The value of short positions on U.S. life insurance stocks has more than doubled to over $5 billion in the past year, according to an analysis of ORTEX data by Reuters.

The move “reflects concerns about [life insurers’] exposure to the opaque private credit sector,” the news agency reported this week. According to Reuters:

“Traders added almost $3 billion to the value of short bets, or bets that a stock price will decline, on 10 top U.S. life insurance companies in the past year, bringing the total to around $5.3 billion, Reuters’ calculations based on data provided by financial analytics firm ORTEX show. These firms saw a more than 130% increase in the proportion of their stock that traders borrowed in order to take out short positions on these companies, the data showed.

Short-sellers, including hedge funds, sense that the bespoke loans that asset managers have sold to life insurers could fail in the next financial crisis. If so, that might drive some publicly traded life insurers to losses, lower their stock valuations, and potentially lead to insolvencies. Recent media publicity about the dangers of the black boxes of private credit has conflicted with private credit vehicle managers’ protests that their private loan structures are built to withstand crises.

They may have a point. Life insurers aren’t buying individual high-risk loans; rather, they often provide anchor-financing for an asset manager’s collateralized loan obligations (CLOs). These are actively managed bundles of high-yield, below-investment-grade, privately-arranged loans to middle-market companies that banks no longer lend to directly.

CLOs convert individual loans into bond-like securities of varying yields and credit quality. These bundles are divided into equity tranches, B-rated tranches, and A-rated tranches, in descending order of risk. Owners of AAA, AA, or A-rated tranches get paid first, but get the lowest returns. Equity tranche owners receive interest payments only after owners of all the other tranches are paid. Life insurers tend to own the lowest-risk tranches, which are designed to yield at least a percentage point more than comparably-rated bonds.

According to members of that industry, owners of A-rated tranches of CLOs have never lost money. That’s partly because the bundles of loans are actively managed, with managers working constantly to replace or refinance loans that weaken. But that process also makes the tranches hard to price and precludes full liquidity for investors.

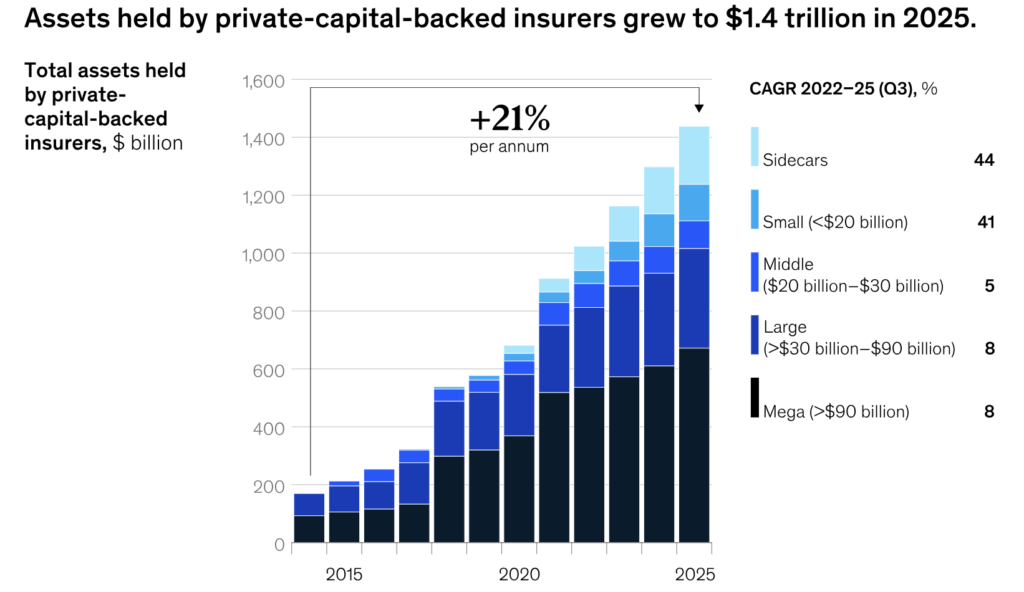

Source: McKinsey & Co.

The Bermuda Triangle

The concerns of short-sellers are linked to the growth of what RIJ has called the Bermuda Triangle strategy, where three types of entities—life insurers that issue investment-like deferred annuities, asset managers that originate and/or distribute private market loans, and affiliated captive or offshore reinsurers—cooperate to raise annuity yields, enhance capital flows to private credit, and reduce the insurer’s surplus capital requirements.

