sales growth, annuity issuers must convince more fee-based investment advisors that annuities are worth buying.

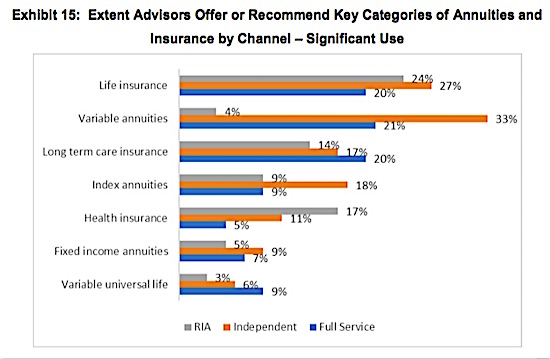

So far, life insurers aren’t doing too badly. Annuities are designated hitters, so to speak, in the financial instrument lineups of most investment advisors, not everyday players. Relative to reasonable expectations, annuity issuers can point to progress in penetrating the advisor market, especially in the independent broker-dealer channel. RIAs (registered investment advisors) remain resistant, however.

Howard Schneider

What do advisors say about insurers? RIJ recently received a copy of “What Advisors Want from Annuity and Insurer Providers-2019,” a study by Practical Perspectives, the Boston-area financial services market research firm.

Over some 120 pages of text and charts, the survey provides both statistical data and anecdotal responses to questions regarding annuities and annuity issuers from advisors in three distribution channels: full-service broker-dealers (wirehouses), independent broker-dealers, and RIAs (registered investment advisors).

Howard Schneider, the president of Practical Perspectives, spoke with RIJ this week about his study. He shared some of the impressions he received while talking directly to advisors, including many RIAs. While upbeat about the potential for life insurers to persuade RIAs in particular to recommend annuities to their clients, he did not downplay the obstacles.

Annuity issuers are having their greatest success with the one-in-four advisors whom Schneider describes as annuity “enthusiasts.” Members of this group are most likely to be found at independent broker-dealers and to accept commissions on annuity sales. But a couple of factors are eroding the numbers of annuity enthusiasts.

Some of these advisors, too new to have large enough books-of-business for a fee-based practice, rely on commissions temporarily, and it’s not clear if they’ll continue to sell annuities in the future. Enthusiasts also tend to be older than the average advisor, Schneider found. As they retire, it’s not clear who will replace them.

There is of also a fundamental obstacle to expanding annuity sales among investment advisors: insurance products are peripheral to what they do. “One of the conclusions of our study is that, even for advisors in the independent channel, who often use annuities and insurance, it’s not core to their relationship with their clients. It’s an add-on,” Schneider said. “It’s an important add-on to some of them, but not the foundation of their relationships. That relationship is based on investment planning, which leads however to risk management, which raises the subject of insurance.”

From the Practical Perspectives study.

The study confirmed the axiom that annuities are typically discussed at a milestone in the client’s life, such as a retirement. “We asked advisors to describe the circumstances in which they recommended annuities, and the second most frequent answer was ‘changing circumstances,’” Schneider said. The most frequent answer was, “When preparing a comprehensive financial plan.”

“They don’t bring up insurance or annuities on an ad hoc basis,” he added. “They’re willing to suggest annuities when the needs arise, but not at every opportunity. The topic is usually driven by the planning cycle, when they’re addressing an issue that requires insurance.”

RIA clients are likely to be wealthier and not as risk-averse as most Americans, so they’re less receptive to products, like index annuities, that promise no investment loss if held to term, Schneider told RIJ. Investment advisors and their clients tend to be risk-takers; buying an annuity means transferring risk to a life insurance company and, in most cases, paying the insurer to take it.

“RIAs tend to deal with clients who have less need for insurance solutions like, for instance, principal-protected products,” he said. “RIAs have told me, ‘I understand the value of an indexed annuity over the short-term, but our firm has a strategy that we think will provide better returns over the long-term.’ There’s some risk involved but most of their clients are willing to accept risk. Their clients will accept more risk than, say, clients of advisors at banks [who tend to have less savings than RIA clients].”

The sheer newness and scarcity of no-commission annuities is also limiting the pace of annuity sales to RIAs. “Another challenge, obviously, is that RIAs are fee-based. While no-commission annuities are available today, the products are relatively new and many have limited functionality. Many RIAs have come up through the securities industry, where insurance product sales are one-off events. A high percentage of them are pure RIAs; half are not insurance licensed,” Schneider said.

“Many of them will discuss insurance with clients but then they’ll say, ‘Go see your insurance agent about that,’ or ‘Go to a provider of low-cost insurance. Some have insurance affiliates. Their model for engaging with insurance and annuities is different, and that’s going to limit demand.”

Annuity issuers also face a potential communication disconnect when they send sales-trained wholesalers to talk to RIAs. Brain-wise, life product sales pitches historically appeal, at least in part, to the limbic system, and RIAs tend to operate from the cerebrum.

“RIAs are very analytical. They might look at the internal rate of return on an insurance product and say, ‘It doesn’t measure up to what I can do.’ But in doing that, they may not consider the value of the insurance. It’s hard to put a value on insurance; at the same time, you can’t compare annuities with investments without ascribing some value to the insurance component,” Schneider told RIJ.

In general—and investment advisors have voiced this complaint for years—RIAs aren’t hearing what they want to hear from life insurer reps. They want better quantification of the value of annuities, such as mortality credits or the ability to create more risk capacity in another part of the portfolio. They also want to hear the truth, preferably without varnish.

“RIAs tend to say that the information they get from insurance companies is biased and not objective. They want to know exactly what type of client in what type of situation will be helped by a particular product. They want a clear understanding of the benefits. They want to be educated, not sold. In terms of understanding the RIA mindset, the asset management firms are up to speed but the insurance firms are still behind the curve,” Schneider said.

“They also want to understand how the product will perform in certain situations,” he added. “Some of the ways in which these products have performed have surprised people, and they don’t like to be surprised. They say, ‘If I don’t understand something, I won’t offer it to my clients.’ RIAs do not want an over-hyped sales approach. Many of them became RIAs to get away from pushing products.”

© 2019 RIJ Publishing LLC. All rights reserved.