A cascade of news articles on Bloomberg, in the Financial Times, and other respected financial news sources has focused on the potential for significant defaults and failures in the opaque, illiquid world of high-yield private credit. A spike in withdrawals from private credit funds managed by Blue Owl and Blackstone has spooked investors across the private-credit sector.

Blue Owl stock was reported down by 9% yesterday, according to the New York Times. Blue Owl owns Kuvare Asset Management and provides investment management services to Kuvare Holding’s life insurers, Guaranty Income Life and United Life. Kuvare also has a reinsurer in Bermuda.

Investment firms with similar strategies have been feeling Blue Owl’s pain for more than a year. Apollo, the private asset manager tied to life insurer Athene, has seen its share price drop to $104 this week from $177 in December 2024. KKR, which controls the Global Atlantic life insurers, has seen its share price drop to $90 this week from $165 in January 2025.

F&G Annuities & Life CEO Chris Blunt

Then there’s Blackstone and its strategic partner, F&G Annuities & Life (F&G). Bloomberg reported this week that Blackstone Inc. is allowing investors to redeem a record 7.9% of shares from its flagship private credit fund, calling the redemptions “the latest sign of unease in an industry that’s faced a wave of withdrawals.”

Blackstone has long managed private credit assets for F&G, whose CEO, Chris Blunt, recently expressed his frustration at the disconnect between F&G’s strong fundamentals and its low stock price. Blunt said shares of the company are trading at roughly 62% of book value. That outlook doesn’t match what he called F&G’s “pristine fixed book” of assets. F&G’s liabilities include 55% fixed indexed annuities and 11% fixed-rate annuities, which have surrender penalties and market-value adjustments to protect them from sudden withdrawals by contract owners.

“The stock is trading as though there are billions and billions of credit losses coming,” Blunt said at his company’s earnings presentation in February. “It’s pretty inexplicable to me.” F&G’s shares closed Tuesday at about $22, or down more than half from $48 in November 2024.

The word on The Street is that investors are bailing out of private lending funds and selling the shares of private lenders because of an anticipated bust in the A.I. business. The world has over-invested in A.I.-related business, goes the conventional wisdom, and a lot of recipients of leveraged loans mid-could fail when the inevitable correction comes.

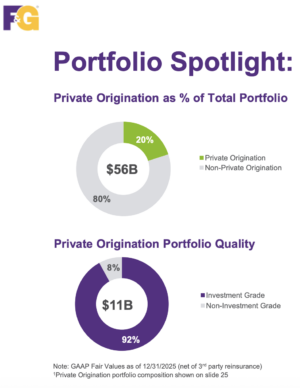

The fact that 20% of F&G’s assets are in private credit, and that Blackstone runs its private credit assets, could explain the low value of F&G stock.

From F&G Annuities & Life February 2026 Presentation, p. 26.

But there could be a deeper reason why the share prices of prominent companies in this sector have fallen. Asset managers have ramped up the leverage of the annuity-issuing life insurers that they own. Higher leverage means higher returns-on-equity. But it also means higher risk.

Which brings us to the Bermuda Triangle strategy. That strategy (as regular readers of RIJ know) involves three types of companies working in concert—an alternative asset manager, a life insurer that issues fixed-rate or fixed indexed annuities, and a reinsurer that assumes the life insurer’s risk in a way (“funds withheld reinsurance” or “modified coinsurance”) that leaves the asset manager in charge of the life insurer’s assets.

The annuity sales provide low-cost revenues, the revenues help the life insurers buy investment-grade tranches of bundles of private loans from the asset managers, and the reinsurance lightens the capital requirements that are a drag on profits.

All of the asset managers and life insurers mentioned above happen to have big presences in the Bermuda Triangle. As noted, F&G is a major issuer of fixed deferred annuities, 20% of its assets are in private credit (see chart at left), and it has used “flow reinsurance” to move liabilities off its own balance sheet and onto the balance sheet of an affiliated reinsurer in Bermuda, F&G Life Re.

(F&G recently announced the sale of F&G Life Re to newly-created Ancient Financial, which will change the reinsurer’s name to Ancient Re. Ancient Financial’s new CEO, Erich Schram, previously ran Blackstone’s Insurance Portfolios, a position that Blunt once held at Blackstone.)

According to a recent statutory filing in its home state of Iowa, F&G runs a 2.4% surplus on liabilities of $71.4 billion, compared with a life insurance industry average of 7.2% (in 2024). Of $12.5 billion in annuity sales, it reinsured $9.3 billion, thus vastly reducing its reported new liabilities for the year. Using “funds withheld” and “modified coinsurance,” it is able to move the liabilities off its balance sheet while keeping its fee-generating assets under management.

Running a “capital light” annuity business, which is designed to sound attractive to investors, is just another way of describing a highly leveraged business. Insurance is by definition a leveraged business: it borrows from policyholders to invest. But the rising leverage of the Bermuda Triangle life/annuity companies has been worrying the Federal Insurance Office, Federal Reserve economists, a former chair of the Senate Banking Committee, the International Monetary Fund, and the Bank of International Settlements for years.

They worry because leverage is the high blood pressure of the financial industry. It helps ripen conditions for the “strokes” known as credit crises. It’s a strange kind of high blood pressure that’s contagious because of the interdependence of the big investment managers.

Neither state insurance commissions, whose states compete to attract life insurers, or their trade group, the National Association of Insurance Commissioners, which is not a regulator per se and has no enforcement power, have shown much serious interest in this.

© 2026 RIJ Publishing LLC.