A Berlin-based “pensiontech” firm and its venture-cap backers are betting that European Millennials will like the idea of saving sustainably for retirement whenever they use their Mastercard debit cards to buy lattes, burgers, or sneakers.

The company, Vantik, issues the Vantikcard (a white-label Mastercard debit card). It promises to invest 1% of the value of all Vantikcard purchases into the Vantik X fund—a fund of ESG (environmental, social, and governance) exchange-traded funds (ETFs).

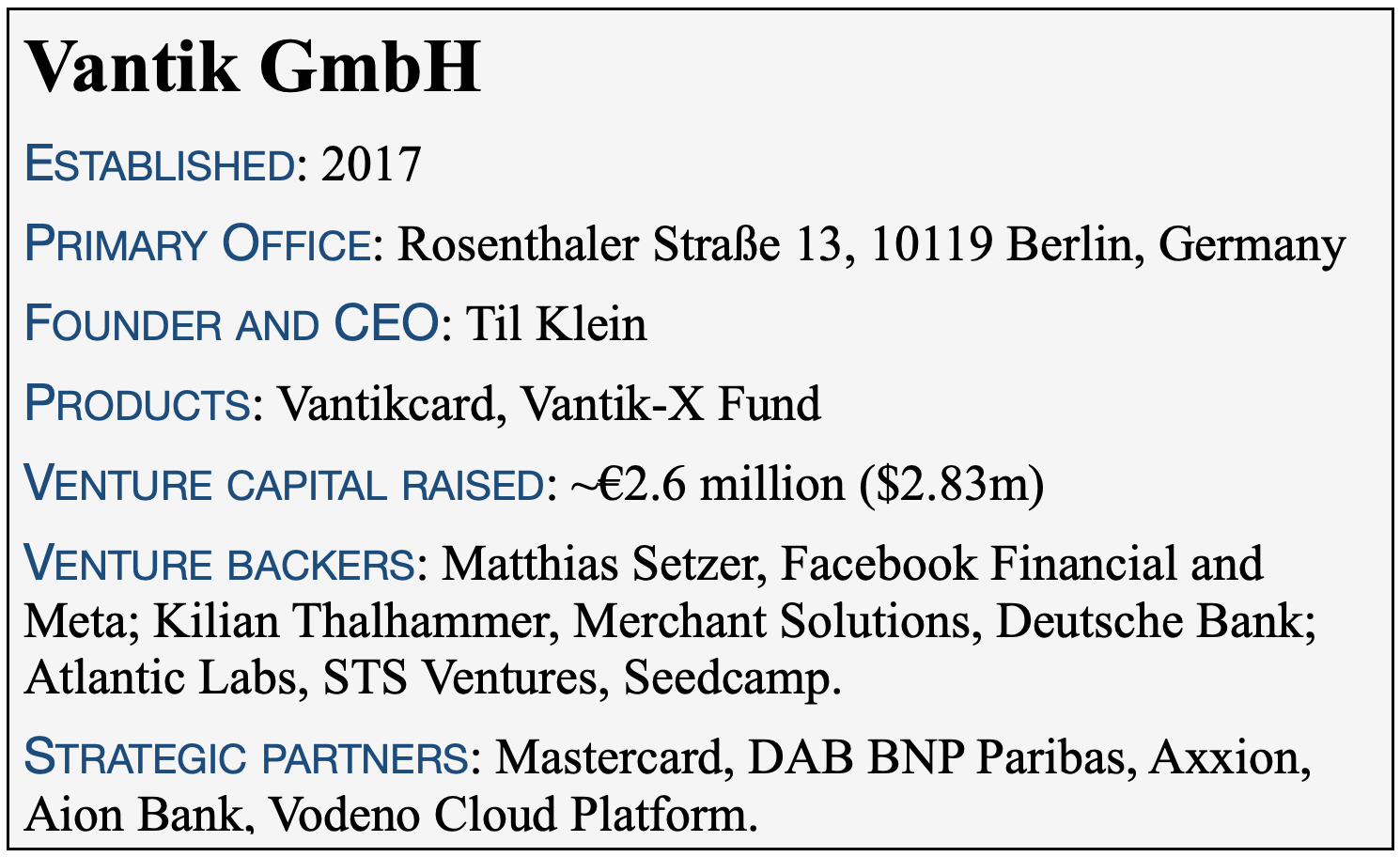

The fund-of-funds was launched in December 2018, by Til Klein, a 30-something German with a resume that includes Boston Consulting Group and UBS wealth management. Vantik issued its first private-label Mastercard debit card in April 2021. (Before launching the card, Vantik pursued retail ETF investors in other ways.) As of last Friday, the Vantik-X fund had about €5.4 million ($5.88m) under management and an NAV of €6.29 ($6.85)—up 26% from its €5 ($5.45) opening price.

