Yes, President William McKinley was a tariff-championing Republican. Yes, Congress passed several tariff bills in the 1890s. And, yes, the U.S. enjoyed an economic boom in the second half of the 1890s—a relief from the depression of 1893.

But neither McKinley nor the tariffs can take credit for enabling the U.S. to close out the 19th century on a high economic note and enter the 20th century—the American Century—as a global dynamo.

No. Historians attribute the boom to:

-

Discoveries of gold in Alaska, the Yukon, and South Africa in the mid-1890s

-

The Spanish-American Wara, declared and ended in 1898

Last April 2, “Liberation Day,” President Trump announced dramatic new tariff levies on most of the countries of the world, including America’s closest trading partners. He effectively put an end to our 30-year experiment in unfettered free trade and “globalization.”

The following day, the U.S. stock market dropped 10%. Global confusion ensued as leaders of Canada, Mexico, Germany, China, Japan and Vietnam, to keep the list short, struggled to figure out how their export-driven economies would be affected.

Why tariffs?

President Trump claimed that William McKinley, president from 1896 until his assassination in 1900, had employed tariffs to raise revenue, protect domestic industries from cheap foreign competition, and stimulate the U.S. economy.

He argued tariffs could drive foreign direct investment into the U.S., revive U.S. manufacturing, and reverse America’s huge trade deficit (in goods, not services) with the rest of the world—and that they could juice up the U.S. economy today.

This week, as some of the tariffs announced last April are scheduled to take effect, a hunt for a historical basis for bringing tariffs back won’t turn up much. While tariffs were a major political football after the Civil War, there’s no good evidence that they turned the U.S. economy around after the Crash of 1893.

Here’s Doug Irwin, a tariffs expert at Dartmouth, writing in an April 2000 National Bureau of Economic Research paper, Tariffs and Growth in Late Nineteenth Century America.:

“The U.S. experience in the late nineteenth century is often appealed to as evidence that high tariffs can prove beneficial to economic growth and development. Upon closer scrutiny, it is difficult to establish this claim.”

America’s Second Gold Rush

Most Americans probably remember reading about the gold rush of 1849, after the precious metal was discovered at Sutter’s Mill in California. Less discussed is the gold rush of 1896, when gold was discovered at Bonanza Creek in Alaska’s Klondike, in Canada’s Yukon, in South Africa, and in Australia. The flood of gold enriched not just lucky miners but entire countries.

At the time, a country’s gold reserves formed the basis for the quantity and value of its currency. And in the early 1890s, when panicky British investors were selling off their U.S. holdings, literal boatloads of gold were floating away from the U.S.

There’s widespread agreement among economic historians that gold from Alaska and elsewhere, which the U.S. Treasury bought with newly issued “gold certificates,” was a dominant factor in pulling the U.S. out of the long post-Civil War deflation—a reversal of the inflation associated with the war.

The record is unanimous on that point. And largely silent on tariffs.

Milton Friedman, the Nobel laureate in economics, wrote in his 1963 classic, A Monetary History of the United States, 1857–1960 (p. 91), referring to the campaign by William Jennings Bryan and Western farmers to have silver supplement the American gold reserves, which could increase the money supply and reverse the deflation that held down wheat and corn prices.:

Placer miner panning for gold in Klondike

“The secular decline from the 1860s almost to the end of the century… was reversed in the 1890s by the fresh discoveries of gold in South Africa, Alaska, and Colorado, combined with the development of improved methods of mining and refining. After 1897, ‘cheap’ gold achieved the objectives that had been sought by the silver advocates.”

The discovery of gold ended the farmer’s quest for “bimetallic” backing of U.S. paper money. Here’s Ron Chernow in his 1990 National Book Award–winning biography of J.P. Morgan:

“The Yukon gold rush and gold strikes in South Africa and Australia helped expand the U.S. money supply and led to higher prices. The bitter deflationary politics of the late nineteenth century subsided.”

The nation’s money supply, and its creditworthiness, depended on its stock of gold, and the fact that foreign creditors could redeem dollars for gold contributed to a massive outflow of gold after the confidence-shattering crash of 1893. In the West, farmers believed silver could back dollars and lift the money supply. The U.S. Treasury and New York bankers contemplated floating bonds to buy gold.