The strategy has also been called “capital light” life insurance, “virtuous flywheel” or “permanent capital” approach to asset management. But the strategy works best when it takes place in relative darkness—inside a single holding company, in a state with weak insurance regulation, in Bermuda, and—most importantly—when it depends on the performance of slices of complex, illiquid, hard-to-price, actively-managed bundles of bespoke high-risk loans.

As Reuters reported:

“Concerns are not about a single blow‑up, but about potential structural vulnerabilities with the (private credit) asset class having much less regulation and oversight than the traditional banking system,” said Mediolanum International Funds head of fixed income Daniel Loughney.

“Institutional exposure to the asset class has grown significantly over the past decade. Overall we see a problem brewing that will affect the life assurance markets, annuity markets and the asset management industry,” he said.

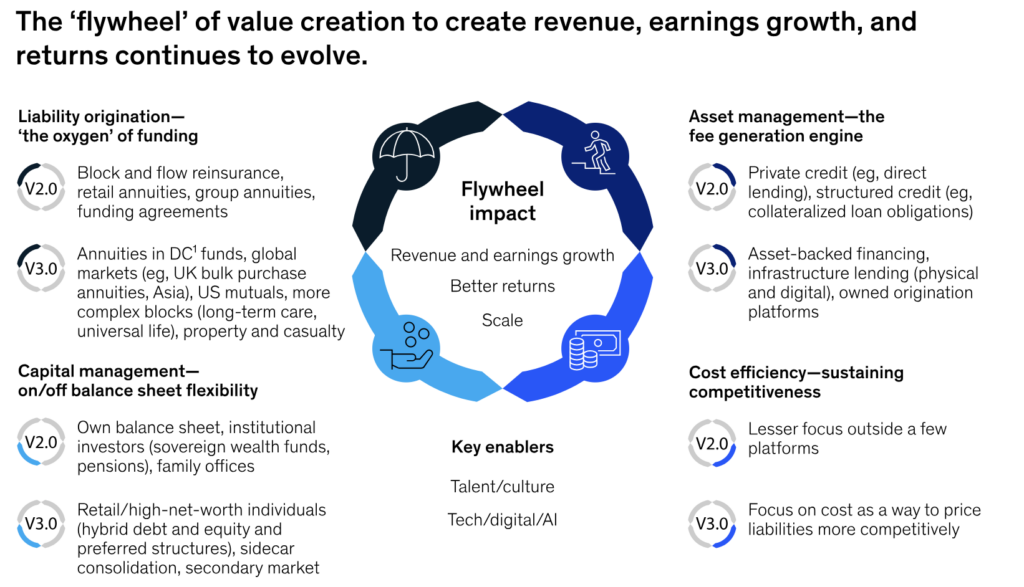

1 Defined contribution. Source: McKinsey & Co.

“Life insurers owned by PE (private equity) firms are very long private assets and have very limited capital surplus available,” said Alberto Gallo, founder of hedge fund Andromeda Capital. The firm holds bets against insurers’ bonds.

Private credit holdings among U.S. life and annuity insurers more than doubled over the last 10 years, during a period of historically low official interest rates, according to ratings company and insurance industry specialist AM Best.

U.S. life insurers have roughly 35% of their balance sheets tied up in private lending, the International Monetary Fund has reported, citing Moody’s data. This type of alternative credit offers higher yields and long-term steady returns, fitting the mandate of insurance companies, which try to match investment horizons with the timing of their payouts to contract owners over years or decades.

The S&P 500 U.S. insurance index, which includes life insurers, has fallen almost 5% so far this year versus a 4.7% rise for the broader S&P index.

Barclays analysts estimate that the collective earnings per share of 15 U.S. life insurance companies will drop by almost 7% over the course of this year, saying that markets appeared to be pricing in a “fairly severe” outcome, including either a recessionary backdrop or losses within private credit portfolios. However, they added that these concerns were overdone.

When looking at short bets against global insurance firms, the value grew by more than 60% in the 12 months to April 15, to over $31 billion, according to calculations by Reuters using S&P Global and LSEG data.

Short positions in Principal Financial Group soared more than 80% in the past year, hitting a peak of over 4% in March, while bets against Brighthouse Financial reached a record high of over 13% of the available stock on March 9, the ORTEX data showed. Both companies declined to comment. Short positions in Prudential rose to 3.27% from 1.96%.

© 2026 RIJ Publishing LLC.