“Our goal is to radically simplify old-age provision,” says the Vantik literature. “Nowadays nobody needs long contract terms for complicated old-age provision products that are not worth it in the end anyway. With the Vantikcard we enable you to start your retirement provision. So that you can easily save a small part for your pension while paying.”

Vantik integrates several au courant technologies—smartphones, ESG investing, Application Programming Interfaces between banks and phones, Apple Pay and Google Pay, cash-back rewards—to capture the hearts and wallets of young Europeans at a time when EU regulators and corporations dither over defined contribution pension reform.

Not coincidentally, Klein is a member of the expert council on European pensions at EIOPA, the European insurance supervisory authority. He was one of the panelists in a recent webinar kicking off the Pan European Pension Product, or PEPP. According to Klein, Vantik has begun the process of obtaining a permit to offer a PEPP. For a recent RIJ article on PEPPs, click here.

Kickstarter

Before you click to your calculator to prove that people can’t spend their way to adequate savings at a rate of 100:1, give Klein credit for finding a way to tease European Millennials into linking their bank accounts to his Vantik X fund—and by making the relationship sticky.

Vantikcard users can’t liquidate the Vantik X fund shares that they buy with their cash back rewards until age 55 or later, when they retire. If they cancel the card, they forfeit the shares that the company bought for them with their rewards.

But the rewards are just a “kickstarter.” Once Vantikcard holders have begun buying Vantik-X shares with their cash back rewards, they will be encouraged to supplement their rewards-based shares with regular transfers from checking accounts at any German bank to the Vantik fund. Their own investments are fully liquid.

It’s all about behavioral finance. “The idea with Vantikcard is to use the 1% cashback as a kickstart into retirement savings and for customers to then save on top of the cashback. The biggest problem for many people is to get started. The Vantikcard helps with that,” a person with knowledge of the company told RIJ.

Klein told GQ magazine last December, “It’s not about supplementing your pension with the cash-back alone. The aim is to create a low-threshold entry opportunity. We want to take the fear out of old-age provision and finally break the vicious circle of constant procrastination.”

Somewhere down the road, annuities could enter the picture. At age 55, Vantik X shareholders can sell their shares and take a lump sum or buy an annuity that pays out a regular lifetime income, according to press reports. In the meantime, they pay an all-in annual expense ratio of 0.95%. That covers fund management, transfers, trading, etc. (The card itself is free and has no annual fee.)

Somewhere down the road, annuities could enter the picture. At age 55, Vantik X shareholders can sell their shares and take a lump sum or buy an annuity that pays out a regular lifetime income, according to press reports. In the meantime, they pay an all-in annual expense ratio of 0.95%. That covers fund management, transfers, trading, etc. (The card itself is free and has no annual fee.)

There’s a “safety buffer”—though not a guarantee— designed to prevent loss of principal over the long run. According to one press report, “one percent of the funds collected from investors flows into a Vantik security buffer. The aim of the buffer is that at the beginning of retirement the investor has at least the amount that he has paid in… the safety buffer is managed by an independent foundation and compensates for a possible loss of capital at the beginning of retirement.”

Roundup time

Klein isn’t the first fintech entrepreneur to build a smartphone app that aims to make automated micro-investing easy for debit card-using young adults. In the US, the Acorns app gets people started investing by “rounding up” their purchases and buying ETFs with the difference. Betterment Visa debt card holders get various cashback rewards on purchases from select retailers. In Germany, there’s the Vivid Prime. It costs €9.9 per month and offers 1% cashback (up to €150) on all purchases, plus access to exclusive retailer discounts.

Vantik recently announced its own round-up feature. “So if you buy a coffee for 2.60 euros, you can automatically round up 0.40 euros and save for retirement. You’ll also be able to set your own savings rules so you can save at your own pace. One such rule could be that you pay five euros into the pension plan every time you’ve eaten burgers again,” Klein said in the GQ interview. The daily spending limit, assigned to each cardholder by Aion, Vantik’s bank, is between €400 ($435) and €1,250 ($1,358). Cardholders can earn cashback up to €100 ($109) each month.

Vantik’s approach may sound gimmicky—and far from proven—to someone at a hundred-year-old brick-and-mortar life insurance company. As a perk, for instance, Vantik invites members to personalize their plastic cards with special “artist, social media names and gamer tags.” But it’s a gimmick that seems to resonate with those who’ve grown up with iPhones in their hip pockets and buds in their ears. Two-thirds of his cardholders personalize their plastic cards, Klein said.

“This is exactly what we need for old-age provision: an easy-to-understand, low-threshold and motivating introduction,” he told GQ. “My tip: Don’t ask an expert, don’t read any books, don’t research on the internet, don’t try to calculate a pension gap. Just start first. The most important thing is to take the first step.”

© 2022 RIJ Publishing LLC. All rights reserved.