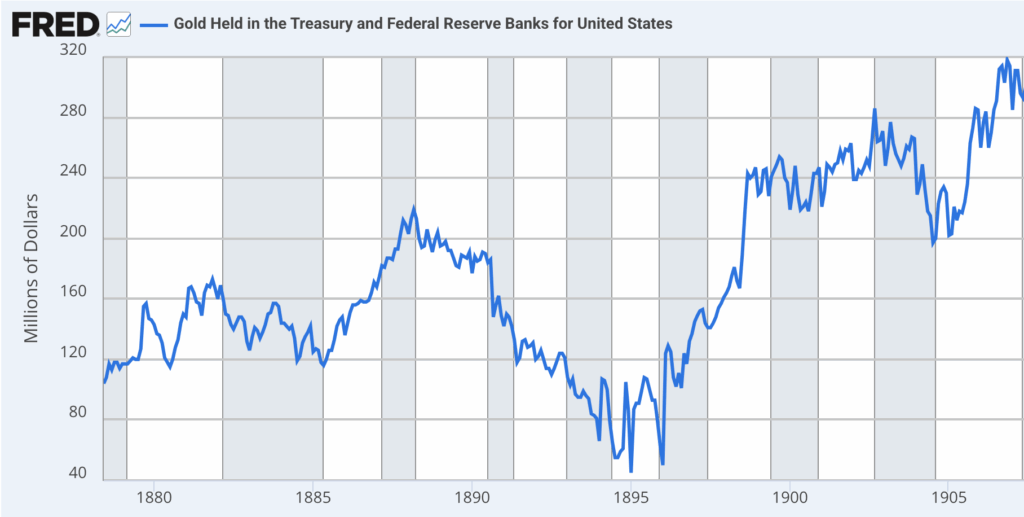

Gold strikes in Alaska and elsewhere rescued farmers and bankers alike. It was not a case of deus ex machina; the pre-Klondike global shortage of gold incentivized a worldwide search for the precious metal (throughout history the preferred method for paying mercenaries and settling international debts) and stimulated the development of more efficient refining methods. Starting in 1896 on (see chart below) the U.S. gold supply did nothing but grow. For most of the previous decade, gold stocks were falling and the U.S. suffered from deflation.

The War with Spain

The tariff debates of the 1880s and 1890s were not unrelated to the gold issue. The common denominator was deflation and falling prices. Democrats touted low tariffs as the solution, while Republicans saw higher tariffs as the remedy. But tariffs were a sideshow. The real problem was the Treasury’s shortage of gold. As Irwin writes:

“The country’s monetary policy under the gold standard, not the tariff, was responsible for the deflation of this period.”

Then came the four-month war with Spain in 1898, which “brought a wave of prosperity… ‘After war will come the piling up of big fortunes again; the craze for wealth will fill all brains,’” wrote economic historian Joseph Dorfman in The Economic Mind in American Civilization, Vol. 3 (p. 230), quoting contemporary observer William Dean Howells, editor of The Atlantic Monthly.

Teddy Roosevelt leading ‘Rough Riders’ in Cuba, 1898

Tariffs were also cousins to the noisy, brief war in Cuba. The common denominator in this case was sugar. Tariffs on sugar provided steady revenue for the U.S. Treasury, but on-and-off tariff policy on sugar in the 1890s created a boom-bust cycle in Cuba, the site of U.S.-owned sugarcane fields and the main source of raw sugar for U.S. refiners.

Economic instability helped spark the Cuban War for Independence from Spain. Spain began burning sugar plantations. The U.S. intervened, Teddy Roosevelt and his Rough Riders took possession of Cuba, and U.S. refiners ended up in control of Cuban sugar (and Cuban politics) until the 1959 communist revolution, led by Fidel Castro.

Victory over Spain gave the U.S. dominion over not just Cuba but also the Philippines. Almost overnight, the country became a global power, with new commitments and opportunities in Asia. American exports later helped European countries fight (and recover from) World Wars I and II, and the U.S. became the world’s biggest creditor nation. Today, we’re the world’s biggest debtor.

Paradoxically, that makes us rich. Much of the world’s savings is parked here. We can afford to run a large trade deficit because we’re wealthy, because everyone everywhere gladly accepts dollars, and because foreigners recycle their export-earned dollars back to the U.S. by investing here or buying our Treasuries.

New U.S. protective tariffs, or even the threat of tariffs, aren’t likely to reverse that mega-trend. The Trump tariffs appear to be bargaining chips for deals he’s making on the side. McKinley could never have imagined that.

© 2025 RIJ Publishing LLC. All rights reserved.